U.S. equities markets have been rising steadily since Donald Trump won the U.S. presidency last autumn, largely on the promise of tax cuts, deregulation and protectionist measures. Although some fund portfolio managers are cautious in their view that economic growth is accelerating, others are reluctant to make a call and focus instead on individual stocks.

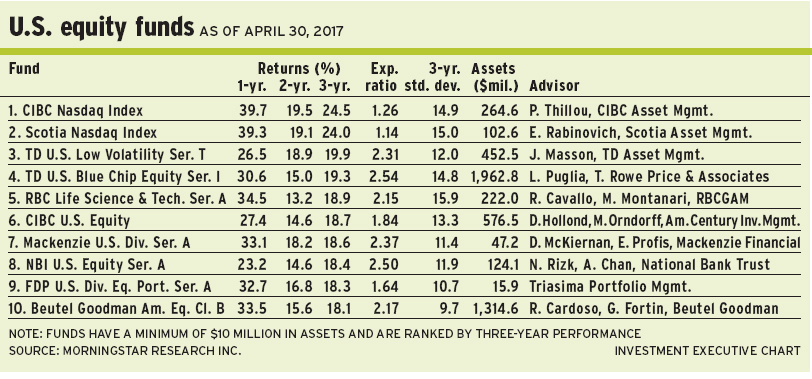

“The underlying assumptions that have driven strong stock performance are that we will have perhaps strong economic growth driven by lower corporate tax rates and less regulation,” says Larry Puglia, vice president at Baltimore-based T. Rowe Price Associates Inc. and portfolio manager of TD U.S. Blue Chip Equity Fund.

Although some pundits discredit the so-called “reflation” story revolving around the Trump administration’s efforts to boost the economy, Puglia argues that there is some merit to the case for reflation, but not to the extent that its proponents maintain.

“Reflation has a number of dimensions to it,” says Puglia. “People were very bullish on commodity price improvements, including the price of energy. That didn’t seem logical to us because the Trump administration is pushing for greater production of hydrocarbons in the Permian basin in the U.S. If anything, that will result in greater supply and perhaps subdued oil prices. Also, expectations for synchronized global growth may be overly optimistic.”

Nevertheless, Puglia points out, U.S. economic growth is picking up, consumer confidence is increasing and the housing market is trending upward: “To me, saying that we could have somewhat higher growth over time and moderately higher interest rates is not overly optimistic.” He adds that in 2017 U.S. gross domestic product could grow by 2.5%-3% in real terms.

“The people looking for very robust growth and very robust reflation probably are too optimistic. But I disagree with the inference that the reflation trend is dead. In fact, some of the banks are reporting fairly strong numbers and a lot of the Trump stocks, including certain consumer discretionary companies, appear to be well positioned.”

Puglia adds that if Congress reformulates a health-care bill, moves on to tax reform and completes these tasks relatively quickly, the financial markets are likely to respond positively to these key steps because they are believed to contribute to higher economic growth over time.

Although Puglia is muted in his bullishness on the U.S. economy, he believes that “there is a reasonable prospect for stronger growth if, in fact, we see [less] regulation and reform taxes, particularly corporate tax rates.”

As a rule, Puglia’s investment choices are not predicated on what happens in the political realm. Yet, in this case, he says, “What happens in the political backdrop is probably a little more important than it normally is to financial markets that’s from a perception standpoint and, ultimately, in reality.”

Although Puglia is cognizant of the risks on the downside, such as the impact of geopolitical conflicts with North Korea and central banks that are becoming less accommodating than in the past, the TD fund is fully invested. Puglia is a bottom-up, growth investor whose sector weightings are a byproduct of stock selection.

About 35.8% of the TD fund’s assets under management (AUM) is held in information technology, followed by consumer discretionary (24.5%), health care (17.4%), financials (9%) and industrials (7.8%), with smaller weightings in sectors such as real estate.

One top health-care holding in the 138-holding TD fund is Intuitive Surgical Inc., a provider of the da Vinci robotic surgery system used to repair inguinal hernias, which is a less invasive option than traditional methods. “[Intuitive Surgical] announced a new product, da Vinci X, which will be a more affordable version of the main robotic surgery platform,” Puglia says.

Intuitive Surgical stock is trading at about US$810.20 ($1,055.85) a share about 26 times 2018 earnings. Based on the firm’s consistently growing double-digit earnings, Puglia has a target of US$900-US$1,100 a share within 24 months.

Making a call on markets is almost impossible, says Rui Cardoso, vice president, U.S. and global equities, at Torontobased Beutel Goodman & Co. Ltd. and portfolio co-manager of Beutel Goodman American Equity Fund.

“For us, the right multiple of the market reflects the characteristics of each stock within the market, which is far too broad. For us, whether the market is expensive or not actually doesn’t matter. The way we look at the world is that we have 25 ‘gem’ assets,” says Cardoso. “When you build a portfolio like that and take a long-term view, it doesn’t matter what happens outside of those names.” (Cardoso works with portfolio co-manager Glenn Fortin, also vice president, U.S. and global equities, at Beutel Goodman.)

If the portfolio managers get most of those names right and do well on the downside, then the results will stand up, Cardoso says: “The outlook we have on the market is framed by this question: ‘How difficult is it to find these gems?’ We’d like to hold the names forever, although [our strategy] rarely works out that way.”

Cardoso and Fortin set a target price, based on a three-year view. “If the stock hits our target, we have a mechanism whereby we automatically sell one-third of the holding,” says Cardoso. Then the portfolio managers reassess the stock and question whether it’s good for another three years.

“If it’s a good business and has compounded extra value, we’ll continue to hold it,” says Cardoso. “If it pulls back, maybe we’ll add to it.” In some cases, the team will sell the stock and use the proceeds to fund other purchases.

There’s no doubt that with markets on an upward trend, finding new names has been hard. “In 2016, we added only two stocks. We have very high hurdle rates, in terms of what qualifies. We are very picky,” says Cardoso, noting, for example, that the portfolio management team added drug distributor Amerisource Bergen Corp. last year.

“The fact is that finding these gems, which are great businesses selling at deep discounts to their intrinsic value, is hard,” says Cardoso, adding that more stocks have been hitting their targets, which means the portfolio managers are trimming positions or even selling them.

Cardoso and Fortin try to avoid stocks that play into a macroeconomic event such as Brexit or the election of Trump. “Even if we were right on Trump’s election,” says Cardoso, “what that means for the economy is a big call. And what the economy means for these stocks, is another big call.

“There are too many linkages that you have to get right. There is too much out of our control,” he adds. “So, we’re only going to focus on what we can control, which is buying a great business that’s trading at a deep discount to its intrinsic value.”

Take, for example, the volatile crude oil price, which peaked at US$112 a barrel in June 2014, then sank to US$26 in February 2016, then gradually recovered to about US$50.

“We don’t know where it’s going. The only oil stock we own is Halliburton Co., a service company that makes its returns from oil drillers and producers,” says Cardoso. “Oil companies have to keep finding more oil, otherwise their business collapses. Halliburton makes a good return over the cycle and we’re comfortable owning [the stock].”

About 22.4% of the Beutel Goodman fund’s AUM is allocated to technology, 20.7% to health care, 19.1% to industrials and 19% to financials, with smaller amounts in sectors such as consumer defensive.

One top holding is Teradyne Inc. which makes semiconductor testing equipment. “It’s a ‘lumpy’ business, so you get big spurts of sales to chip manufacturers,” says Cardoso, noting that Teradyne has emerged with a market share of more than 50% after a lengthy period of industry consolidation. Teradyne stock is trading at about US$33 ($44.50) a share, or about 9.5 times forward enterprise value to earnings before interest, taxes, depreciation and amortization. Cardoso believes the stock still trades at a discount of more than 20% to its value.

© 2017 Investment Executive. All rights reserved.