Precious metals equity funds have struggled for several years as the gold price has oscillated between US$1,290 and US$1,350 an ounce, thanks to uncertainty about the strength of the U.S. economy and investors throwing in the towel after gold stocks’ lengthy weak performance. Yet, portfolio managers express optimism that gold bullion’s price could break through the upper limit of its present range and possibly hit US$1,400 and related stocks rise due to better fundamentals.

“Since January, the gold price has been range-bound between US$1,200 and US$1,350. This is an indication there are a lot of conflicting data points that investors are trying to analyze,” says Ani Markova, vice president with Toronto-based AGF Investments Inc., and portfolio manager of AGF Precious Metals Fund. “Investors want to be bullish on U.S. [economic] growth, but they see momentum indicators slowing. We’re in a holding pattern, waiting for clarity on U.S. fiscal or monetary policies. In the context of overall equities markets, other sectors have worked better than precious metals and investors’ interest has faded.”

In Markova’s view, some investors question the Trump administration’s ability to introduce major fiscal policies.

“Trump was elected on the promise that he would grow the economy by almost 4% [a year], and certainly we have not seen any help from the policy standpoint,” says Markova. “Equities markets are arguably stretched and, without tax reform or nominal [gross domestic product] growth to support earnings and valuations, we could be faced with an equities market sell-off as a result of a business slowdown. But the gold [asset class] should do better because it has negative correlation to the overall market. It’s a defensive, portfolio insurance type of asset class.”

What might help gold is uncertainty about how the U.S. Federal Reserve Board will deal with the trillions of dollars in debt instruments on its balance sheet.

“[The Fed’s strategy] will have an impact on equities markets and global liquidity. Since 2008, all the major central banks have put so much liquidity into economies, which found [its] way into markets. If they reduce that liquidity, will markets taper?” asks Markova. “I don’t have an answer to that. But we live in unprecedented times. And in such times, we have to have some protection in assets such as gold.”

Markova argues that bullion could reach US$1,400 within 12 to 18 months: “As we get closer to the debt ceiling negotiations in the U.S., the government is likely to raise the debt ceiling, which means putting more debt on the balance sheet. I expect to see a bigger deficit. Those two factors are negative for the U.S. dollar and, in that environment, gold is very likely to rise beyond the US$1,250-US$1,300 range. The next range is likely to be US$1,300-US$1,400.”

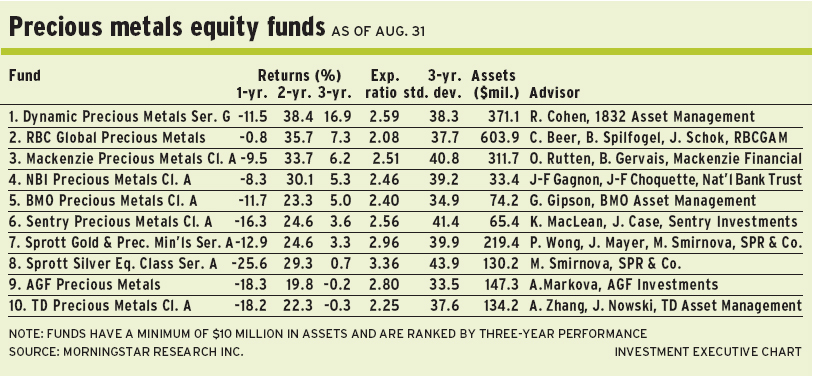

Markova, a bottom-up investor, now focuses on small-capitalization bullion producers, which account for about 40% of the AGF fund’s assets under management (AUM), while mid-caps account for 40% and large-caps, 20%.

“We’re entering the business cycle in which more investment dollars and a greater mergers and acquisition appetite will be focused on the junior and mid-tier companies that are exploring and replacing reserves and resources,” says Markova, noting that senior producers have struggled to replace reserves. “Which are the companies that are able to consolidate or hold on to prospective exploration properties, or deliver drill results and grow the inventory of minable ounces? Those are the stories that we have emphasized.”

One of the top holdings in the 80-name AGF fund is Endeavour Mining Corp., which is expected to produce about 500,000 oz. this year in countries such as Mali and Cote d’Ivoire.

“Its focus is not only on growth through a group of high-quality assets, but also assets that can help reduce the overall costs of production,” says Markova, noting that by 2019, the firm’s target is more than 800,000 oz. “We have a perfect situation, in which growth is going up and costs are coming down.”

Endeavour stock recently traded at $23 a share, or one time net asset value. Based on the firm’s expected production, Markova has a target of $32-$35 within 12 to 18 months.

Chris Beer, vice president of Toronto-based RBC Global Asset Management Inc. (RBCGAM) and portfolio co-manager of RBC Global Precious Metals Fund, believes that the Fed’s anticipated interest rate increases in the next year or so will be gradual and ultimately supportive of gold bullion’s price.

“Given what we’ve seen of the Trump agenda and the trade agenda, those tend to be inflationary, based on historical experience,” he says. “So, bouncing between US$1,200 and US$1,300 has not been surprising. And going forward, we are unlikely to see massive interest rate increases. But from a macro perspective, gold has a good shot at breaking through US$1,300.”

However, forecasting when this will occur is problematic, Beer admits: “If you use an oil price of US$50 a barrel, real interest rates of 55 basis points for the 10-year treasury and the U.S. dollar at where it’s now on a trade-weighted basis, a year out you could be looking at north of US$1,300 [as oz. for gold bullion]. It’s a combination of those three variables. But if you use a US$55 oil price, higher inflation and a weak U.S. dollar, you could get to a US$1,350-$1,400 gold price.”

Geopolitical uncertainty could drive gold even higher. Not only are there worries about the conflict between North Korea and the U.S., but another concern is last summer’s change within the Saudi regime in which Crown Prince Mohammed bin Nayef was replaced by his cousin, Mohammed bin Salman.

“All is not necessarily well in the Middle East,” says Beer. “And there is Russia’s involvement in Ukraine, which the U.S. cannot stop. The geopolitical space is very tough to forecast, but this is an environment in which people are probably, at the margin, allocating a little more to gold.”

Beer notes that the weakness in the gold price has been a positive factor in forcing many bullion producers to clean up their balance sheets. For example, big firms such as Barrick Gold Corp. sold off some assets in the past few years and will bring its debt levels down to about $5 billion by yearend 2018 from $12 billion today. “Companies have been extraordinarily lean on capital deployment these past few years,” Beer says. “Capital spending will have to increase if gold companies are to replace reserves, and finding those companies best able to deploy capital is our No. 1 focus.”

Another sign of more conservative capital allocation: in 2013-14, large-cap producers had 440 million oz. in gold mine reserves; today, that figure has dropped to 300 million oz.

“That’s a function of the gold price. But the average reserve life for mines has generally come down from about 12 years to about eight years,” says Beer. “From a supply perspective, in 2016, we started to see a decline in overall gold produced and saw another decline in 2017. But, historically, what has moved the gold price is a macro event rather than the true supply/demand picture for gold.”

Beer argues there is more value in mid-caps, which account for about 40%-45% of AUM, followed by 30% in small-caps and 25% in senior producers.

A top mid-cap holding in the 70-name RBC fund is Kirkland Lake Gold Ltd., which has a production target of about 600,000 oz. this year from mines in Ontario and Australia.

“This is a company that is trading at five times enterprise value to [earnings before interest, taxes depreciation and amortization.] It’s growing production at 10%-20% a year, has no debt and a low valuation. And the gold price has a decent chance of breaking through the US$1,300 level. If that happens, margins will expand even more,” says Beer, noting that the stock has a 40% upside within 12 to 18 months.

Newmont Mining Corp. is another favourite. It produced about five million ounces in 2016. The stock is trading at US$35.80 (C$45.90), about eight times EV to EBITDA. The target is US$42 in 12 to 18 months.

© 2017 Investment Executive. All rights reserved.