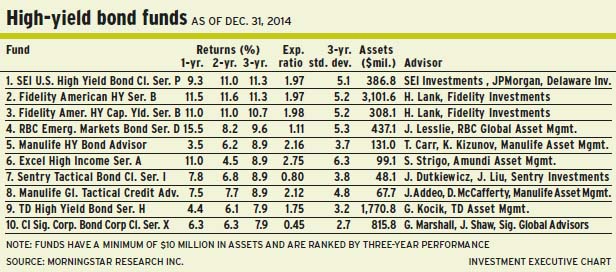

High-yield bonds performed well in 2014, thanks to improving economic fundamentals and a benign interest rate environment. Despite the strong probability of rising interest rates in the U.S., portfolio managers of high-yield bond funds are upbeat about prospects in 2015.

“We’re in a sluggishly improving economy, which is the perfect backdrop for interest rates to stay relatively low,” says Harley Lank, vice president with Boston-based FMR LLC (a.k.a. Fidelity Investments) and lead portfolio manager of Fidelity American High Yield Fund. “We’re not seeing a lot of inflationary pressures and there’s relative weak growth around the globe. That will help keep a damper on interest rates. Even if they tick up a little bit in the U.S., and [are raised] gradually, high-yield [bonds] can handle that well.”

However, he concedes, a rapid series of interest rate hikes would affect the high-yield asset class. “But keep in mind, that’s usually associated with a rapidly improving economic environment. That generally means good things for non-investment-grade companies as well,” says Lank, who expects benchmark 10-year U.S. treasury yields to climb to about 3% by the end of 2015 from 2% today.

The spread between high-yield bonds and U.S. treasuries is about 475 basis points (bps), but, Lank says, there is a reasonable possibility that the spread could narrow to about 400 bps in the next year.

Although Lank expects some volatility along the way, the backdrop is favourable, “driven by my expectation of very low default rates,” he says, adding that the current 2% default rate is well below the long-term average of 5%.

Returns in 2015 could be about 7%-8%, Lank says. In effect, that’s slightly higher than the 6.7% coupon from the benchmark Bank of America Merrill Lynch high-yield master II constrained index, he adds: “It’s the first time in a couple of years that I’ve said there is possibly one to two percentage points of capital appreciation.”

About 41% of the Fidelity fund’s assets under management (AUM) is in BB-rated bonds, 36.6% is in B-rated bonds, 9.3% is in CCC-rated bonds, 3.7% is in BBB-rated bonds and about 5% is in cash.

“There are a lot of opportunities to make total returns through credit improvement of single B- and BB-rated names in the marketplace,” Lank says. “That’s where I’m focusing a lot of my attention.”

The Fidelity fund holds 10.8% of AUM in telecommunications, 9.6% in energy, 9.5% in health care, 8.6% in diversified financial services and smaller weightings, such as 5.4% in cable TV. The fund’s average duration of about four years is similar to that of the benchmark.

Running a portfolio of about 350 issuers, Lank likes names such as Ally Financial Inc., formerly the financing arm of General Motors Corp., which was spun off during the 2008-09 global financial crisis. “It’s got an extremely resilient business model,” Lank says.

Ally’s BB-rated bond, maturing in 2031, is yielding about 5.7%.

It’s not going to be an easy ride, argues Terry Carr, vice president and head of Canadian fixed-income with Toronto-based Manulife Asset Management Ltd., and portfolio co-manager of Manulife High Yield Bond Advisor Fund. (He shares portfolio-management duties with Konstantin Kizunov, managing director of Manulife AM.)

“Despite a good economic environment in the U.S., interest rates keep falling. It’s due to international jitters, chaos in energy market and geopolitical risks – a whole host of challenges,” says Carr. “If you went back a year ago, you would not have seen much of this. We were quite constructive on the U.S., which has played out. But you have a dichotomy between the U.S., which is recovering nicely, and the rest of the world that is far more challenged than people thought. That sets us up for volatility.”

Much like other portfolio managers, Carr expects U.S. rates to rise in mid-2015, with another rate hike possible by the end of the year. Yet, there also is a risk that the U.S. Federal Reserve Board will hike the rates only once, to reflect slow global economic growth.

“We are not expecting much of an interest rate headwind at this point,” Carr adds. “But if we start to get more bullish signals, whether from Europe or China, that [event] could reverse interest rates more materially, given how much they have rallied. If we don’t get that, then interest rate worries are misplaced. I don’t think that in the longer run, the U.S. could go it alone unless some positive things happen in other jurisdictions.”

Given the possibility of two scenarios, the Manulife fund’s portfolio managers are being cautious, keeping average duration at about 3.75 years.

About 63% of the Manulife fund’s AUM is in B-rated bonds, 18% is in BB-rated, 16% is in CCC-rated and 3% is in cash.

About 80% of AUM is in U.S.-denominated bonds, mostly hedged back to the Canadian dollar (C$). There’s also 20% in Canadian firms and 5% in international issuers. From a sectoral standpoint, 18% is in basic industries (vs 10.5% in the benchmark), 8.7% is in energy (14.5%), 7.7% is in consumer non-cyclical (3%), 5.5% is in consumer cyclical (4.7%) and smaller weightings, such as 2.7% in financial services (6.3%).

Kizunov, largely a bottom-up investor, likes names such as Thompson Creek Metals Co. Inc., one of the world’s largest miners of molybdenum (used in making steel), which operates mines in Canada and the U.S.: “The company is in the final stages of ramping up Mount Milligan copper/gold mine in northern British Columbia. It will materially diversify [the firm’s] asset base.”

The 2019-dated bond, rated CCC, is yielding about 7%.

Although there is a likelihood of higher interest rates in 2015, the impact on the high-yield asset class will not be that significant, agrees James Dutkiewicz, chief investment strategist with Toronto-based Sentry Investments Inc. and lead portfolio manager of Sentry Tactical Bond Fund. (He works with Jie Liu, portfolio manager and head of credit at Sentry.)

“A gradual tightening, with one or two [interest rate] hikes on the back of good macroeconomic data, is actually quite good for high yield. It will highlight the ‘carry’ or attractiveness of the asset class. There is a fair bit of cushion, as far as spreads are concerned,” says Dutkiewicz, who notes that the 475-bps spread for high yield over treasuries is consistent with long-term trends.

“Compare that with investment-grade spreads, which are 135 bps over treasuries,” adds Dutkiewicz. “So, there’s a 340-bps extra cushion between the two asset classes, which is reasonably attractive.”

Dutkiewicz expects total returns for the high-yield asset class will be around 6%-8%, after fees.

He notes that default rates of 2% are very low. But they could climb in 2015 to about 3%, mainly because of the troubled energy sector, which accounts for about 15% of the benchmark and is under pressure from low commodities prices.

The recent pullback in the energy sector has spilled over into industrials and chemicals: “We have seen softness in other names, which has given us opportunities to add to the fund.”

As a result, Dutkiewicz has reduced the cash weighting in the Sentry fund to about 5% of AUM from 12%, and added some energy and industrial firms.

From a credit standpoint, about 24% of the Sentry fund’s AUM is in investment-grade bonds, 49% in BB-rated, 18.7% in B-rated, and 5% in CCC-rated. “We don’t need to go into the CCC space, to boost our yield,” Dutkiewicz says. “We are tilted to higher quality, with a BB average rating.”

The U.S. accounts for 37.6% of the Sentry fund’s AUM; Canada, 24.3%; and Europe, 21%; with smaller weightings in Latin America and China. From a currency perspective, the fund is hedged back partly to the C$.

Dutkiewicz likes Banco Santander SA, a leading Spain-based bank with operations in the U.K. and Latin America. “The Spanish economy is in the recovery stage,” he says. “The likelihood of this bank getting into trouble is quite low – and we’re being paid a healthy coupon.”

Banco Santander’s 2019-dated bond, rated BB-plus, is yielding about 6.375%.

© 2015 Investment Executive. All rights reserved.