Members of the millennials generation are known for being attached to the latest “smart” mobile device. But according to recent surveys, millennials (generally, those aged about 15 to 34) still like to talk to another human being – in-person – when it comes to their finances.

For example, 75% of millennials surveyed for a report from San Francisco-based Charles Schwab Corp. said they would be more interested in talking with a professional financial advisor when their financial situation became more complicated: that rate was higher than for Generation X, at 72%, and for baby boomers, at 71%.

Similarly, a 2015 report from San Francisco-based Salesforce.com Inc. found that 51% of millennials who would like to change how they currently manage their investments said they want to collaborate with a financial advisor, slightly less than 56% of Gen Xers and 65% of baby boomers who feel the same. Both reports were released in May 2015.

The interest of millennials in actually meeting with an advisor is not surprising to Peter Drake, vice president of retirement and economic research with Toronto-based Fidelity Investments Canada ULC. He notes that many members of this generation – in Canada, at least – grew up learning the value of teamwork.

“They have spent a lot of their years in school working as teams,” says Drake. “And that suggests to us that they’re prepared to team up with an advisor.”

More specifically, Drake believes, this younger generation of investors trust and are impressed by advisors who work within larger teams themselves.

Part of working together with this millennial clients, according to Drake, is sharing data through technology. Millennials know and understand data; this age group also knows that data sometimes can be misleading. As a result, these clients will want to work with advisors who can provide solid information to be reviewed on millennials’ own time.

“It’s no longer the case [that] the advisor says to the millennial: ‘I’m the advisor and I have the training and experience, and here’s what you should do’,” says Drake. “I think the advisor has to demonstrate why that advice is good and show the data he or she is using.”

Indeed, sharing information and working as partners will help advisors to establish trust with millennials – something that is easier said than done with this demographic.

For example, only 49% of surveyed millennials believe their advisors have their clients’ best interests at heart, according to the Salesforce report, compared with 72% of baby boomers.

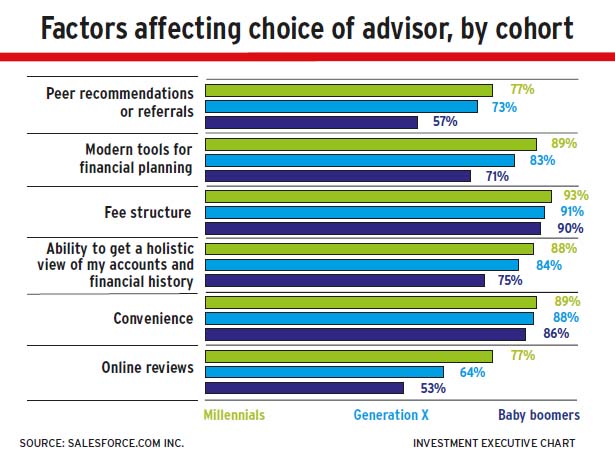

Although face-to-face meetings are important, technology remains a key part of any advisor’s relationship with millennials. In fact, 89% of millennials said that modern financial planning tools are an important factor when choosing an advisor, according to the Salesforce report, compared with 83% of Gen Xers and 71% of baby boomers.

Besides dealing with advisors who have the latest in desktop tools, millennial clients are looking for advisors who can talk – or exchange messages – with their clients at any time. According to Salesforce’s report, millennials are more likely to feel comfortable sharing documents, making investment decisions and getting advice via email than any other generation is. Simon Mulcahy, senior vice president and general manager, financial services industry, with Salesforce, views this level of comfort as part of the ongoing shift away from the regular quarterly or annual reviews that many advisors offer to clients.

Instead, millennial clients prefer more on-demand questions and answers; this practice allows clients to access their own information resources in addition to the information received from an advisor.

“You have this move away from this sort of butler-style concierge,” says Mulcahy, “to a sort of ‘wingman, hey just shout at me and I’ll help you out immediately if you need anything’ type of advisor.”

Mulcahy notes that this shift isn’t limited to a specific age group; it includes anyone who is “millennial-minded,” including Gen X or tech-savvy baby boomers.

Technology also plays a crucial role in how millennials select their advisor: 77% of surveyed millennials in Salesforce’s report said they feel peer recommendations are important when choosing a financial advisor, compared to 57% of baby boomers.

Similarly, the same proportion of millennials would use online reviews in selecting an advisor, compared with 53% of boomers.

“If you’re not online, you don’t exist anymore,” says Gary Liu, vice president of marketing for Hearsay Social Inc. in San Francisco. “Social [media] is how people pass the time when they’re in line at Starbucks or for the plane or the train.”

Without a professional profile on major social media sites, whether it’s Facebook, LinkedIn or Twitter, as well as having an updated website that is compatible with mobile devices, potential clients will not be able to find you when they conduct a search online from wherever they might be.

Still, many millennials don’t even seem to realize that they should be searching for such advice. According to the Charles Schwab report, only 62% of millennials are likely to invest, compared with 79% of baby boomers and 72% of Gen Xers.

As a result, the millennial demographic represents a potential market for advisors’ services, according to Drake, and should not be downplayed by the financial advisory industry, despite some unflattering perceptions of millennials.

“There was a time when the baby boomers weren’t making much money, and now they’re doing very well,” says Drake. “Remember that every generation has looked askance at the younger group – and, you know what, [that younger group] has come out OK.

“So,” he adds, “I think there’s a great future [for advisors’ books] in millennials.”

© 2015 Investment Executive. All rights reserved.