CANADIAN SMALL- AND MID-cap stocks have been under considerable pressure due to weak commodity prices and uncertainty about the strength of domestic economies. Yet, fund portfolio managers generally remain upbeat in the belief that selective opportunities are attractive.

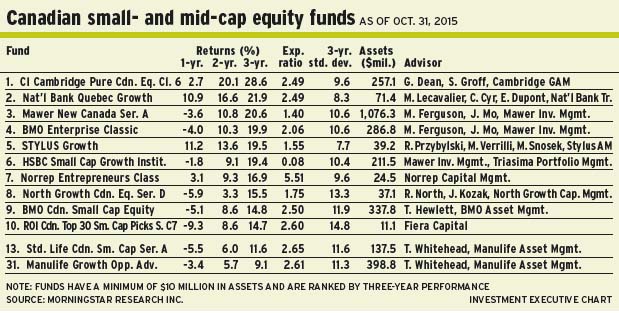

“The Canadian small- and mid-cap market is momentum-driven and lacks diversity of quality companies,” says Greg Dean, principal at Cambridge Global Asset Management, a unit of Toronto-based CI Investments Inc., and portfolio co-manager of CI Cambridge Pure Canadian Equity Fund. He shares portfolio-management duties with Stephen Groff, another principal of Cambridge.

“When you see these violent moves in the asset class, they usually are exacerbated in both directions,” says Dean. “When times are great, people get excited about a bunch of below-average companies and a few very strong, well-run businesses that happen to be listed in Canada. What we’re seeing this year is the opposite.”

As a result of the market’s gloomy mood, “world-class companies are getting thrown out – along with the companies that deserve to return to valuation reality,” says Dean. “The average companies were being lifted up by the world-class companies.”

However, Dean does not think the market is overreacting. Rather, the situation is a case of a few companies making headlines. Moreover, even if those high-priced companies have declined in value, Dean believes, there is more to come. At the same time, the bearish mood has resulted in attractively priced companies in the energy, industrials, health-care and consumer staples sectors.

A bottom-up investor, Dean is reluctant to forecast when the market will touch bottom. He prefers to take advantage of declines to pick up individual stocks. “You’re not dating these stocks; you’re marrying them,” he says. “It’s important to do a lot of homework up front – and [to] be very patient.”

The CI fund holds about 30 names. About 78% of the CI fund’s assets under management (AUM) is in Canadian stocks, 10% is in non-Canadian, and 12% is in cash. About 27% of AUM is a blend of consumer cyclical and staples names; energy represents 22%; industrials, 16%; and financials, 12%; with smaller holdings in sectors such as information technology (IT).

One top holding is Finning International Inc., the largest Caterpillar equipment distributor in Canada, which has seen a change in its management team. [“Finning has] focused on generating returns as opposed to generating top-line growth,” says Dean, noting that the stock has a 4% dividend yield. Although earnings have dropped this year, Dean still expects that the free cash-flow yield will be almost 10%.

Finning stock is trading at about $20.30 a share. There is no stated target.

The market rout began early this year in the energy sector, says Tyler Hewlett, vice president at Toronto-based BMO Asset Management Corp. (BMOAM), and lead portfolio manager of BMO Canadian Small Cap Equity Fund. He shares portfolio-management duties with David Taylor, portfolio manager at BMOAM.

“[The bearish mood] now is more widespread because, with pressure on North American markets, we’ve had this general equity weakness,” says Hewlett.

Hewlett notes that the benchmark S&P/TSX small-cap index is down by about 12% year to date: “There’s been a general malaise.”

Hewlett agrees with Dean that almost all small- and mid-cap stocks are being tarred with the same brush. The causes are attributable to factors such as uncertainty surrounding the direction of interest rates and concerns about the weakness in the energy sector. Yet, turning to the U.S. economy, Hewlett notes that the situation is not so bad, based on observation of portfolio holdings in that market.

“The environment seems pretty constructive – unless, of course, we go into a recession. But we’re not seeing many signs of that,” says Hewlett. “We focus on the company fundamentals and we’re seeing very strong end-markets for the majority of our holdings.”

As long as that pattern persists, he believes, the market will recover. “But if those fundamentals deteriorate, which we’re not seeing any signs of,” he adds, “then the market will remain volatile for a while.”

About 5% of the BMO fund’s AUM is in cash. Financial services account for 25% of AUM; consumer discretionary, 19%; IT, 18%; industrials, 14%; energy, 13%; and there are smaller holdings in sectors such as materials.

One favourite stock in the 50-name BMO fund is Altus Group Ltd., an information provider that is regarded as the “Bloomberg” in the real estate industry. “Commercial real estate owners use [Altus] to value properties or for tax-planning purposes and return attribution,” says Hewlett.

Altus is under new management and generating 20% earnings-per-share growth year-over-year. Altus shares, which have a 3.2% dividend yield, are trading at $18.75 each. The 12-month target is about $25 a share.

The market is forming a bottom, argues Ted Whitehead, senior managing director at Toronto-based Manulife Asset Management Ltd., and lead portfolio manager of Manulife Growth Opportunities Fund and Standard Life Canadian Small Cap Fund (the latter of which he began managing last June).

“Oil had dropped as low as US$38 a barrel in August. Oil then went up to US$48 and, as indices corrected in September, oil went down to US$44. So, it set a higher low. That’s what you look for as an indication of a turnaround,” says Whitehead. “We’ve had a new relative high, since this bottoming process started. [The recovery] won’t be a V shape. I’d say that the worst is probably over.”

Meanwhile, he notes, there is genuine concern about the strength of global economies, as the International Monetary Fund has lowered its forecast to 3.1% global gross domestic product growth after forecasting growth as high as 3.5% last summer.

“There is a global growth fear. Our stocks [in Canada] are more cyclical. But what people forget is that 85% of our exports go to the U.S. If the U.S. is still muddling along and doing better, which is our view, then Canada has probably finished with that mild recession [recorded early in 2015] and things are likely to improve moderately as we move toward yearend and into 2016.”

Did our markets drop too far? Possibly, Whitehead concedes. But he also argues that when coming out of a recession, there is more money to be made in small-caps than in large-caps. He adds that there is some debate over which sector will show leadership when markets inevitably rebound.

“Are we seeing an inflection point, where materials and energy will do better, and will the Canadian dollar get stronger? In my view, the leadership prior to the correction will take over come November and December,” says Whitehead, noting that health-care, IT and industrial firms that benefit from demographic trends and generate earnings in the U.S. will resume leadership roles.

Both the Manulife and Standard Life funds have about 17.1% of their AUM in IT; 14.6% in industrials; 11.8% in energy; 10.3% in financials; and smaller weightings in health care and consumer staples.

A top holding in both the Manulife and Standard Life portfolios is Richelieu Hardware Ltd., which supplies parts to kitchen cabinetmakers and hardware retailers.

“The story is home renovation, which is on the uptick. And new-home sales in the U.S. also are growing,” says Whitehead. “[Richelieu has] beaten earnings in six of the past seven quarters. Analysts also have revised their earnings [forecasts] upward to a little over 11% for the next quarter.”

Richelieu stock is trading at about $71.90 a share, or about 23.5 times forward earnings. Although that multiple is high, Whitehead notes, Richelieu is growing by almost 20% a year. The target in the next 12 to 18 months is $80 a share.

© 2015 Investment Executive. All rights reserved.