If you plan to put your clients into stocks now, here is a research plan you may want to consider: look over the five sectors that are rising in price, outperforming the market and producing rising earnings.

These sectors, in order of size, are: financial services, industrials, telecommunications services, consumer discretionary and consumer staples. These sectors combined account for 51% of the S&P/TSX composite index.

There’s an element of a momentum strategy in the selection criteria. But it is always preferable to put your clients’ money into sectors that are doing better than others and rising in price.

The measurements used here are for the capped index versions of these sectors. These are the indices reported on an intraday basis by the Toronto Stock Exchange.

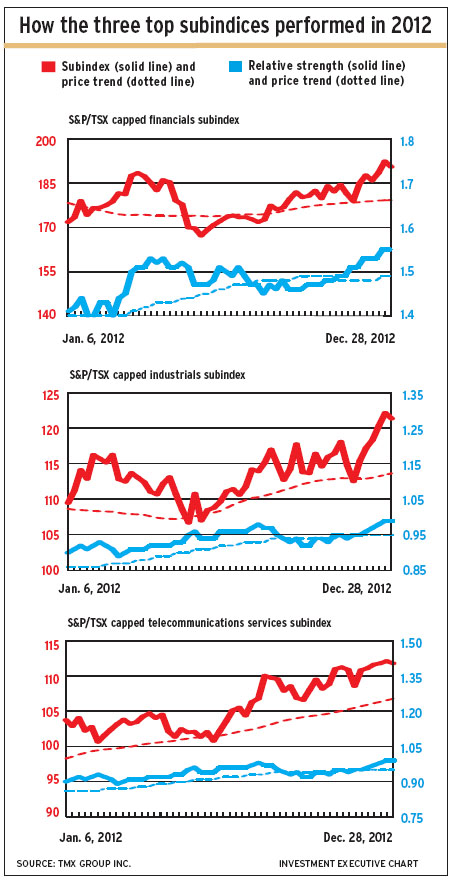

The accompanying charts for the top three performing subindices show the rising week-to-week index levels, as well as the price trend as revealed by 40-week moving averages (red graphed lines). At the bottom of each chart, the blue lines show relative strength and the trend line.

Here’s a brief look at the key trends in these sectors:

– FINANCIAL SERVICES. Earnings have made a big recovery since the stock market crash of 2008-09, but have not yet matched their 2007 high. Earnings dropped through the first half of 2012, but have risen by 11% since August to $14.47, adjusted to the index. On a year-to-year basis, they ended 2012 being down by 6%.

Dividends have advanced slowly; the sector yield has crept up to 4.1% from 3.5% early in 2011. The price/earnings (P/E) multiple dropped to 11 in late 2011, but since has risen to 13.2.

The financials sector now pays out 54% of earnings as dividends on average – a higher ratio than in the years just before the 2008-09 crash.

– INDUSTRIALS. This sector’s subindex earnings have hit bottom three times in the $5.20-$5.60 range since 2007. After dropping through most of 2012, industrials’ earnings have perked up to $6.03. They have gained by 9% since September.

Meanwhile, the average dividend has risen to $2.79, exceeding the 2008 high. The payout ratio has risen to 46% – up from 29% in 2006 – so there is indication of management confidence about this sector’s outlook.

At 122, the subindex is approaching its 2007 high of 127. The P/E multiple has pushed up to 20, the highest among the five sectors. Yield has dropped a bit, to 2.3%.

TELECOMMUNICATIONS SERVICES. In the 2009 crash, this sector’s dividend yield topped 6.5%. Now, the yield is 4.8%, but the average sector dividend has risen to $5.34. Dividend payments rose by 10% in 2012.

Sector earnings have recovered from their 2011 drop, having gained through 2012 to reach $7.27.

Telecoms have had one of the steadiest price rises since 2009 and perhaps may be overextended at present. The payout ratio has varied widely in the past few years and now stands at 74%. The sector trades at 15 times earnings.

– CONSUMER DISCRETIONARY. Earnings are volatile in this sector. The subindex, its earnings and its dividends are below their pre-2009 highs. Earnings also are below their early-2011 high. But the earnings trend is upward, rising by 68% from the recent low in March 2012.

Earnings on this subindex are $5.23. This sector has a long way to go to match its earnings high of more than $8 in 2008.

Dividends gained by almost 4% in 2012, to $2.55, for a 49% payout ratio. The dividend trend is flat, with the current payment almost the same as it was in late 2009.

The P/E multiple dropped to 18.4 during 2012 from a high of 30.

– CONSUMER STAPLES. For steady earnings growth, this sector is a recent leader, increasing by 10% in 2012 to $16.04. In 2007, earnings dropped to as low as $6.

The dividend has been rising, too. At $4.52, it is 20% higher than at yearend 2011. The dividend rose above $3 in 2006, then climbed to $4 in May 2012.

This results in a low dividend yield, currently 1.8%. The yield hasn’t changed much over the past six years: it has briefly been as high as 2.2% and as low as 1.4%.

Over the same six-year period, the P/E multiple for consumer staples has dropped to 15. However, it reached as high as 33 in 2007, which makes the sector look inexpensive now.

© 2013 Investment Executive. All rights reserved.