Bond market volatility, triggered by comments from the chairman of the U.S. Federal Reserve Board about phasing out Quantitative Easing III (QE3), has put pressure on real estate investment trusts (REITs) and related equities. But real estate fund portfolio managers maintain that the fundamentals in the sector are sound – and that selectively chosen securities will ride out the prospect of rising interest rates.

“We’re in an adjustment phase rather than a permanent downturn,” says Michael Missaghie, a portfolio manager with Toronto-based Sentry Investments Inc. who oversees Sentry REIT. “We are likely to see higher volatility until investors get comfortable with the 10-year U.S. bond yield at a higher range of 2.5%-3%. But this is likely to create a buying opportunity for quality names.”

The Fed has stated the level that two key metrics – unemployment and inflation – have to be in order to raise interest rates. “But we are nowhere close to where the Fed wants to be,” Missaghie says. “We don’t anticipate that it will taper its bond-buying program in a large way any time soon. And [the Fed] won’t look at the benchmark interest rate, which is close to zero, any time soon.”

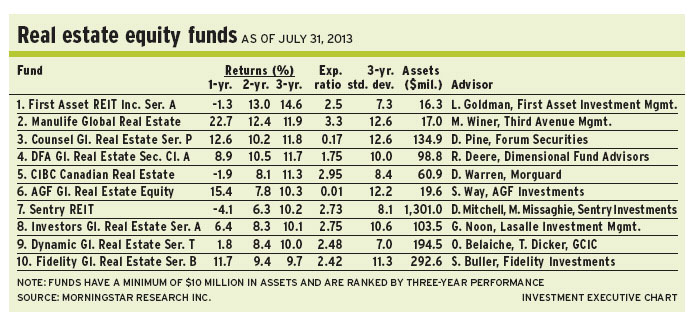

Missaghie, who shares portfolio-management duties with Dennis Mitchell, Sentry’s chief investment officer, says REITs and equities are looking more attractive, based on cash-flow multiples and net asset values (NAVs).

“The spread over the risk-free rate on benchmark 10-year bond yields also is a key measure,” says Missaghie, adding that the spread is about 400 basis points (bps) over U.S. treasuries vs the historical average of 350 bps. “This is signalling that the [real estate] sector is slightly undervalued.”

On a price-to-NAV basis, the sector is trading at a 10% discount, vs a 5% premium over the NAV before the market jitters had set in. On a free cash flow basis, the equities are trading at around 15 times adjusted funds from operations (AFFO), vs 17 times before the downturn.

“We’re getting closer to the historical average of 14.5 times,” says Missaghie, “but far from the peak of 19 times AFFO in 2007.”

The sector’s fundamentals remain solid, he adds: “Occupancy and rent levels are stable or improving. You have very little new supply. And free cash flow growth that REITs are generating is closer to 5%-6%, vs the historical norm of 2%-3%. In an environment [in which] all these things are working for the sector, it doesn’t make a lot of sense that it is trading at a 10% discount to NAV and close to the average historical free cash flow multiple.”

About 54% of the 50-name Sentry fund’s assets under management (AUM) is in Canadian firms, 30% is in U.S., 10% is in Europe and Asia, and 6% is in cash.

One top holding in the Sentry fund is U.S.-based Simon Properties Group Inc., the largest REIT in the world. “[Simon] is trading at a 10% discount to NAV,” says Missaghie, adding that cash flow growth will be almost 10% in 2013-14. Simon is trading at about US$163 per unit ($169.30) and pays a 2.8% yield. Missaghie believes its intrinsic value is US$180 per unit.

Although the bond market reaction to the Fed’s comments about easing off from QE3 was strong, it’s important to recognize the positive dynamics behind the move, argues Derek Warren, a portfolio manager with Toronto-based Morguard Corp. who oversees CIBC Canadian Real Estate Fund.

“The U.S. economy is strengthening,” says Warren. “This is not a ‘bad news’ story; it’s a ‘good news’ story. This affected REIT pricing, but the move was necessary. REITs had several strong years, with returns in the 20% range – that’s a little bit much. So, a pullback was to be expected. Last January, we were starting to reposition the portfolio. We expected a correction, although it happened more severely than anticipated – it always does.”

Indeed, notes Warren, the benchmark Morgan Stanley REIT index, which tracks U.S. REITs, has been on a roller-coaster ride. Between Jan. 1 and May 21, the index was up by 20%. Then, it tumbled on the Fed’s commentary: year-to-date returns fell to about 6%. “Things are more normalized [now],” says Warren. “Over the long term, real estate returns are 10% per annum. So, 6% in seven months is fine. But it’s the volatility that has shocked the market, not the returns themselves.”

Determining what to expect for the balance of the year is a mug’s game. Yet, with the benchmark 10-year bond yield possibly moving to 3% from 2.5%, Warren believes that investors will shift their focus from the value of a property and pay more attention to the value of its cash flow.

“After three years of double-digit returns, we are returning to a more normalized real estate cycle,” he says. “You will get your 7% yield and 3% growth, for a total of 9%-12% annual returns.”

About 70% of the 44-name CIBC fund’s AUM is in Canadian companies, 27% is in U.S. firms and about 3% is in cash. Says Warren: “We are going to Canada for yield, but to the U.S. for growth.”

One favourite Canadian name in the CIBC fund is Allied Properties REIT, which specializes in upgrading heritage properties in downtown urban centres. “It’s a very high-quality company with the best balance sheet in the REIT space,” says Warren. “And it has no need to go to market for capital.” Allied Properties is trading at $32.37 a unit, or 16.5 times AFFO. It has a 4.2% yield. Warren has no stated target.

On the U.S. side, Warren likes Camden Property Trust, a mid-sized apartment builder active in the U.S. Southwest and Southeast. “Apartments have underperformed other subsectors,” he says, “and are trading at a discount to traditional valuations. But this area is now participating in the economic recovery.”

Camden units are trading at about US$73.50 ($76.30) each or 20 times AFFO. The units also have a 3.4% dividend yield.

Although it’s uncertain if the worst is over, says Tom Dicker, a portfolio manager with Toronto-based GCIC Ltd. who is co-manager of Dynamic Global Real Estate Fund: “It certainly feels like the worst is over. We had the initial shock that tapering of the Fed’s bond-buying program could end and the realization that the direction of interest rates had finally changed. But we’re now ‘normalizing,’ and the bond market is pricing in a more reasonable scenario.”

Since the turmoil has abated, Fed chairman Ben Bernanke has issued more “dovish” commentary, stating that the timeline for tapering the bond-buying program is “flexible,” notes Dicker, who shares portfolio-management duties with Oscar Belaiche, senior vice president with GCIC.

Dicker argues, much like his peers, that valuations are attractive, given that the earnings yield on REITs is 6.8%, vs 7% for the long-term average. “Now, we’re at 14.8 times AFFO, but the long-term average is roughly 15 times AFFO,” says Dicker. “This tells you that either the market is anticipating that NAVs are lower than what analysts estimate or that stocks are very cheap. Either way, it’s a better time to invest than two or three months ago.”

From a strategic standpoint, Dicker has allocated about 38% of the Dynamic fund’s AUM to Canadian firms, 35% to U.S. companies, with smaller amounts going to holdings in France and Australia, and 8% to cash.

“We like the growth profile of the U.S. REITs,” says Dicker, who has concerns about overbuilding in Calgary and Toronto. “Rents continue to improve in the U.S. across most property types.”

One top U.S. holding in the Dynamic fund is Prologis Inc., the largest owner of industrial properties in the world.

Prologis shares are trading at about US$40.20 ($41.65) and offer a 2.8% dividend yield. At 26 times AFFO, the multiple is high, Dicker admits: “But the company has a strong growth profile, which should be 10%-plus for the next few years.”

On the Canadian side, Dicker likes Brookfield Office Properties Inc., a leading office developer/owner with properties in Canada, the U.S. and Europe.

Brookfield stock has come under pressure because of market concerns about a major tenant departing from Brookfield Place, formerly the World Financial Centre, in New York.

“Brookfield has work to do on the leasing,” Dicker says, “but it has some very talented people in that area. There also is new transit being built underneath, and Brookfield’s rents are very competitive.”

Brookfield’s stock is trading at about $17.85 a share, although Dicker believes the NAV is $20, which implies a 9% discount. The stock pays a 3.25% dividend.

© 2013 Investment Executive. All rights reserved.