After three miserable years, precious metals stocks have rebounded, driven by investors responding to improving fundamentals. And although the price for gold bullion has been flat since the start of this year, at about US$1,220 an ounce, portfolio managers of precious metals equity funds are bullish and argue that the sector’s prospects have turned for the better.

“Bullion really took it on the chin last year, but gold stocks started to lead,” says Ani Markova, vice president with Toronto-based AGF Investments Inc. and lead portfolio manager of AGF Precious Metals Fund. One of the main drivers of a falling gold price, she adds, was the stunning 34% decline of gold-based exchanged-traded funds (ETFs), which dropped as panicked investors dumped those ETFs.

“Eight-hundred and eighty tons [of bullion], combined with 600 tons from COMEX warehouses, hit the market. And the only [countries willing to buy gold] were China and India,” says Markova, who works with Robert Lyon, senior vice president of AGF. “Because of this development, the gold price went below US$1,200 last December. Since then, the market has stabilized and we have seen a levelling off of ETF volumes. Most investors seem to want to stay invested. That gives a nice cushion to the gold price.”

Gold bullion has settled around the so-called “all in” cost of production, which is about US$1,300 an ounce.

“That price is the natural equilibrium price at which gold is consolidating. That’s what we’re seeing this year,” says Markova, noting that gold stocks are up by 27% year to date, while bullion is up by only 6.5%. “It’s natural in this environment, with stability in the commodity price, for gold stocks to bounce back and respond more positively.”

Also, management teams at gold-mining firms have been more focused on cost-cutting and demonstrating better profitability, explains Markova: “That’s why the gold stocks sold off earlier – because investors recognized that the earnings were not there. Now, valuations have come down substantially, and investors are saying, ‘Show us the profitability.’ It comes down to the deferral of unprofitable projects, more focus on better mining practices and rethinking of the assets that are being operated.”

Markova believes that bullion’s price may range between US$1,200-US$1,400 an ounce in the near term; but, over the longer term, the price will rise to US$2,500 because of global inflationary pressures. She is confident that the momentum into next year favours gold stocks.

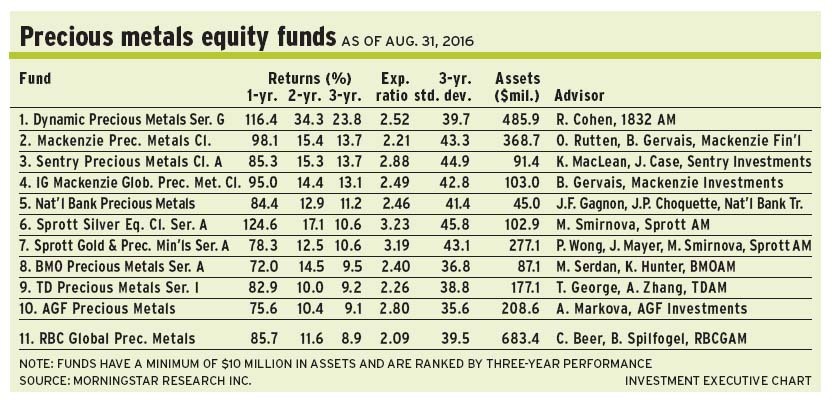

About 50% of the AGF fund’s assets under management (AUM) is held in small-caps and junior exploration firms; 30% is in large-caps; and 20% is in mid-tier producers. Small-cap and mid-cap companies, adds Markova, “are quicker to respond to changes and adjust their business plans.”

The AGF fund holds 95 names. One top name is RioAlto Mining Ltd., a mid-cap firm active in Peru that produces about 220,000 ounces of gold a year. “[Its] cash cost is US$700 an ounce,” says Markova, “so [it is] very profitable.”

RioAlto’s stock is trading at about $3.10 a share, or at its net asset value (NAV). Markova has a target of about $4 within 12 to 18 months.

Last year’s abrupt decline in the gold bullion price is reminiscent of what happened in 1999, following the signing of the so-called Washington Agreement, in which the European Central Bank and central banks of countries such as the U.K. agreed to limit bullion sales to 400 tons per annum for five years.

“Back then, we had a strong U.S. dollar, and dot-com stocks were the rage,” recalls Robert Cohen, vice president at Toronto-based 1832 Asset Management LP and portfolio manager of Dynamic Precious Metals Fund.

“But then, dot-com stocks fell,” says Cohen. “And people said they liked gold after all.”

The agreement marked a turning point, as bullion’s price spiked to US$350 an ounce and continued to climb for a decade.

Today, Cohen argues, we are at another inflection point, given that gold bullion is trading at about 13 times crude oil’s price of US$93 a barrel, vs the historical multiple of 15.

“The mentality of the market has calmed down, while ETFs still hold about 1,600 tons of gold,” says Cohen. “But last year’s 800-ton ‘shock’, when investors dumped gold en masse, is not likely to be repeated – and certainly not to that magnitude.”

The latter part of 2014 could be important, Cohen believes, as investors are likely to gain more confidence.

“Last year, stocks were oversold by at least 30%,” says Cohen, noting that in 2008, gold stocks sold at 1.7 to 1.8 times NAV. “If there is no change in the gold price, though, there isn’t a lot of ‘meat on the bones’ of gold stocks. They’re trading at reasonable multiples – from 0.8 to 1.2 times [NAV].

“I don’t expect to see the 2008 multiples for some time,” he continues, “or until the market gets very comfortable. But I won’t argue with the current regime of valuations; I’ll just accept it.”

Cohen is a bottom-up, value-oriented investor. About 39% of the Dynamic fund’s AUM is held in small-caps, 35% is in mid-tier players and 15% is in large-caps. From a geographical standpoint, about 76% of the holdings are in Canadian firms, with the balance in foreign firms.

Running a tight portfolio of 25 names, Cohen likes Roxgold Inc. That firm is active in Burkina Faso and developing the Yaramoko project, an underground mine producing high-grade ore that will have an estimated annual production of almost 100,000 ounces a year, beginning in 2016. Acquired about two years ago, Roxgold’s stock price has been on a roller-coaster because of management changes. “The stock,” says Cohen, “has come off the bottom very nicely.”

Roxgold stock is trading at about $0.85 a share, vs $0.45 last January. There is no stated target.

Normally, gold stocks run ahead of bullion, but stock prices have lagged the bullion price, observes Onno Rutten, vice president, investment management, with Toronto-based Mackenzie Financial Corp. and portfolio co-manager of Mackenzie Precious Metals Class Fund (working alongside Benoît Gervais, senior vice president at Mackenzie).

Rutten notes that the bullion price has dropped by 30% since August 2011, while the S&P/TSX global gold sector index has tumbled 47% over the same period. And both are attributable largely to lowered expectations for the bullion price.

“There was a fear that gold would continue to come down,” says Rutten, “because the ‘playbook’ for the market was that the economy was recovering, quantitative easing [QE] would be removed, and we would not need gold for insurance.

“But, early this year,” he continues, “there was a realization in the market that the exit from QE was not going to be that easy. The new chairwoman [of the U.S. Federal Reserve Board] was dovish and [indicated] she would rather err on the side of easing than tightening. The European Central Bank [ECB] went to an accommodative stance, lowering its rates.” Rutten notes that the ECB’s negative benchmark rate indicates how dramatic the European slowdown has been.

“Put all this together,” he adds, “and the expectations for gold and gold stocks substantially improved at the start of the year because of the realization that the ‘Goldilocks’ scenario of economic growth was not going to play out so easily. There was a renewed appreciation of the insurance and protection that gold can bring to a portfolio.”

Although Rutten is reluctant to make any forecasts on bullion’s price, he notes there has been a wide divergence in gold equities valuations: “Companies that have executed well have seen an upward revaluation, whereas those that are struggling to execute are seeing contractions of their multiples. That creates an environment in which active management can add value.”

Rutten has split the Mackenzie fund’s AUM more or less equally among small-cap, mid-tier and large-cap producers. One favourite name in the portfolio of 90 names is Detour Gold Inc., which is developing a mine in northern Ontario that has the potential to produce 600,000 ounces of gold a year.

“[The mine] has a 22-year reserve life,” he says, “and it’s in a low-risk jurisdiction.” Detour stock is trading at about $13.40 a share.

© 2014 Investment Executive. All rights reserved.