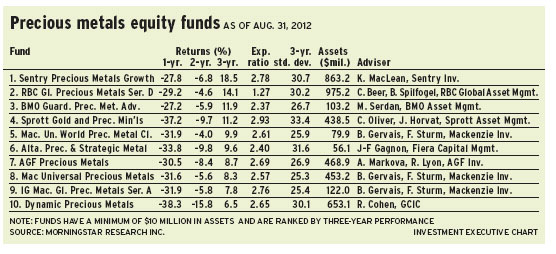

PRECIOUS METALS EQUITY funds have taken a beating in the past 12 months, thanks to flat gold bullion prices and disappointed investors who have left the sector. Yet, fund portfolio managers believe the sector is poised to recover, buoyed by both the belief that continued monetary stimulus will support a rising gold price, which has recently surged to US$1,730 an ounce, and improving fundamentals in the sector.

“When you look at different sector funds, gold tends to be either the poster child or the whipping boy,” says Ch r i s Be e r, v i ce president of Toronto-based RBC Global Asset Management Inc. (RBC GAM), and co-manager of RBC Global Precious Metals Fund. “I often get asked, ‘Why has the sector under-performed gold bullion?’ And I tell them the only resources stock that’s outperformed the underlying commodity is Agrium Inc. But look at Suncor Energy [Inc.]: it was a $65 stock in early 2008; today, it is $32 and oil prices are up again.”

One of the chief culprits for the past year’s malaise in the gold sector is “industrywide inflation in capital costs and, more important, labour costs,” says Beer. “The trades required to build a $10-billion processing plant or a $1-billion mine are complex and expensive. The cost to develop a mine by a smaller firm, such as Detour Gold Corp., has gone to $1.6 billion from $1 billion in the past couple of years – and that’s only one example.”

Beer, who shares portfoliomanagement duties with Brahm Spilfogel, RBC GAM vice president, also notes that in the past decade, gold prices have risen at an annual compound growth rate of 16% and costs have escalated at an annual compound rate of 14%, but capital expenditure has increased at 20% compounded annually.

“The market doesn’t believe these companies can reinvest their cash flow and get a rate of return they’re willing to live with,” says Beer. “The margin between the gold price and costs has grown by 2% a year. But with a flat gold price this year, margins will be even more constrained.”

Still, Beer is optimistic about a turnaround in gold stocks, partly because senior bullion producers are either postponing or cancelling costly ventures. “Barrick [Gold Corp.], for instance, is not going to build the Cerro Casale project in Chile,” says Beer, adding that the company also had been hurt by runaway costs in building the Pascua-Lama project in the Andes. “These companies are finally ‘getting it’ and they’re looking at their capital structures. Because the market has penalized them, they are looking at alternatives more realistically.”

The RBC fund contains about 180 companies, and Beer and Spilfogel have split the fund’s assets under management (AUM) roughly equally among large-cap, mid-cap and small-cap bullion producers. One small-cap favourite is Rio Alto Mining Ltd., which is developing a mine in Peru that is producing about 150,000 oz. a year. Rio Alto stock is trading at about $5 a share, or about five times cash flow. But Beer has a target of $6-$7 within 12 to 18 months, based on management’s success in developing a neighbouring copper/gold project.

Beer also likes small-cap Contine nta l G ol d In c. , which is developing a Colombian project that has the potential to produce more than 200,000 oz. annually within two years. Continental’s share price is about $7.75, although Beer believes it could double within 18 to 24 months.

ANI MARKOVA, VICE PRESIdent with Toronto-based

AGF Investments Inc. and manager of AGF Precious Metals Fund, argues that the sector has seen the worst of the decline.

“We’ve gone through a prolonged period of consolidation, which is very healthy for the industry,” says Markova. “Perhaps gold bullion ran into an overbought situation last year. This year, it has bounced off the US$1,550 an oz. level – or, the marginal cost of production – which gives me comfort that we are still in a secular bull for the commodity. We’re ready to resume the upward momentum.”

Although August saw the beginning to the recovery of gold stocks, they still are trading at less than 10 times cash flow, she says, compared with the historical average of 22 times. “Gold stocks are now trading like any other stocks,” says Markova. “I don’t think we’ll go back to the levels at which stocks traded at significantly high premiums just because they are gold equities. To me, some stocks are fairly valued and some are undervalued; it’s a stock-picking exercise. Many producers are in undervalued territory, or where we see a compelling reason to go in and buy them.”

Cheaper valuations are not the only reason to buy. Purchase decisions also involve the gold bullion price. “I do believe we will see a much stronger price over the next six to 12 months,” says Markova. “It’s driven by what’s going on in the global macroeconomic environment, both in the U. S. and Europe, and also China and Japan. They are continuing to ease their monetary policies, which is very attractive for gold.”

Markova, who shares portfoliomanagement duties with Robert Lyon, AGF’s senior vice president, agrees with Beer that gold companies have become more conservative about expansion plans. Says Markova: “Companies are saying, ‘It’s no longer growth at any cost, but profitable growth.’ This is what investors want. We’re looking for free cash flow generation, which we haven’t yet seen because of the massive capital overruns on many projects.”

The AGF fund is fully invested; Markova has allocated about 10%-15% of its AUM to gold and silver bullion, 30% to large caps and the balance to mid- and small-caps.

One large-cap pick in the AGF fund, which has more than 120 names, is Eldorado Gold Corp., which is active in Romania, China and Greece and produces about 637,000 oz. of gold a year. “This is a company that is targeting 160% top-line growth within four to five years,” says Markova. “It is committed to paying dividends and has one of the lowest cost structures in the industry.” Eldorado’s share price is about $14, but Markova believes the stock could hit $20 in two to three years.

Another favourite is junior miner Argonaut Gold Inc., which has gold mines in Mexico. “I see an opportunity to reach 250,000 oz. over the next two or three years,” says Markova. The stock trades at about $9.75 a share, or eight times 2013 earnings estimates. The target is $12-$13 a share in about two years.

ONE OF THE MAIN FACTORS that has held back gold stocks, and the bullion price, is that the U. S. has “paused” in the rate of printing money, argues Benoît Gervais, vice president, investments, with Toronto-based Mackenzie Financial Corp., and co-manager of Mackenzie Universal World Precious Metal Class Fund.

“It’s not zero growth but diminished growth in money supply that has caused the gold price to go sideways,” says Gervais. “A year ago, when gold hit US$1,900 per oz., we thought gold’s fair value was US$1,700 per oz. So, it was overpriced at the time.” Based on the current 13% growth rate of the U. S. money supply, Gervais believes that the gold price could be US$1,890 per oz. by June 2013.

Of course, that bet on money-supply growth is not guaranteed. But Gervais is confident, pointing to the signs of more monetary easing in the U. S., as well as in Europe: “There is still a possibility of disagreement in Europe over conditions for money-printing, but the base case put forward by Mario Draghi, head of the European Central Bank, and Angela Merkel, chancellor of Germany, is for more printing of money.”

Gervais, who shares portfoliomanagement duties with Fred Sturm, senior vice president with Mackenzie, and who also manages Mackenzie Universal Precious Metals Fund, notes that gold producers are focusing on generating stronger returns on their investments.

“Some gold companies have learned the hard way and are trying to differentiate themselves after losing a lot of money,” says Gervais. “Yamana Gold Corp. is one example. After buying too many things, it is behaving better than others. But others, [such as] Barrick Gold, are still trying to find their way. The market has been saying, ‘We’re taking away your capacity to buy things.’ That’s why Barrick is trading at three times EBITDA [earnings before interest, taxes, depreciation and amortization] – down from 10 times.”

In a portfolio with investments in about 60 companies, the Mackenzie fund’s AUM is divided roughly among large-caps, midcaps and small-caps. On the largecap side, the fund has a position in Barrick, whose stock has been hurt by cost overruns.

“We think the stock is low enough because it’s going to be tough for [Barrick] to make mistakes,” says Gervais. “The bad news is priced into the stock.” Barrick stock is trading at about $38.90 a share; Gervais has a target of more than $50 within about 18 months.

On the small-cap side, Gervais favours Tahoe Resources Inc., which is developing a silver mine in Guatemala that will go into production next year. The stock is trading at about $19.20 a share; Gervais has a target of about $25 within 18 months.

© 2012 Investment Executive. All rights reserved.