CANADIAN EQUITY BALANCED funds produced double-digit returns in 2014, in the face of severe pressures on the energy sector. And despite the prospect of rising interest rates in the U.S., a development that Canada also may experience in mid- to late 2015, fund portfolio managers remain upbeat on equities while tempering their enthusiasm for bonds.

“Interest rates are likely to rise in the U.S., given the employment outlook. We see pretty robust job growth in the U.S. and improving consumer spending,” says Cecilia Mo, vice president at Toronto-based 1832 Asset Management LP, and portfolio manager of Scotia Dividend Balanced Fund. “By mid-2015, we will very likely see the Federal Reserve [Board] start tightening in the process of normalizing interest rates for this cycle. The Fed will start with 25 basis points [bps] and then see how it goes.”

Mo expects the Canadian dollar (C$) to continue to decline and fall to US$0.85, or possibly lower. “The Canadian economy has relied too much on consumer spending and the residential property market. The declining dollar could help rebalance our economy and boost our export markets,” says Mo, who expects the Bank of Canada will be supportive of a weak C$ and likely to lag the Fed’s tightening bias.

As for market valuations, Mo argues that Canadian stocks are expensive, especially the utilities and banking sectors, which she is avoiding altogether. However, some information technology (IT) and industrial stocks that are leveraged to U.S. growth appear to be interesting as are some energy names (which, Mo argues, have been oversold).

“The next three to six months will be very challenging,” Mo says. “There are a lot of companies trading at a discount to intrinsic value. I’m buying a few names on an incremental basis.”

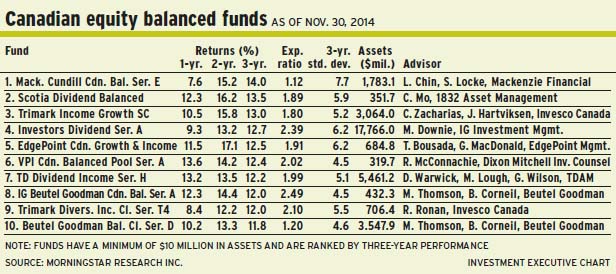

Mo is a value-oriented portfolio manager. About 10% of the Scotia fund’s assets under management (AUM) is in cash, 19% is in energy, 17% is in industrials, 15% is in financials (insurance firms and asset managers) and 12% is in consumer discretionary. There are smaller holdings in sectors such as materials.

The equities portion of the Scotia fund is about 78% of AUM, with 58% in Canada and 20% in the U.S. (which is partially hedged back into the C$). About 12% is split between Scotia Fixed Income Fund and Scotia Private Canadian Corporate Bond Pool, managed by Romas Budd, vice president of 1832 AM. This portion of the balanced fund has an average duration of 4.3 years (vs 7.1 for the benchmark FTSE TMX Canada universe bond index), held primarily in federal and provincial bonds.

Running a fund with 78 names, Mo likes Canadian mid-cap stocks such as Stantec Inc., an engineering firm involved in infrastructure and transportation, which earns almost 50% of its revenue from the U.S. “[Stantec] has an excellent management team and solid organic growth,” says Mo, adding that the firm is expected to grow revenue and earnings by about 15%-17% in 2015.

Stantec stock is trading at about $30.15 a share, or 13.5 times trailing earnings. There is no stated target.

Equally bullish is doug Warwick, managing director of Toronto-based TD Asset Management Inc., and lead portfolio manager of TD Dividend Income Fund.

“The U.S. is particularly strong, the rest of the world is ‘weakish,’ and Canada might weaken a bit because of the recent decline in crude oil,” says Warwick, noting that the drop in oil prices could be deflationary. “We don’t think interest rates will rise materially. People keep talking about it, but the rate hikes continue to be delayed.”

Rising interest rates are a healthy sign, Warwick argues, and probably would be absorbed by the market in a few months. “We’ve gone back and looked at previous periods of rate rises and noted that the market weakens for three to six months. But, generally, the market is higher within 12 months; it recognizes that it’s the stronger economy that is driving the higher rates,” Warwick says, adding that rates may go up by 50 bps at the most.

Moreover, he argues, rising rates will help financials because the hikes would relieve some of the pressure on so-called “net interest margins” that banks have been living with.

Meanwhile, Warwick says, valuations still are attractive. He notes that bank stocks, for instance, are trading at 11.7 times future earnings – almost the same as in late 2013.

Says Warwick: “Investors are a little slow to realize that the businesses that the banks are involved in have evolved and are much more stable. People worry about the housing market and how it might [affect] the banks. I don’t think it will be a huge issue.”

He adds that the banks would not see an appreciable decline in their Tier 1 capital ratios should a severe decline in home prices occur.

About 21% of the TD fund’s AUM is in fixed-income, which has an average duration of 6.5 years and is heavily weighted in investment-grade corporate bonds. Meanwhile, 46% of AUM is in financial services stocks, 8% is in energy, 7% is in utilities and 7% is in IT. There are smaller weightings in sectors such as consumer goods, with 2%. Less than 5% is in non-Canadian assets.

Running a portfolio with 55 equity holdings, Warwick likes names such as Bank of Nova Scotia, which under new CEO Brian Porter, has restructured some of its less profitable international operations: “Our expectation is that the bank will continue to do well.” Scotiabank has a 16.5% return on equity, which Warwick believes will improve with time.

Scotiabank stock trades at about $65 a share, or at 11.8 times future earnings. There is a 4% dividend. There is no stated target.

Clayton Zacharias, vice president at Toronto-based Invesco Canada Ltd. and lead portfolio manager of Trimark Income Growth Fund SC, is reluctant to predict the direction of interest rates or markets. He shares portfolio-management duties with Jennifer Hartviksen, vice president and head of fixed-income at Invesco.

“Using a bottom-up approach, we construct concentrated portfolios and look for compelling opportunities, regardless of what’s going on in the overall market,” says Zacharias. “But we’ve been finding that valuations are pretty full, making it difficult to find compelling opportunities. The one recent exception is the energy space, where valuations have come off dramatically.”

As an example of a market that has become pricey, Zacharias points to stocks of grocery firms, such as Loblaw Cos. Ltd., whose valuation is around 19 times forward earnings. “Are they better or worse businesses than a year ago, when their valuations were much lower?” asks Zacharias. “I find it hard to justify paying a high multiple just because I want something perceived to be safe. That’s not our style.”

Although Zacharias is cautious about predicting the pace of interest rate hikes, he notes that rising rates should result in falling price/earnings multiples.

“We’re not willing to pay up on stocks, just because interest rates have been temporarily low,” says Zacharias. “A lot of investors have fallen into that trap. On an absolute basis, some valuations have risen too high.”

Zacharias is a value-oriented investor. About 14% of the Trimark fund’s AUM is in cash, which is a residual of his bottom-up approach. “I’d rather be patient and deploy the cash whenever we find the right opportunities.”

There also is 25% in fixed-income, with a particularly short average duration of 3.1 years and weighted toward corporate bonds.

From a sector standpoint, 23% of AUM is in financials, 11% is in energy and 7% is in health care. There are smaller holdings in such sectors as IT, with 6%. About 21% of AUM is in non-Canadian assets, which is unhedged.

Running a tight portfolio of 29 holdings, Zacharias likes names such as Brookfield Asset Management Inc., which has interests in infrastructure, real estate, renewable energy and private equity.

“[Brookfield invests] in quality, long-life assets that generate strong cash flows over time. These assets are hard to replicate,” says Zacharias, noting that the firm owns major office towers in New York, Calgary and Toronto. Brookfield also collects fees for managing about US$84 billion worth of assets held by third-party owners.

Brookfield stock is trading at about $56.75 a share, pays a 1.3% dividend and trades at about its net asset value. There is no stated target.

© 2015 Investment Executive. All rights reserved.