Natural resources stocks performed well in 2016, but this year is proving to be more challenging. Markets are nervous about fluctuating oil and gas prices, and China’s move to tighten credit could choke off demand for commodities. Fund portfolio managers are counselling patience, and they point to promised production cuts in oil and gas as an indicator of better days ahead.

“China loosened credit in mid-2015 and commodities had a nice upward run until about the end of 2016,” says Brahm Spilfogel, vice president at Toronto-based RBC Global Asset Management Inc. (RBCGAM), and portfolio co-manager of RBC Global Resources Fund. “But since mid-2016, China began to tighten again, which has affected demand for domestic housing and lending and, by extension, demand for metals.”

As a consequence, adds Spilfogel, the equities markets have become nervous about the risk of further tightening, and the malaise has raised doubts in the minds of many investors.

The problem, Spilfogel says, is that China accounts for up to 60% of global demand for various industrial commodities – such as iron ore and copper – and this has a major impact on prices for raw materials.

“We’re about halfway into this slump, during which markets are going sideways. Until we see a reasonable growth rate in demand [from China], the nervousness in the markets is likely to continue,” says Spilfogel, who shares portfolio-management duties with Chris Beer, vice president at RBCGAM.

Still, Spilfogel doesn’t believe the current uncertainty will last long. Eventually, he says, “The commodity space will benefit from nice, steady growth in demand – barring, of course, a global recession.”

As for the dynamics for crude oil, an industry for which China is less of a factor than that country is in the materials space, Spilfogel notes that the oil price weakened this spring, in part due to excess shale production from the Permian Basin in Texas and New Mexico. However, he believes, the supply/demand situation appears to be improving with the expectations of an agreement in late May between OPEC and other global producers that the production cuts agreed to in November 2016 will be extended for nine months.

Spilfogel believes the price of oil – now about US$46 a barrel – should be US$55-US$60. “It’s moving in that direction,” he says. “At US$50 a barrel, making money is very hard for many North American producers. So, the price has to go higher to generate more supply.”

Spilfogel’s outlook for the resources sector is positive. He notes that valuations are more attractive in the mining industry than in the oil and gas space: “Oil and gas stocks are fairly valued to overvalued. But, over time, they will probably grow into their multiples.”

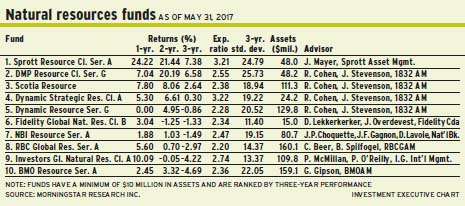

About 52% of the RBC fund’s assets under management (AUM) is in materials stocks (vs 43% for the fund’s internal benchmark) and 45% in energy (vs 56% for the benchmark). The RBC fund has about 83 holdings.

A bottom-up stock-picker, Spilfogel likes names such as Texas-based Pioneer Natural Resources Co., which produces about 235,000 barrels of oil equivalent a day from Permian Basin.

“We expect production [in that region] to grow at a 15% rate compounded over the next five to 10 years,” he says.

Admittedly, Pioneer stock is expensive, as it trades at 10.5 times enterprise value (EV) to earnings before interest, taxes, depreciation and amortization (EBITDA). “But, given the company’s growth rate, we expect the multiple will compress over time,” Spilfogel says.

Pioneer stock is trading at about US$173.30 ($229.10) a share. Spilfogel has a target of US$220 over 12 to 18 months.

Another favourite is Toronto-based Lundin Mining Corp., a copper, lead and zinc producer with mines in Chile, Spain, Portugal and the U.S. Lundin recently received US$1.5 billion from Freeport-McMoRan Inc. for Lundin’s stake in a copper mine in the Democratic Republic of the Congo. “Lundin has one of the better management teams around. [The company has] a great balance sheet. We’re not worried that [management] will invest the money in something that doesn’t make sense.”

Lundin stock is trading at about $7.35 a share, or 4.9 times EV to EBITDA. Spilfogel’s 12- to 18-month target is $9 a share.

Last year, markets rebounded on a so-called “trifecta” of recovering commodity prices, companies lowering costs while improving balance sheets, and money returning to the sector, with valuations rising, says Darren Lekkerkerker, portfolio co-manager of Fidelity Global Natural Resources Fund, sponsored by Toronto-based Fidelity Canada Asset Management ULC.

“That helped to produce really nice returns last year,” says Lekkerkerker, who shares portfolio-management duties with Joe Overdevest, portfolio manager with Fidelity. “But this year, not much has changed, although people are nervous.”

One thing that is making investors jittery is China’s appetite for metals and minerals. “Last year, the Chinese stimulated demand. This year, they’re pulling that back,” Lekkerkerker says. “China is a command economy and, for the next few years, it will be OK. [China’s economy] is slowing from a very fast rate of growth, but still has a decent growth rate – 6.7%. And demand for resources is continuing to grow.”

Another factor is uncertainty in the U.S. about the outcome of the pro-economic growth policies of President Donald Trump. “World gross domestic product growth was recovering before the U.S. presidential election, and we believe that will continue. The U.S. and Europe look a little better, and that’s positive in terms of resources demand.”

A third factor concerns the narrow band of crude oil pricing, which has changed little in the past year, largely due to U.S. shale-oil production.

“Producers in the Permian Basin have costs that are quite low,” says Overdevest. “Many [producers] are drilling wells that are attractive at [a crude oil price of] US$50 a barrel. [These producers] are not cutting back; in fact, they are accelerating their growth. OPEC has cut back its supply, but it’s more than offset in places like the Permian.”

Overdevest notes that the U.S. is producing 9.3 million barrels a day, vs global production of 96.3 million barrels. “Supply and demand is very much in balance at this time,” he says. “That’s why the oil price is not moving a whole lot from the narrow band. What’s going to change this is that the oil supply has to change drastically. The only other factor is a change in demand. Although global growth is anemic, demand still is growing. But on the supply side, there is not much changing.”

Over the long term, Lekkerkerker and Overdevest are bullish. But current conditions are not as positive as they were a year ago, says Lekkerkerker, who argues that there are only a few pockets of attractive stocks.

“That’s where active [portfolio]management comes in,” he says. “Going forward, it will be more of a specific commodity and specific stock-picking environment.” For example, he adds, lumber looks attractive because of tight supply conditions, while natural gas is suffering from excesses.

About 58% of the Fidelity fund’s AUM is in oil and gas stocks, and 34% is in basic materials (including metals and mining). The Fidelity fund’s weighting in energy is slightly lower than the energy weighting in the benchmark MSCI all-country world natural resources index, while the Fidelity fund’s weighting in basic materials is slightly higher. There also is about 6% in cash, while the portfolio managers look for buying opportunities.

Lekkerkerker and Overdevest are bottom-up stock-pickers; the Fidelity fund holds about 51 names.

The portfolio managers like Red Deer, Alta.-based Parkland Fuel Corp., which operates convenience stores and gas bars across Canada.

“[Parkland operates] in a different part of the energy chain,” says Overdevest, adding that the firm has grown through acquisition. “The gas-bar business is a very good one because people often buy water or chocolate bars, which are high- margin items. More important, there is high traffic flow, which leads to very high returns on equity. In Parkland’s case, it’s over 12%.”

Parkland stock, which trades at about $31.40 a share, has a cash-flow yield of about 6% and a 4% dividend yield. There is no stated target.

Another favourite is Vancouver-based West Fraser Timber Co. Ltd., a major producer of lumber in Canada and the U.S.

“There are pretty attractive supply/demand characteristics for lumber,” says Lekkerkerker. “The number of single-family homes being built in the U.S. still is very low compared with the previous peak. We think housing starts will continue to grow and drive the demand side of the equation. And on the supply side, adding capacity in the U.S. is hard, because the labour market is really tight due to very low unemployment.”

West Fraser stock, which is trading at about $58.80 a share, has a forward price/earnings multiple of about 10. Says Lekkerkerker: “The stock is cheap.”

© 2017 Investment Executive. All rights reserved.