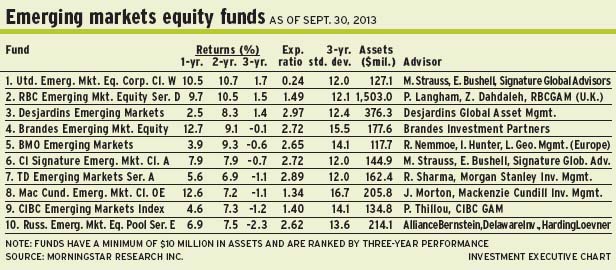

Emerging-markets stocks took a beating early this past summer, when they endured a double whammy in the form of concerns about faltering economic growth in China and the impact of higher interest rates in the U.S. Although the pressure has eased somewhat, there is uncertainty about short-term prospects, so fund portfolio managers urge investors to take a longer-term view.

“There were four reasons for the downturn in the first half of the year,” says Zeena Dahdaleh, associate portfolio manager at London-based RBC Global Asset Management (U.K.) Ltd. (RBCGAM) and portfolio co-manager of RBC Emerging Markets Equity Fund. (She shares portfolio-management duties with Philippe Langham, head of emerging-markets equities with RBCGAM.) “Growth forecasts have been lowered in China, and there also were concerns about the pace of credit growth. The second concern has been the U.S. dollar [US$]. Historically, emerging-markets equities underperform during periods of US$ strength. Third, weak earnings momentum was a cause for concern. Last, higher U.S. bond yields led to a sell-off of emerging-markets bonds, which led to rising funding costs and, ultimately, hit local currencies.”

Today, however, there are reasons to be more positive, Dahdaleh argues: “Recent data points on China say that growth momentum is reaccelerating. Of course, the credit cycle remains an issue, but we expect to see slower credit growth in the coming years, which will help rebalance China’s economy and move away from [infrastructure] investments and lead to higher-quality growth.”

In addition, although the US$ is currently strong, Dahdaleh believes that over the longer term, many emerging-markets currencies are undervalued. “We see a strong case for longer-term appreciation of local currencies,” she says, “given the superior economic fundamentals, higher foreign exchange reserves and current-account surpluses.”

Dahdaleh notes that earnings momentum has begun to improve; although higher bond yields are a concern, most economies are strong enough to support those yields. And valuations have improved as the discount to stocks in developed markets has expanded to 20% from 12% at the start of the year.

Dahdaleh says that clients should focus on the longer term: “We are very positive, because of the faster economic growth, attractive demographics and a rising middle class.”

The RBC fund is fully invested; about 20% of its assets under management (AUM) is in financials, 14.7% is in consumer staples, 14% is in consumer discretionary and smaller weightings are in sectors such as telecommunications. “We have a preference for stocks that have a bias toward domestic growth,” says Dahdaleh. “Fi-nancials and consumer stocks are primary beneficiaries of this theme.”

A top holding in the 60-name RBC fund is India-based Housing De-velopment Fi-nance Corp. Ltd., a major residential-mortgage lender with growing market share. The stock is trading at about 798.7 INR ($13.40) a share. There is no stated target.

But it may be time to be guarded, argues Matthew Strauss, vice president at Signature Global Advisors, a unit of Toronto-based CI Investments Inc., and portfolio co-manager of CI Signature Emerging Markets Class Fund. (He shares portfolio-management duties with Eric Bushell, Signature Global Advisors’ chief investment officer.) For years, Strauss notes, stocks benefited from so-called “easy money,” thanks to central banks’ policies in developed markets.

“It was a ‘rising tide’ situation — until last summer,” says Strauss. “Now, we are on the other side of that tide. There are concerns that credit will be more expensive and not so easy. It could be a foretaste of what’s to come.”

Although markets have recovered somewhat lately, Strauss cautions about the near term: “If the U.S. economy picks up, it will give stability to global growth. But that’s when [U.S.] Federal Reserve [Board] will start its tapering program.”

More important, he adds, it means clients must become much more choosy: “Being selective was not essential during the ‘incoming tide’ period. Whether it was a weaker country that was not committed to structural reforms or a strong country didn’t make much of a difference. Now that we are on the other side, it will make a big difference — and continue to do so.”

Strauss, a portfolio manager who blends top-down and bottom-up investment styles, points to vulnerable countries such as Brazil, South Africa and India. “We have to pay special attention to [these countries ]when the Fed starts to taper because they’re in need of capital inflows,” he says, noting that bond yields have risen in these countries and their currencies have been under pressure. “The fear of tapering is partly priced into the market. But we know that rates also are higher and will affect domestic growth.”

About 15% of the CI fund’s AUM is in cash, and Strauss admits he is cautious: “We don’t see an imminent crisis. But it’s probably better to have cash to deploy at the right opportunity.”

In terms of sectoral exposure, 24% of AUM is in financials, 13.3% is in information technology, 11.1% is in consumer discretionary, with smaller weightings in areas such as industrials and energy. Asia accounts for 50% of AUM; Latin America, 18%; and Eastern Europe/Africa/Middle East, 16%.

One favourite in the CI fund (which holds about 110 names) is Ayala Corp., a Philippines-based firm with interests in banking, property development and telecom. “Like many conglomerates, it trades at a discount,” says Strauss. “But we are finding more value in it than the sum of its parts.”

Ayala stock trades at about 615 PHP ($14.70) a share, or 23 times forward earnings. “It’s expensive, but it’s based in a high growth market,” Strauss says. There is no stated target.

Clients should take a longer-term view and bear in mind that many emerging-market companies are in good shape, says Rasmus Nemmoe, senior portfolio manager, global emerging-markets equities, with London-based Lloyd George Management (Europe) Ltd., and co-manager of BMO Emerging Markets Fund. (He shares portfolio-management duties with Irina Hunter, senior portfolio manager at Lloyd George.)

“For instance,” says Nemmoe, “most of the companies in the Southeast Asia region spent the past decade deleveraging. They learned their lesson during the Asian financial crisis in 1997-98. What we have today is a region [in which] most of the companies, in aggregate, have pretty solid balance sheets.”

Moreover, Nemmoe adds, consumer borrowing is low relative to developed markets, sovereign-bond ratings have seen upgrades and bonds issued by countries such as Indonesia and, more recently, the Philippines have acquired investment-grade status.

Still, Nemmoe acknowledges, emerging-markets equities have been hit despite their solid fundamentals: “The sad fact is that the asset class [is] inversely correlated to the US$, which is a function of the Fed’s monetary policies. Whenever you have this speculation that the Fed will taper its expansionary monetary policy, you will see some market volatility. But that contrasts with the fundamentals that we see, both on the bottom-up, corporate level and also, to some extent, in many countries on the sovereign level.”

Nemmoe agrees that it’s time to be selective: “Look at China, for instance: the investment-driven growth model is driven by [sovereign debt] expansion [but that debt] is expanding at a faster pace than the ability to service it. At some stage, this has to wind down. And once growth slows meaningfully, you will also see corporate earnings contract even further. As an investor, you need to be more selective and disregard the benchmark or index levels.”

Nemmoe has allocated about 29.2% of the BMO fund’s AUM to financials, followed by 17% to consumer cyclical stocks, 14.5% to communication services and 12% to consumer defensive. There are smaller weightings in sectors such as technology. About 65% is in so-called Greater Asia, 13% is in Eastern Europe/Africa/Middle East and about 20% is in Latin America.

Running a portfolio with about 50 holdings, Nemmoe focuses on companies that generate high, sustainable returns on invested capital over a business cycle and have predictable cash flows.

One top holding in the BMO fund is Universal Robina Co., a Philippines-based maker of consumer staples such as biscuits, snacks and instant coffee.

Universal Robina stock trades at about 130 PHP ($3.10) a share. There is no stated target.