If you have not done so lately, re-examine the transportation stocks in your clients’ portfolios. Sudden weakness in these stocks — both Canadian and American — may signal problems ahead. This weakness may have a serious message for the entire market, as well.

The downturn in the transportation sector comes after a 16-year run of market-beating performance for these stocks. The S&P/TSX transportation subindex bottomed in 1999. Relative to the S&P/TSX composite index, the subindex has risen since then. Its rise relative to Wall Street’s benchmark, the S&P 500 composite index, started a little later, in 2000.

Although the pattern for these stocks has been similar in both countries, Canadian stocks produced much larger, long-term gains. Since 1999, the TSX transportation subindex has climbed by 817%, based on its monthly close in February 2015. In the same period, the Dow Jones transportation average gained 164%.

Compare the Dow Jones industrial average’s (DJIA) gains to the 128% rise in the S&P/TSX composite index or the 62% gain by the S&P 500 composite index in the same period.

From February 2015 to the May 2015 close, the TSX transports dropped by 13% and the Dow transports dropped by 8%. This price drop occurred as many transportation companies in both the U.S. and Canada continue to report continued gains in revenue and profits. But this apparent dichotomy is a typical phenomenon at the end of a rising market cycle – if this is in fact near the end.

For example, Southwest Airlines Co., the premier U.S. air carrier, reported a 6% first-quarter gain in revenue vs a year before and a 198% gain in net profit. Alaska Air Group Inc., top-rated among regional airlines, gained 4% in revenue and 67% in net profit.

Major U.S. railways cut expenses in the first quarter, helping to boost profits. CSX Corp. led with an 11% rise in net profit.

Canada’s two major railways did better, despite bitter winter weather and contraction in the U.S. economy in the first quarter. Canadian National Railway Co.’s revenue rose by 15% year-over-year and net profit rose by 13%.

Air Canada’s revenue rose by 6% and its cash flow jumped by 135%, but the company continued to report a net loss. And, in the trucking sector, acquisitions transformed TransForce Inc.’s revenue, which rose by 339%, leading to a 137% year-over-year net increase in profits.

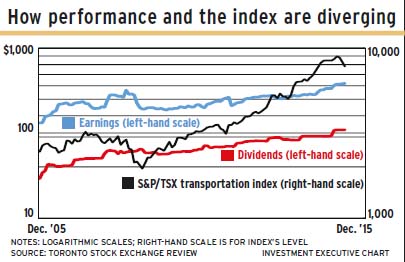

Since 2000, transportation stocks’ market-leading stock price increases have put these stocks into the “growth” category. This means dividend growth, as well as large capital gains. But the rise in the subindex now has outstripped earnings and dividends. In the five years ended May 31, 2015, the TSX transportation subindex rose by 164% while earnings grew by 92% and the indicated dividend was 79%.

Current earnings for the subindex, at $383, are historically expensive at a price/earnings multiple of 20. The multiple has been as high as 26 in 2005 and last autumn. The long-term average P/E is 15.9.

Current yields are low, ranging between 1% and 2% for most of the period between 2005 and now. Yields averaged 1.8% between 2005 and the present. Indicated dividend on the transportation subindex is $109.

As a “look ahead” mechanism, the stock market’s transportation sell-off may portend fundamental problems ahead. This is where the Dow Jones transportation average comes into play. The oldest system of market analysis works on the interplay between trends of the Dow Jones transportation average and its partner, the DJIA.

This is the age-old “Dow Theory,” a sometimes derided market indicator, but one that has never failed – although it sometimes is terribly early and sometimes terribly late in providing a bull or bear signal.

Comparing the movement of the Dow transportation average with the DJIA produces a picture of the entire market’s health. These indices produce an “ignore at your peril” signal when they diverge.

Since this year began, the Dow transport average has tracked lower while industrials have made new highs. This is a caution sign. The longer these indices diverge, the longer the market is in limbo.

If transportation stocks rally above their previous high, all will be well in the market. The sector’s cost-cutting and lower fuel costs suggest this is possible, although not certain.

© 2015 Investment Executive. All rights reserved.