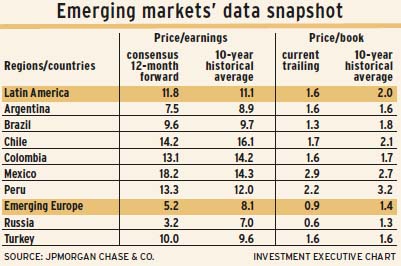

Emerging economies in Latin America and eastern Europe will face a challenging 2015, with wide divergences and no clear consensus among portfolio managers regarding the outlook for countries in these two regions.

For example, Paul Taylor, chief investment officer, fundamental equities, with BMO Asset Management Corp. in Toronto, is “modestly bullish, with a bit of trepidation” regarding these regions.

But Christine Tan, portfolio manager with Excel Investment Counsel Inc. in Mississauga, Ont., has “more of a negative bias” on these regions as a whole.

“The overhanging stressors” in these economies, says Matthew Strauss, vice president and portfolio manager with CI Investments Inc. in Toronto, “are low commodities prices and a tricky macroeconomic environment.”

One of the key determinants of the outlook for Latin America and eastern Europe is lower oil prices. Net oil-importing countries, such as Turkey, Peru and Chile, will benefit from lower importing costs for oil, while oil- exporting countries, such as Russia, Venezuela, Colombia and, to a lesser extent, Brazil and Mexico, will be hurt by declining oil revenue. The decline in gold bullion and base metals prices also will hurt exporting nations, especially countries in Latin America.

Given the divergence in the outlook for Latin America and eastern Europe, Taylor says, these regions “will follow a two-tier growth rate” in which economic growth in Latin America, which is dominated by commodities exports, will be weaker than in eastern Europe, which is a commodities importer.

But for eastern Europe, the risk of deflation spilling over from developed Europe runs high. In fact, “deflation has already spilled over into the region,” Strauss says.

Michael Greenberg, vice president and portfolio manager with Franklin Templeton Solutions, a division of Franklin Templeton Investments Corp. in Toronto, is a little more optimistic: “The credit cycle is improving and banks are willing to lend. [I don’t] see the eurozone area heading fully into deflation.”

But geopolitics also could dampen growth in eastern Europe. In particular, sanctions against Russia “are a big negative overhang,” suggests Strauss, who believes that “[Russia’s President Vladimir] Putin’s ambitions have cast a dark cloud over the region, with many countries exporting to Russia heading into recession.”

Given that the European Union is Russia’s largest trading partner, the sanctions have spurred “negative sentiments over the [regional] economic recovery that was supposed to occur,” Taylor says.

Overall, though, Tan and other portfolio managers are taking a stock-specific approach to investing in these regions. When deciding where to invest, Tan says, “it’s extremely important to understand the macroeconomic differentiation among markets.”

Tan focuses on “core secular themes that are independent of the underlying economic cycle,” such as health care and education, with selective bets on consumer stocks. “Consumers in commodities-producing countries will be a little more muted,” she says, but consumers in oil-importing countries will benefit from lower prices and more disposable income.

Secular plays, says Taylor, are benefiting from “urbanization, which is raising the standard of living” in emerging markets. Thus, he favours consumer discretionary stocks and industrials, which will benefit from demand for goods and services. His portfolio is neutral on financials, which will remain relatively stable, and underweighted in non-cyclical stocks.

In Latin America, both Strauss and Greenberg prefer Mexico. That’s because its economy is a “good growth story buoyed by reforms in the energy sector, although the government still has to deal with popularity problems, which has cast a shadow over the macroeconomic environment,” says Strauss. Mexico also will benefit from the strength of the U.S., the largest importer of Mexican goods.

For his part, Greenberg says Mexico “is a little bit more expensive, but you’re paying for quality.” He suggests that “investor confidence is up because the country is less reliant on energy.”

Strauss prefers infrastructure plays, such as Grupo Aeroportuario del Sureste SAB de CV, which holds concessions to operate, maintain and develop airports. He believes this stock represents a good growth opportunity.

Tan believes energy reforms in Mexico will take several years but “will be great for job creation and will result in infrastructure spending.” She is underweighted in Mexico, but she expects to add to her position. She holds Fibra Uno Administracion SA de CV, which invests in commercial and industrial real estate and will benefit from continued expansion.

There is less optimism for Brazil, Latin America’s largest economy, although there are opportunities in certain stocks.

Strauss “is bearish on Brazil, not only because of low oil prices but because it’s a big exporter.” Nevertheless, he is “more concerned about its leveraged economy” and adds that the country is “going into a period of fiscal austerity and heading into a recession led by consumers. The domestic drivers of growth are softening.”

Taylor says the appointment of a pro-business finance minister in Brazil will address inflation and implement “more credible fiscal and monetary policies, but this will take time to implement.”

Strauss holds Embraer SA, an aerospace conglomerate, which, he says, is “competitive globally when the home currency weakens” – as it has in Brazil.

As a secular play, Tan owns Kroton Educacional SA, the largest private educational company in Brazil and Latin America, which will benefit from increased spending in education.

Another country in Latin America that portfolio managers are keeping their eyes on is Peru, which continues to grow in spite of weak commodities prices, especially copper. Strauss likes infrastructure projects, and he invests in Credicorp Ltd., Peru’s largest financial services holding firm, which will benefit from infrastructure financing.

In eastern Europe, Turkey is the preferred economy. “Its strong economic direction has brought stability to growth,” says Tan.

Strauss adds that Turkey “is a big beneficiary of lower oil prices, which will benefit its large current account deficit.”

Turkey also is benefiting from lower inflation and interest rates. But, Greenberg cautions, security risks “could be a drag” on investing in the country.

As for specific Turkish stocks, Strauss likes Garanti Bank, the second-largest private bank, which has strong growth fundamentals.

Although Russia is considered to be politically risky, Taylor believes its “extremely ‘high risk/return’ profile is skewed in a positive fashion and equities markets have discounted the worst-case scenario.”

As a result, he is using hedging strategies to invest in the long-term potential of Russian equities, but cautions that this strategy is “not for the faint of heart.”

Tan also likes certain companies in Russia, such as Magnit PJSC, the country’s largest retailer, and Yandex NV, which operates the largest search engine in Russia. She is underweighted in Russia but says “it has strong businesses” that are attractive investments.

© 2015 Investment Executive. All rights reserved.