Amid the stock market gloom of the past few months, there is a gleam – of gold.

Investors’ rush to safety since late last year may have ended the four years-plus bear market in gold bullion. The price of gold in Canadian dollars has jumped by 33% from its monthly closing low in June 2013 to the end of February 2016. Gold-mining shares have responded explosively.

Not everyone is impressed, though. Enthusiasm was muted at the annual Prospectors & Developers Association of Canada convention in March – maybe because overenthusiastic gold market-timers sometimes can signal a downturn in the short term. Better to wait and see.

And Finance Canada is bearish on gold. It has sold the dregs of Canada’s gold currency reserves. That’s quite a contrast to what other nations (especially China) are doing; they keep adding to their gold hoards by the ton.

Naturally, gold miners’ share prices have revived despite such caution. The weak loonie helps mightily by enhancing the price Canadian mines receive.

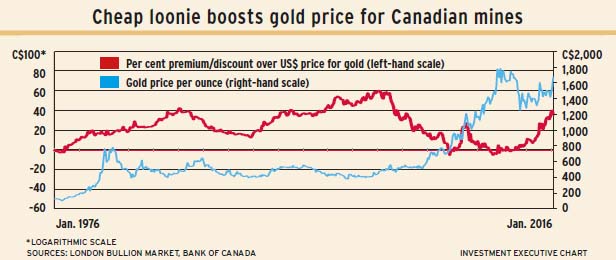

The cheap loonie is tough on snowbirds, but it benefits Canadian exporters. Products such as gold sold in U.S. dollars (US$) become much more valuable in Canadian dollars (C$) – for gold, as much as 40% more.

Gold’s base price is set in US$, with the London Bullion Market’s twice-daily fixes providing a benchmark level. In US$, gold dropped by 39% from its bull market high in August 2011 to a low in July 2015. In C$, the bullion price dropped by 30% from its high in November 2011 to a low in June 2013. Then, in mid-December 2015, gold touched short-term lows of US$1,049.40 and $1,458.29 an ounce. Within a dozen weeks, the US$ price jumped by 22% and the C$ price jumped by 17%.

With the US$/C$ exchange rate factored in, the recent price of US$1,277.50 became $1,701.76 and the S&P/TSX global gold mines index jumped by 54% from a low in July 2015. From a short-term low last November, that index rose by 49%. This spells “bull market” to gold-focused investors and analysts. The S&P/TSX GICS gold industry index, which represents Canadian mines, rose by 14% from July 2015 to the close of January. From November 2015’s close, the latter index gained by 8%.

Going into March, though, the rise was tapering off. This illuminates the picture: despite the huge, fast jump in gold share prices, the TSX global gold mining index (at a recent 181) must overcome some hurdles to make the bull market case more definite. In particular, there are three price highs between 200 and 225 on the index to be surpassed. With the market in correction mode, attempts to clear those highs may have to wait.

Gold bullion’s price surge is so recent that its effect has yet to be felt on developing and exploration gold-mining companies. Their concern is having cash on hand to enable the expansion or continuation of their work. Companies are reluctant to sell stock at still depressed prices to raise cash. Some have been willing to accept takeover offers from better financed companies.

Recent takeover events include Claude Resources Inc., a Saskatchewan-based producer, being acquired by Vancouver-based Silver Standard Resources Inc. Ontario-based Kirkland Lake Gold Inc. acquired a neighbouring producer, St. Andrew Goldfields Ltd. And Lake Shore Gold Corp., an Ontario-based mid-tier producer, is being acquired by Tahoe Resources Inc., a U.S.-based silver-mining firm listed on the Toronto Stock Exchange.

The scale of financing needed to bring proven gold resources into production is exemplified by another recent transaction. First Mining Finance Corp., a year-old Vancouver-based mining finance company, paid $10 million in stock for Toronto-based PC Gold Inc., apparently a bargain. But the formerly producing PC mine near Thunder Bay, Ont., will require $40 million to get back into operation.

Gold mining is not as significant in Canada as it used to be, but still pays substantial dividends to investors. Indicated dividends on the global gold index currently are being paid at a $1.2 billion rate, vs a high of $3.8 billion in 2013. Dividends on the gold industry index are being paid at $845 million, down from $2.4 billion in mid-2013. Earnings on the latter index peaked at $10.1 billion in 2011, but the figures are now in red – a 12-month loss of $7.8 billion.

The most recent statistics from the Mining Association of Canada show domestic gold production in 2014 totalled 150 metric tons, worth $6.8 billion. Canada accounts for about 6% of global gold production.

In the long run, forecasts of supply shortfalls sound bullish for gold mining. In 2015, Goldman Sachs Group Inc. forecast that high-quality gold deposits will become scarce within 20 years. The market’s response is to drive the price higher, making lower-quality reserves viable. There is plenty of gold not currently mineable in Canada’s bedrock.

© 2016 Investment Executive. All rights reserved.