p> Canadian small- and mid-capitalization stocks have rallied this year, especially in the energy and materials sectors. Although fund portfolio managers maintain those sectors tend to have lower-quality names, the consensus is upbeat about opportunities in other parts of these asset classes.

“There’s been a big relief rally in Canada relative to what people believed would happen a year ago,” says Greg Dean, principal with Cambridge Global Asset Management, a unit of Toronto-based CI Investments Inc., and lead portfolio manager of CI Cambridge Pure Canadian Equity Fund. He shares portfolio- management duties with Stephen Groff, principal with Cambridge.

“[Last year,] we saw depression levels of commodities prices, and recessionary levels for industrials. But like [for] anything else, the pendulum swings too far in both directions. In 2014, people were too optimistic. Then through 2015, the pendulum swung hard the other way,” says Dean. “We actually reopened one of our Canadian funds and took advantage of some of the opportunities.”

Today, Dean believes conditions are fairly balanced: “From here, you just have to pick stocks well. I don’t think many people benefited from the recent [stock prices’] appreciation because a lot of [investors] left the market.”

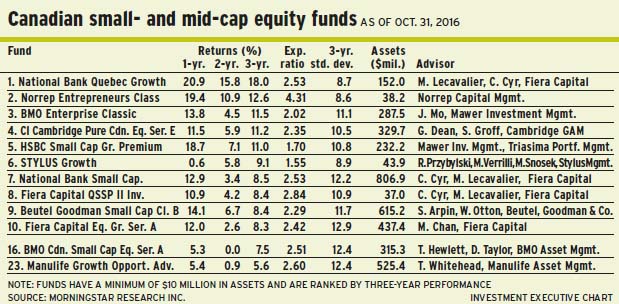

Dean is reluctant to offer a forecast, mainly because the domestic market is concentrated in financials, energy and materials. Rather, he is confident about the diversification of the CI Cambridge fund, which holds 32 names.

“I don’t spend a lot of time on macro calls, unless we feel the market is at one of the extremes – either too positive or negative,” says Dean, adding that he’s concerned about the impact of potentially higher interest rates and how that may trigger selling by panicked investors. “Today, we’re somewhere in between. Stocks are not cheap, but they’re not expensive either or reflecting investor euphoria as they were in 2014. [Today’s stock market] is an exciting hunting ground.”

About 24% of the CI fund’s assets under management (AUM) is in cash, 18% is in energy, 15% is in a mix of consumer staples and discretionary stocks, 12% is in industrials and 12% is in financials, with smaller holdings in sectors such as technology.

The heavy cash weighting is due largely to profit-taking after commodities and industrials stock prices surged upward since last year. “We’re still uncomfortable with the Canadian consumer, so cash is a very desirable place to be until we find great opportunities.”

Although Dean is cautious about the consumer-based sectors, he likes Brick Brewing Co., which has reduced costs by consolidating its operations and benefited from volume growth in Ontario. “Earnings will more than double this year,” says Dean.

Brick stock trades at $3 a share, or 20 times consensus earnings. Dean’s target is $5 a share within two years.

The rally has been narrow, says Tyler Hewlett, vice president with Toronto-based BMO Asset Management Inc. (BMOAM) and lead portfolio manager of BMO Canadian Small Cap Equity Fund. He shares portfolio-management duties with David Taylor, portfolio manager at BMOAM.

“[The rally] was focused on energy and gold. You had a kind of ‘anti-U.S. dollar rally,’ as I call it,” says Hewlett. “After several years of a strong U.S. dollar and, going into 2016, you had expectations for [the U.S. Federal Reserve Board to increase interest rates], which is negative for commodities. As those expectations began to fade, you had this anti-U.S. dollar rally and, given the dominance of commodities in the Canadian market, that really drove the rally.”

Two-thirds of the rally came from gold, Hewlett estimates, plus another 20% from energy stocks.

“For the first six months of the year, the rally was a low-quality and indiscriminate,” he says. “All the gold stocks were going up in tandem. Other parts of the market were largely ignored, regardless of the fundamentals.”

Meanwhile, Hewlett notes, gold stocks have slumped because bullion has taken a hit on expectations of the Fed raising interest rates this winter. However, oil stocks are holding their own, as crude oil remains around US$45-US$50 a barrel.

In terms of risks on the horizon, Hewlett points to the aforementioned potential interest rate hike in the U.S., although he believes that the impact on the equities market is likely to be short-term. “The market has gotten used to very low interest rates. But it could perceive [a rate hike] as a positive thing, once [investors] realize that the economy can sustain slightly higher interest rates.”

A bottom-up investor, Hewlett argues that many stocks display strong fundamentals: “There’s certainly a skew toward better economic conditions in Central and Eastern Canada, and a weaker view of the West. Oil has come off its lows, but it’s much lower than a few years ago. Companies that are exposed to the consumer sectors in Alberta, for example, are a bit weaker, given the uncertain outlook for oil.”

About 20% of the BMO fund’s AUM is in industrials, 20% is in energy, 15% is in technology, 12% is in consumer discretionary and 10% is in materials. There are smaller weightings in financials and real estate.

One of the top holdings in the 60-name fund is StorageVault Canada Inc., which provides moving services and self-storage units in 40 locations.

“[That’s] a very fragmented and underpenetrated market in Canada,” says Hewlett.

StorageVault stock is trading at about $1.25 a share, although Hewlett’s target is $1.50 a share within 12 months.

Ted Whitehead agrees with his peers and says the equities market’s rally has been driven by a surge in gold prices and a similar upward move in oil prices. But risk appetite and improving fundamentals also played a part.

“In Canada, the small-cap index came off dramatically last year, and a lot of that was in the materials sector and was overdone,” says Whitehead, senior managing director with Toronto-based Manulife Asset Management Inc. and portfolio manager of Manulife Growth Opportunities Series Advantage Fund.

“Whereas gold was the first to rally, that has spread to energy. A lot of that is due to OPEC being more accommodating and open to the idea of cutting back production and letting prices rise. Whether prices will go higher is a million-dollar question. But [the market] now has put in a kind of floor and prices may not go below US$40-US$45 a barrel. I’m not calling for higher prices, but for more stabilization.”

Whitehead addresses the macroeconomic picture by saying it’s easy to be negative, and points to uncertainty surrounding the U.K.’s intention to exit from the European Union.

“My view is that we have hit a spot and are chugging along with 1.5%-2% gross domestic product growth. The beauty of that is it’s likely to keep interest rates low and we’re not likely to see too much inflation,” says Whitehead. “Low interest rates and an agreement [by OPEC] about oil should stabilize the Canadian dollar in the US75¢-US80¢ range.

“If you are a believer that we are in the midst of a commodities recovery,” he adds, “then small-caps will perform better because they have more exposure to that part of the economy. That’s where I’d lean for maybe the next year or so. In large-caps, certain sectors, such as staples, are overvalued. People are focused on buying yield and not as concerned about growth.”

The Manulife fund is fully invested. About 23% of AUM is in energy, 20% is in materials, 12% is in technology and 12% is in consumer cyclical. There are smaller holdings in sectors such as industrials.

One top holding in the 80-name Manulife fund is Chemtrade Logistics Income Fund, which produces a wide range of industrial chemicals, such as liquid sulphur dioxide.

“[Chemtrade] is engaged in a cyclical recovery and [the stock] pays a relatively high yield,” says Whitehead, noting that the stock has a payout ratio of about 75%, but generates a 6.5% distribution.

Chemtrade stock is trading at about $17.45 a share. Whitehead has a share price target in the low $20s within 12 to 18 months.

© 2016 Investment Executive. All rights reserved.