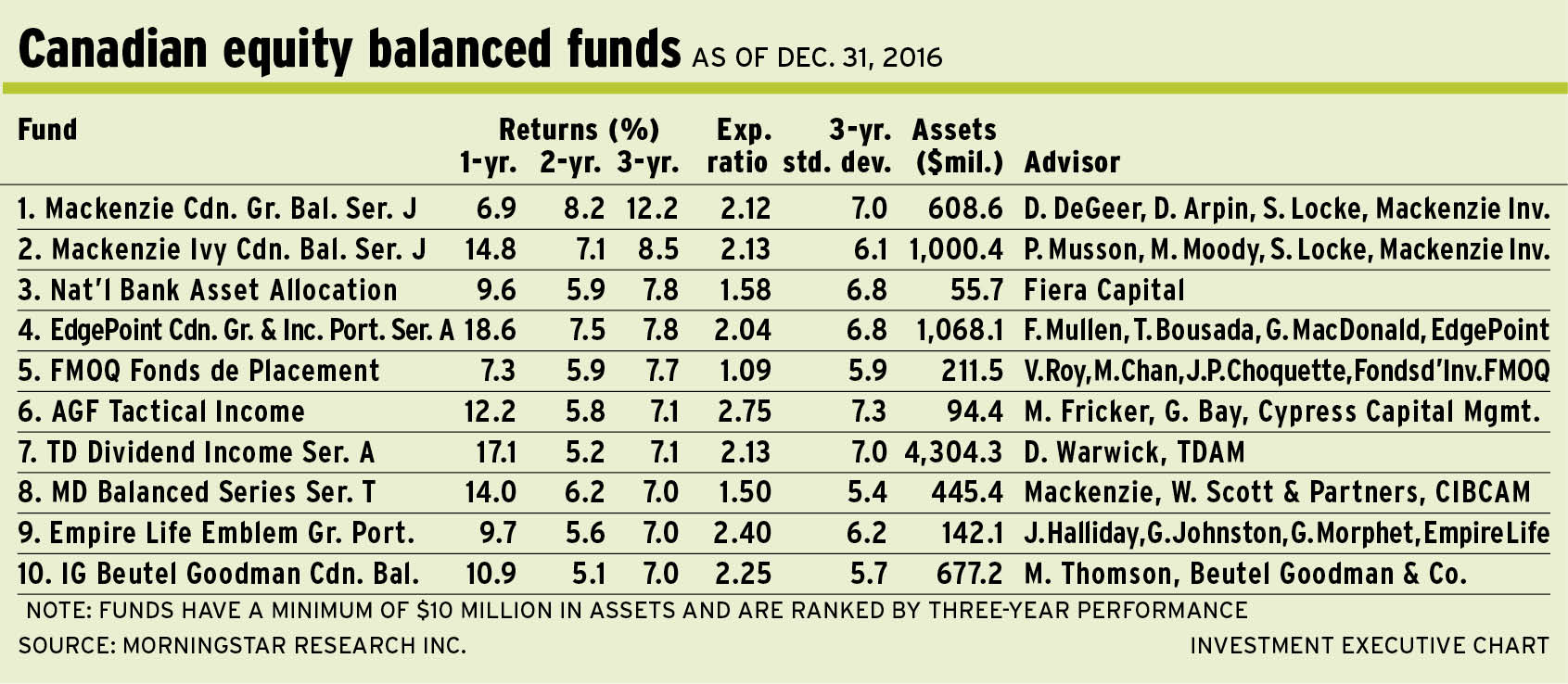

Canadian equity balanced funds generated high single-digit returns in 2016, as resources stocks rebounded on growing strength in North American economies and yields on fixed-income securities began to recover from their downward trend.

Yet, Donald Trump’s win in the U.S. presidential race has sent a mixed message: bonds have seen some losses due to yields perking up on expectations of fiscal spending; and equities have edged upward on the promise of growth. For portfolio managers, this is a time to tread carefully and juggle the two asset classes.

“We do expect that Trump’s victory and pro-growth agenda will be positive for the U.S. economy and markets,” says Michael Fricker, a portfolio manager who co-manages AGF Tactical Income Fund at Vancouver-based Cypress Capital Management Ltd. (a unit of Toronto-based AGF Investments Inc.). He works with Greg Bay, portfolio manager with Cypress.

“Yes, [Trump’s] policies should be broadly inflationary, whether that is due to lower taxes, fiscal stimulus, trade protectionism or immigration policies. On the back of this, we expect bond yields to continue rising,” says Fricker. Benchmark U.S. 10-year treasuries are yielding 2.5%, up by about 80 basis points (bps) since last autumn.

Much depends, however, on what Trump delivers in contrast to his campaign promises. “It’s important to recognize that a number of his policies may not be implemented,” says Fricker. “If they are, they may be implemented in a watered-down form.”

For example, Trump talked about reducing business taxes to 15% from almost 40%. However, the tax rates may be reduced to 25% instead. “They may be more in line with tax rates in members of the OECD,” says Fricker.

Interest rates are a greater concern, and the trend definitely is upward. “Ten-year U.S. treasury yields [are unlikely to] break through the 3% mark in three to six months,” says Bay. “The timing is always a little tricky. We expect that the policies will be inflationary and growth-oriented. The markets obviously will discount that, as they have with the rise in rates in November. The 3% mark is not out of the question.”

The Federal Reserve Board raised short-term interest rates by 25 bps in December and noted that it is likely to hike rates two to three more times in 2017.

Overall, Fricker says, his firm is cautious about Canadian markets: “We may see benefits from our own government infrastructure spending and, of course, our exports will benefit from a stronger U.S. economy.”

Fricker says his firm is more bullish on the U.S.: “But on the flip side, now we have trade concerns because Trump is talking about tearing up [the North American free Trade Agreement (NAFTA)]. I don’t think Trump will tear it up, although he will engage in discussions to tweak or modify the agreement.”

Fricker and Bay are cautious on bonds and have about 13% of the AGF fund’s assets under management (AUM) held in fixed- income, as well as 9% held in preferred shares and 4% in cash. The average duration for the bond component is three years, vs 7.2 years for the FTSE TMX bond universe index. But the pair are bullish on equities, which account for 74% of AUM.

Trump’s intentions to spend large on infrastructure and lower taxes are expected to fuel U.S. economic growth at a faster rate than if Hillary Clinton had won the election, says Doug Warwick, managing director of Toronto-based TD Asset Management Inc., and lead portfolio manager of TD Dividend Income Fund.

“[Trump’s election win] has pushed up interest rates quite a bit. But the outlook is better for the U.S. economy,” says Warwick. Higher interest rates typically help Canadian banks, Warwick adds, because they ease pressure on net interest margins. “The worry that interest rates will drop to zero, or even negative numbers, and stay there for years seems to have lessened.”

Warwick notes there is much talk about U.S. protectionism, and the likely targets will be China or Mexico. “The target is not really Canada. It’s more Mexico. Even if NAFTA was eliminated, we would fall back to the free trade agreement [previously negotiated] with the U.S. [alone].So, if Trump peels back one agreement, in theory the other should still stand,” says Warwick, adding that there is usually a sizable gap between presidential campaign talk and the realities of government. “Maybe [the gap] is a hope, or a belief, but Canada should do reasonably well with a stronger U.S. economy.”

Warwick, like Fricker, is bullish on markets for 2017: “We expect continued growth. Trump’s platform is expansionary. In the U.S., unemployment levels are down to 1973 levels, although wages are not as good as they were a few years ago. If you can continue to expand the U.S. economy and are close to full employment, that should lead to some wage inflation. That’s really good for the consumer.”

Still, Warwick says, there are risks on the downside, in the form of protectionist measures that become excessive: “How far the U.S. goes [is key]. If there are a lot of tariffs and retaliatory moves around the world, that will slow global gross domestic product.”

Another risk exists in the form of interest rates increasing by much more than expected. “A relatively small increase in rates brings us back toward a level where we should be,” says Warwick. “I’m not concerned that rates will spike extremely high. But there is a risk that it will happen.”

Despite significant market changes, Warwick has kept about 81% of the TD fund’s AUM in equities and income trusts, with 18% held in bonds and 1% in cash. On the fixed-income side, 52% of that portion is in corporate bonds, 39% is in governments and 9% is in high-yield bonds. The average duration is 7.15 years.

On the equities side, Warwick favours financial services, which account for 47% of total AUM, followed by energy (8%)and utilities (7%). “[The allocations] go back to our bottom-up approach,” he says. “We’re looking for less cyclical companies, with above average returns on equity and growing free cash flow, which leads to growing dividends and strong balance sheets.”

Forecasting where stocks may go is a mug’s game, considering that very few people predicted that Trump would be elected, says Frank Mullen, a portfolio manager with Toronto-based EdgePoint Investment Management Inc., lead portfolio manager of EdgePoint Canadian Growth & Income Portfolio. He shares portfolio-management duties with Tye Bousada and Geoff MacDonald, principals at EdgePoint.

“Not many people called for a Trump victory. And if they did, I don’t think anyone would have said that it would be so positive for the stock market,” says Mullen. “The market is proving to us that most people were unable to predict how positive certain investments would have responded.”

A bottom-up stock-picker, Mullen sees opportunities in market volatility, such as that caused by the U.S. presidential election. “As someone who looks at a stock as ownership in a business, volatility is a gift,” says Mullen. “Fundamental investors can try to decipher whether or not that [volatility] is noise or has a fundamental impact on the merits of a business. When we see dislocations between price and value, we can make an investment decision. Anytime there is volatility, there is an opportunity for someone who looks at stocks from a business-centric standpoint.”

Mullen argues that because what Trump will achieve in the short term is unclear, EdgePoint is examining buying opportunities in investment categories that are not performing well and possibly taking profits in stocks that have done well lately.

“Day-to-day movements create opportunities, he says. “If a stock declines in the short term, that’s an area where you can either increase your conviction or use as an opportunity to re-allocate [portions of] the portfolio to some names that have declined in the past while.”

About 67% of the EdgePoint fund’s AUM is held in equities and 33% is in fixed-income, vs an internal target of 70% equities and 30% bonds. The average duration for the bond component – entirely composed of corporate issues – is 2.8 years. “We still believe that, based on where rates and credit spreads are now, vs equities valuations, we can generate better long-term performance in equities markets.”

© 2017 Investment Executive. All rights reserved.