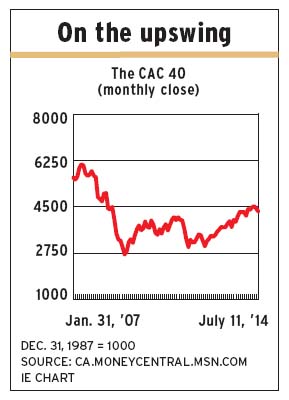

Despite the lacklustre growth prospects for France as a whole, portfolio managers are finding good investment opportunities among companies based in that country. Many of these opportunities are with global firms and, as a result, are not so much tied to demand within the nation, although some firms do operate domestically in the main.

“France is considered the sick man of Europe,” says Martin Fahey, head of European equities with I.G. Investment Management Ltd. In Dublin. “It’s a very state-protected economy, with government spending equivalent to about 50% of gross domestic product [GDP].”

And even though France’s economy is growing, its real GDP is expected to rise by only 0.8% this year. As well, unit labour costs were about 5% higher than in Germany last year; that’s in stark contrast to 1995, when those costs were 15% lower than those in Germany.

Other portfolio managers agree with Fahey. Says Charles Burbeck, co-head of global equity portfolios with UBS Global Asset Management (U.K.) Ltd. in London: “There’s been little effort to restructure the government – and [the government] doesn’t want to change labour laws. It’s not an attractive place to run a business.”

Wendell Perkins, senior portfolio manager with Manulife Asset Management (U.S.) LLC in Boston, is also concerned about the inflexible labour laws: “Government policy isn’t dealing with the broader issues of inefficiency.”

However, France’s government has lowered payroll taxes and the new prime minister, Manuel Valls, has promised not to raise taxes, to cut social charges on businesses by an additional 10 billion euros, and to create 50 billion euros in public-sector budget savings. If he can do this, more French stocks will become interesting.

Nevertheless, the aforementioned portfolio managers have found French stocks they like right now. Here’s a look at some of their picks, as well as those of Don Reed, president and CEO of Franklin Templeton Investments Corp. in Toronto and portfolio manager of the Templeton International Stock Fund, and Peter Hadden and Stephen Oler, portfolio managers with Pyramis Global Advisors in Smithfield, R.I., a unit of Boston-based FMR LLC (a.k.a. Fidelity Investments) and portfolio co-managers of Fidelity Europe Fund:

– Carrefour SA is the second-largest retailer in the world in sales, after Arkansas-based Wal-Mart Stores Inc. Carrefour has a format similar to Wal-Mart’s, but with more food products. In 2013, 47% of Carrefour’s sales were in France, 26% in the rest of Europe, 18% in Latin America and 9% in Asia.

Sales in France have suffered from increasing competition and the resulting downward price pressure. But earnings have improved as a result of restructuring by a new management team that came in two years ago. Burbeck expects further earnings’ recovery.

Analysts with J.P. Morgan Cazenove (JPMC), the European marketing arm of New York-based J.P. Morgan Securities LLC, also like Carrefour’s stock, rating it as “overweight.”

– Iliad SA is one of four main firms in the overcrowded telecom market in France. Hadden thinks Iliad will be in the best position when consolidation hits.

JPMC analysts also like the stock, rating it as “overweight.”

– Kering SA, which was known as Pinault-Printemps-Redoute, or PPR, until June 2013, has a portfolio of luxury, sport and lifestyle brands that include Alexander McQueen, Bottega Venetta, Gucci, Saint Laurent and Puma.

Normally, this stock trades at a premium, but its price has dropped off substantially because of problems at Puma and lower spending in the important luxury-goods market in China. However, Perkins says, Kering has cut costs and is dealing with Puma, which needed to refresh its product line. In addition, Perkins is starting to see signs of a stabilizing and improving economy in China.

Fahey, Hadden and JPMC analysts also like this stock.

– Legrand SA is a global leader in low-voltage electrical products and in building digital information networks for commercial, industrial and residential markets. Oler considers Legrand very well positioned for future earnings growth.

However, both Burbeck and JPMC analysts prefer Schneider Electric SA, France’s other global low-voltage company (see below).

– Michelin SA, one of Reed’s picks, is the second-largest tire company in the world after Japan-based Bridgestone Corp. Reed notes that most of Michelin’s sales are replacement tires, which is much more profitable than volume sales for new cars. Industry prospects also are good, given strong car sales in China and India – and the fact Michelin has production facilities in both countries.

– Natixis SA. Oler believes this stock’s price will rise as investors discover the value of its very large global asset-management business. Natixis Global Asset Management SA has US$900 billion in assets under management that are managed in-house or through its 20-plus affiliates in Europe, North America and Asia.

– Orange SA, formerly known as France Télécom SA, is the other strong telecom company in France. Perkins expects this firm to survive consolidation; he also notes that its dividend yield is a healthy 6% and its share price is “remarkably cheap.”

– Peugeot SA sells its automobiles predominantly in Europe, and its restructuring story is one that Burbeck likes. Peugeot almost went bankrupt 18 to 24 months ago because of weak financials and dropping market share. However, France’s government and Dongfeng Motor Corp., a state-owned, China-based company with which Peugeot has a successful joint venture, have provided capital in exchange for a 14% ownership stake each.

Peugeot also is regenerating its model lineup and cutting costs. Burbeck says a couple of new models are “doing very well.”

– Schneider Electric SA is a global leader in the low-voltage electrical market, much like Legrand. However, Oler says, Schneider has sufficiently different geographical markets and products so that a portfolio could reasonably contain both stocks – as does Fidelity European Fund.

Burbeck prefers Schneider to Legrand, noting that the former has a good track record of well-managed acquisitions and cost-cutting; he also says Schneider is a “rare example of a French company that’s very well managed and shareholder-friendly.” He believes that Schneider can grow its earnings at 10% a year for the next three to four years, given the strong demand by businesses for ways to lower energy costs.

JPMC analysts have an “overweight” rating on this stock.

– Société Générale SA. This global bank’s stock price is down as investors wait to see what kind of penalty it will get for violating U.S. embargoes against Sudan, Iran and Cuba. (BNP Paribas SA, France’s other major global bank, was recently fined $9 billion for the same infraction.)

However, Oler doesn’t think that Société Générale is in nearly as much trouble as BNP Paribas and, as a result, he doesn’t expect Société Générale will get anything like that kind of penalty.

JPMC analysts have an “overweight” rating on this stock.

– Total SA. Perkins considers this company to be a leader in the trend among global integrated oil and gas companies toward achieving greater capital discipline. In fact, he says, the company is “totally focused” on this.

Total is reining in spending and delaying or cancelling large projects for which the returns aren’t good enough. At the same time, Total still is investing for growth. Perkins particularly likes the firm’s long-term prospects, particularly in Angola.

– Veolia Environment SA. Oler likes this water and waste-management company. Its stock is a play on economic recovery in France because demand for waste management is tied to economic growth. However, he notes, water demand is not as cyclical. The result is “a good, steady income stream and a good dividend.”

– Vivendi SA is a global mass media and telecom firm that Perkins considers to be an interesting restructuring play. Vivendi, having grown through acquisition, had become somewhat unwieldy and wasn’t performing well. The firm has sold some of its positions – including its telecom business, which will be merged with Numericable Group SA, assuming the deal gets regulatory approval.

That deal will give Vivendi about 13.5 billion euros in cash, which can be used to build core assets and/or reduce debt, increase the dividend or buy back shares.

Perkins favours this company, noting that its shares still trade with a holding-company discount, which should disappear. There is execution risk, he adds, but, assuming that goes well, “the ingredients are there for a significantly higher valuation.”

© 2014 Investment Executive. All rights reserved.