NOW MAY BE A GOOD TIME to consider the huge potential in investing in India. That’s because recently proposed reforms to open up the country to foreign competition and lower subsidies for fuel are promising. In addition, India’s government also is making efforts to fast-track badly needed infrastructure projects.

Although the success of the country’s information-technology (IT) sector is well known, the equities recommendations from analysts include only one IT stock. Not everyone is convinced IT will continue to outperform. Charles Burbeck, head of global equities with Barclays Bank PLC‘s private wealth-management division in London, says Western companies are providing significant competition in the IT sector. And, he notes, that there has been some backlash in some countries to Indian-manned call centres.

Ironically, India’s democratic government has been a major impediment to growth. Mark Mobius, executive chairman of Franklin Templeton Investments Corp.‘s emerging-markets group in Singapore, says government corruption is the biggest challenge for India; he points to the paralysis this has produced at the national level during the past few years.

However, Burbeck is more concerned about the impediments to decision-making created by the country’s huge bureaucracy.

The other big issues, Mobius says, are inadequate availability of power; environmental issues that can hold up mining projects; and the need to import raw materials.

India’s biggest advantage is its young and growing population, with most educated people speaking English. With 1.2 billion people, India’s population is almost as large as China’s 1.3 billion; India’s higher birth rate, at 1.3% in 2011 vs 0.5% for China, means India could surpass China in population in about 15 years. The median age in India is 26.5 vs 35.9 in China, which means many Indians are only starting their careers and haven’t started accumulating assets yet.

India’s real gross domestic product (GDP) was US$4.5 trillion (US$3,700 per capita) in 2011 on a purchase-power parity basis, compared with China’s GDP of US$11.3 trillion (US$8,500 per capita).

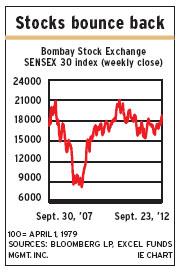

Economic growth in India has slowed this year to 5%-6%, but, says Roshan Padamadan, product specialist with HSBC Global Asset Management (Singapore) Ltd., with drops in interest rates and bank-reserve requirements, GDP growth is expected to return to 7%-8% in 2013.

Government reforms won’t have an immediate direct impact but should have indirect impact by increasing foreign investors’ interest. David Kunselman, senior portfolio manager with Excel Funds Management Inc. in Toronto, whose Excel India Fund is the largest India-based mutual fund in Canada, has seen signs of this.

The reforms include opening up the economy to foreign direct investment – to as much as 51% in retailing; 49% in civil aviation; 49% for power-generation exchanges; and 74% in broadcasting.

India’s government also has announced it will establish a national investment board under the direction of the prime minister, which will fast-track projects for which the approval process previously would have been lengthy, given multi-department jurisdictions. One project that’s expected to start soon is the US$90-billion Delhi-Mumbai industrial corridor, which will provide a freight rail line and a highway lane dedicated to trucks.

As well, plans have been announced to sell shares in state-owned natural resources enterprises; and diesel and other fuel subsidies have been reduced. These moves should help squash rumours of a possible downgrade by credit-rating agencies.

Here’s a look at some recommended stocks, which can be purchased as either American or global depository receipts:

– hdfc bank is growing at a clip of 15%-20% a year, Kunselman says, and has an attractive valuation. He notes HDFC struck a deal in January with U.S.-based Wells Fargo & Co. to offer remittance services between the U.S. and India.

A report from J.P. Morgan Securities LLC‘s Indian office has an “overweight” rating on the stock, which says, “Its immaculate quality in tough conditions will drive outperformance.”

– icici bank is the largest private-sector bank in India. Burbeck likes the stock as a general play on economic growth in India.

The bank was hit by bad debts during the global credit crisis, and concerns about its exposure to large India-based companies still weigh on its stock. But Burbeck believes these concerns are overdone and that the share price will rise as that becomes clear.

ICICI has had a complete overhaul over the past few years, Burbeck notes, that involved improving its asset quality, reducing wholesale banking and focusing more on retail, and slowing its international expansion. He says both ICICI and State Bank of India (see below) are better capitalized than many Western banks.

Kunselman also recommends ICICI stock, and a J.P. Morgan report has an “overweight” rating on it, which notes that ICICI is aiming for a 18% return on equity in three years, resulting from improved margins and further cost efficiencies. That report agrees that ICICI’s capital position is good.

– infosys ltd. is a global IT company, providing business consulting, technology, engineering and outsourcing services. Kunselman notes that Infosys has one of the largest corporate universities in the world and is one of the most cash-rich companies in India. It is still growing and looking for acquisitions, particularly in Europe.

– itc ltd. is a conglomerate that had started in tobacco, which is still its biggest product; however, ITC also has hotels; makes paperboards, paper and packaging; and has an agricultural business. Kunselman says ITC has a long track record of consistently growing earnings with low volatility.

– larsen & toubro ltd. is India’s largest engineering and construction firm. Thus, Burbeck says, it is well positioned to benefit from increased infrastructure and corporate capital spending. (L&T has US$28 billion in orders – equivalent to three years of revenue.)

However, a J. P. Morgan report is not enthusiastic and recommends “underweighting” the stock, saying that its analysts’ estimate of growth in orders this year is just 8.5% vs management’s 15%-20%.

RELIANCE INDUSTRIES LTD.’s stock has underperformed in recent years, Burbeck says, due to slow earnings growth, falling natural gas production and lack of expansion. But new refineries will start up next year, and the firm has substantial reserves in U. S. shale gas as well as in Indian gas; demand will increase as India’s stanSdard of living contiEnueXstEoclCimUb. TMENT

Still, a J. P. Morgan report has an “underweight” rating on the stock as it anticipates softening in petrochemical margins and moderating refining margins.

STATE BANK OF INDIA is Burbeck’s other bank pick and provides exposure to rural India, which, he says, is “growing far faster than the rest of the country.”

Burbeck thinks markets have overpriced their concerns about bad debts and underestimated the potential from rural growth. He also notes the bank has “salary accounts of key government establishments, which ensures a longterm source of funding.”

Although a J. P. Morgan report states the bank’s near-term performance will be challenging, it has an “overweight” rating on the stock – mainly because it’s so inexpensively priced.

TATA MOTORS LTD.’s stock has bVeeEnpunished for both the failure of its Nano car launch and because of concerns that sales in its Jaguar and Land Rover (JLR) division, acquired in 2008, would suffer in the U. S. and Europe in this sluggish economic environment.

But Tata has found offsetting JLR sales in China and Russia – and Burbeck expects Nano sales to pick up in the rural areas of India, where the car’s low price makes it affordable. He notes that the Nano hasn’t been a success in the cities, as urbanites want Western cars.

Kunselman isn’t surprised it’s taking time for Nano sales to take off – two- and three-wheelers are still the dominant form of transportation in India. He notes that, globally, Tata is the fourth-largest truck manufacturer and second-largest bus producer.

A JP Morgan report has an “overweight” rating on the stock, saying that the stock will be initially driven by JLR sales.

© 2012 Investment Executive. All rights reserved.