Although international equities markets have fared well in the past 12 months, volatility has increased lately on three fronts.

First, there is Greece’s unending debt crisis which appeared to be on the road to resolution at the time of writing, although the result remains fluid. Second, frothy China’s equities markets corrected sharply until Chinese authorities intervened. Third, markets are weighing the likelihood of the U.S. Federal Reserve Board finally raising interest rates.

Still, portfolio managers remain undeterred, suggesting that volatile conditions may yield buying opportunities.

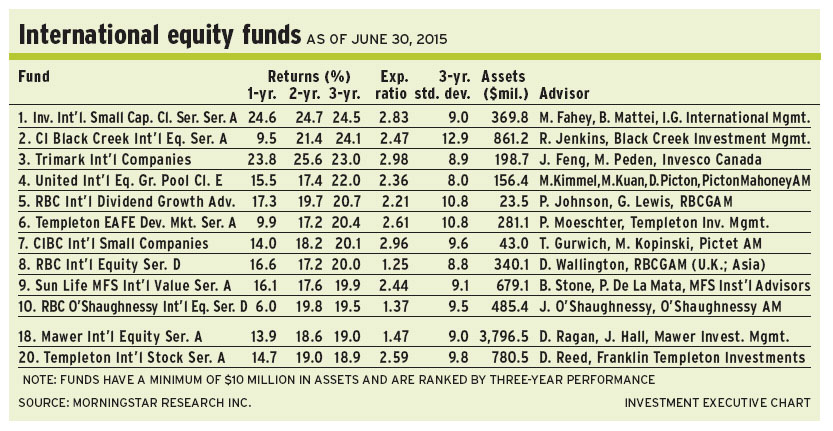

Massive liquidity and monetary easing by central banks is the principal cause behind rising markets, argues David Ragan, a director at Calgary-based Mawer Investment Management Ltd. and portfolio co-manager of Mawer International Equity Fund.

“There are a lot of problems in the world and lots of concerns, and not a lot of growth, even in the U.S.,” says Ragan. “But central banks – initially in the U.S., followed by Europe and Japan and China – have been putting a lot of money into markets. That money is available very cheaply and driving up [the value of] financial assets.”

Ragan acknowledges that Greece’s debt crisis still may hurt weak eurozone players such as Italy and Spain: “I think it’s positive for the long-term viability of the euro that it’s been shown that members can be kicked out of the union. This should help motivate member countries to adhere to the union’s fiscal rules much more closely or risk giving up the euro or their sovereignty.”

Had Greece left the eurozone and created a new currency, Ragan notes, companies with unpaid bills from Greece would have felt the pain. That is mostly not an issue for the funds he manages, he says: “There shouldn’t be any big surprises – at least, among the companies that we own in our portfolios, since they have been asking to be paid up front.”

Meanwhile, Ragan argues, valuations are moderately high, with European stocks trading at price/earnings ratios of about 16. “If interest rates in developed markets are around 1%, you’re probably getting a 6%-8% return from stocks,” he says. “That’s a pretty good spread – but it’s contingent on rates staying low.”

The biggest risk is a significant spike in interest rates, which would make stocks look expensive.

A bottom-up investor, Ragan has allocated about 61% of the Mawer fund’s assets under management (AUM) to Europe, 26% to Asia, 7% to North America-listed U.K.-based companies, 2% to Australia and 3% to cash.

From a sector standpoint, 20.3% of AUM is in consumer defensive (vs 10.9% in the benchmark MSCI Europe Australasia and Far East index), 19.1% is in financials (vs 25.8% in the index), 18.7% in industrials (12.7%) and smaller holdings in sectors such as health care and basic materials.

One top holding in the 56-name Mawer portfolio is China Mobile Ltd., the world’s leading cellphone service provider. China Mobile’s stock had been under pressure because of the firm’s reliance on a 3G network. But after standards for a 4G network were approved last year, Ragan bought the stock in the spring of 2014.

China Mobile’s Hong Kong-listed stock is trading at about HK$101.30 ($15) a share. There is no stated target.

The prospect of the fed raising rates is self-evident, agrees Jeff Feng, vice president, Trimark Investments division, at Toronto-based Invesco Canada Ltd., and lead portfolio manager of Trimark International Companies Fund.

“It’s likely to happen in the second half of this year and is priced into markets,” says Feng. He notes that Janet Yellen, chairwoman of the Fed, has said the pace of rate hikes would be “slow and measured.”

As for frothiness in China’s markets, Feng expresses caution about so-called New Economy stocks that are trading at 100 times earnings and higher. “If you don’t think that’s a bubble, I don’t know what is,” says Feng, adding that there are some exceptions in China’s markets and that he has found a few stocks of good value.

Turning to Greece’s debt crisis, Feng admits there is much uncertainty: “All the politicians are doing is kicking the can down the road. The situation is not sustainable. You are also creating a bad example for other eurozone countries.”

Moreover, Feng is puzzled why European stocks command high valuations compared with cheaper emerging markets equities, which many investors are shunning: “Maybe it’s OK to chase momentum if you are a short-term investor. But, fundamentally, you should have concerns about Europe. It’s purely driven by quantitative easing.”

A bottom-up stock-picker, Feng has allocated about 43% of the Trimark fund’s AUM to Asia, which includes 23% of AUM to Greater China, 7.5% to Japan and 6.5% to South Korea. There is also about 54% in Europe, of which almost half is in the U.K., and 3% in cash.

Feng is bullish on consumer defensive stocks, which account for 28.4% of AUM. There is also 18% in industrials and 11.5% in consumer cyclical.

One recent acquisition in the 45-name Trimark fund is SoftBank Corp., a Japanese telecom and Internet firm with diversified interests, including holdings in U.S.-based wireless carrier Sprint Nextel Corp. and China-based e-commerce player Alibaba Group Holding Ltd. Although SoftBank’s market capitalization is US$70 billion, the firm’s various investments are worth US$90 billion in aggregate.

“You can get that 35% stake in Alibaba at 14 times earnings, whereas Alibaba itself is trading at 27 times forward earnings,” Feng says. “So, you are getting Alibaba at a huge discount.”

SoftBank stock is trading at 7200 yen ($70.50) a share. Feng has a target of 9,000-10,000 yen within an unspecified time frame.

Looking at valuations, Asia ex-Japan is the world’s cheapest region, says Don Reed, president and CEO of Toronto-based Franklin Templeton Investments Corp., and lead portfolio manager of Templeton International Stock Fund.

China and Hong Kong stocks, for example, are trading at about 12.6 times earnings.

“Japan is more expensive, but it’s not trading at 75 times, the levels that occurred 20 years go,” says Reed. “It’s falling more in line [with other markets].”

Europe is the second-cheapest region, with stocks trading at 16 to 16.5 times earnings. And what’s interesting about Europe, says Reed, is that many companies have a lot of cash on their balance sheets. That cash can be returned to shareholders through dividends, share buybacks or acquisitions.

As for Greece, Reed does not believe that the country will be pushed out of the eurozone. And because of Greece’s small size, its departure, should it ever happen, may not be a major concern.

“That impact is not as big as the psychological impact that may be felt by some people,” says Reed, adding that he believes a last-minute resolution is possible. “It’s a lot of noise. It’s the psychological impact [that matters].”

Reed like his peers, believes that if interest rates rise in the U.S. in a measured fashion, there won’t be much impact on markets. More to the point, a rate hike will indicate the Fed is exhibiting confidence in the U.S. economy.

Reed is bullish on his investment prospects, and has allocated about 15.5% of the Templeton fund’s AUM to the U.K., 14% to China, 11% to Japan, 8.7% to Germany and smaller weightings to countries such as France.

From a sector standpoint, financials are the largest weighting in the Templeton fund, at 25.6%, followed by 5.6% in health care and 13.1% in telecom, with smaller holdings in industries such as energy.

One top name in the 58-name Templeton portfolio is GCL-Poly Energy Holdings Ltd., a Hong Kong-listed maker of solar-grade polysilicon (a feedstock material used in solar energy applications) and polysilicon wafers. “[GCL-Poly has] a 20% world market share and [is] the lowest-cost producer,” says Reed, a bottom-up stock-picker. “We are expecting growth of about 20% per annum.”

GCL-Poly stock is trading at about HK$1.80 ($0.25) a share, or at 13.4 times trailing earnings. Based on a five-year outlook, Reed expects the stock price to double.

© 2015 Investment Executive. All rights reserved.