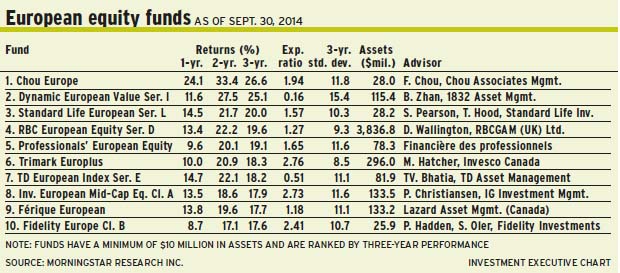

After a strong run-up in 2012 and 2013, European equities markets have been eking out modest returns (but flat in Canadian dollar terms), as economic growth has faltered this year. However, fund portfolio managers maintain that the region will pull through, and they are focusing on industry leaders that offer better prospects.

“The European economy is doing what it is supposed to be doing: moving slowly. But people should not be surprised,” says Benjamin Zhan, a portfolio manager with Toronto-based 1832 Asset Management LP, who oversees Dynamic European Value Fund. “Unfortunately, some people put too much hope in 2013. They were surprised, and started selling when it got late, which happens all the time with investors.

“So,” he continues, “it’s a matter of expectation, as opposed to what is really happening on the continent.”

Zhan argues that 2011 marked an inflection point for Europe, as governments and central bankers scrambled to restore confidence.

“The first foundations for a united Europe were put into place. The 17 members agreed to push through social reforms, which were very hard, and also put together a transcontinental financial tax and a banking supervisory body to monitor the banking system,” says Zhan, who works with Chuk Wong, vice president of 1832 Asset Management.

“The train is in motion; it’s started,” says Zhan. “But what we’re seeing now is the unwinding of what happened before 2011.”

Among the developments Zhan points to is the reversal of the position of Germany’s chancellor, Angela Merkel, who says she now is committed to keeping Greece in the European Union (EU). Meanwhile, Mario Draghi, head of the European Central Bank, says he will do anything it takes to save the EU. And authorities in Brussels have given banks more breathing room. “The difference today is that the train is in motion,” says Zhan.

“What are the implications?” he asks. “In the past, every time there was a market rally, it was followed by a sell-off. If you believe, as I do, that the trend is up, then every correction is a buying opportunity because Europe is moving in the right direction. It’s just a bumpy ride now.”

Zhan, a bottom-up, value investor, has allocated about 23.2% of the Dynamic fund’s assets under management (AUM) to the U.K., 20.3% to Germany and 13.3% to Italy, with smaller weightings to countries such as France and Switzerland.

On a sector basis, the Dynamic fund is dominated by consumer discretionary (44.5% of AUM), followed by industrials (26%), financials (12.5%) and smaller exposures to sectors such as consumer staples and information technology.

Among the top holdings in the 53-name Dynamic fund is Swatch Group AG, the Switzerland-based maker of luxury watch brands such as Omega.

“[Swatch] is protected by brands that have been built over centuries and no one can take away,” says Zhan, adding that the firm traces its roots back to 1735. “[Swatch] has survived management missteps and technological changes. But every time it fell, it came back stronger.”

Swatch stock is trading at about 454 Swiss francs ($533.30) a share, or roughly 15.8 times earnings. There is no stated target.

Markets are in “catch-up” mode, argues Michael Hatcher, vice president and head of global equities with Toronto-based Invesco Canada Ltd. and portfolio manager of Trimark Europlus Fund. Hatcher works alongside Matt Peden, portfolio manager with Invesco Canada.

“At the end of the significant rally in 2013, valuations got into ‘very fair’ territory,” says Hatcher. “If anything, the underlying economies and earnings are just starting to consolidate and may be catching up. Thirty per cent gains in 2013 are not the long-term expected investment return; it’s more mid- to high single digits.”

Europe will continue to recover gradually for the foreseeable future, says Hatcher: “The fact that some quarters are up a bit and then they pull back a little bit says Europe is muddling along. I don’t see any significant acceleration or significant slowdown.

“There will always be news items and the media will say things are changing drastically,” Hatcher continues. “But when you add up all the quarters and combine them on an annual basis, you can see a slow and steady progression. We’ll ultimately be on a better footing. After all, we are coming off a significant financial crisis that will take a long time to work out.”

Still, Hatcher admits, valuations are elevated. Thus, cash in the Trimark fund comprises about 16% of AUM.

“I’m looking for businesses that have strong and stable cash flows,” says Hatcher. “Some businesses in this market are above fair valuation, especially those that have a cyclical component and [have] gotten ahead of themselves. We’ve lightened up [in] some of the names that may have more exposure to the economic cycle, and put more money to work in businesses that have stable cash flows.”

Hatcher is a bottom-up, “growth at a reasonable price” portfolio manager. About 20.6% of the Trimark fund’s AUM is in the U.K., 17.3% is in Switzerland, 9.3% is in Ireland and 8.9% is in Germany, with smaller weightings are in countries such as France.

From a sector viewpoint, there is 34.3% of AUM in consumer staples, 14.9% in health care, 11.2% in information technology, and smaller exposures in sectors such as consumer discretionary.

One favourite name in the concentrated Trimark portfolio of 28 holdings is Henkel & Co. AG, a Germany-based firm that is the world’s largest producer of industrial adhesives.

“[Henkel is] two-and-half times larger than [its] nearest competitor, and no one else has the breadth of products,” says Hatcher. “Adhesives are a very small-cost component, but their functionality is critical. You don’t take a risk by going to a secondary supplier if you can have the best-in-class.”

Henkel stock is trading at about 80.70 euros ($109.50) a share, or 15 times forward earnings. There is no stated target.

Another favourite is Anheuser-Busch InBev SA, the world’s No. 1 brewer, known for brands such as Budweiser and Stella Artois.

“There’s low single-digit volume growth in the [brewing] industry,” says Hatcher. “But 55% of InBev’s [earnings before interest and taxes (EBIT)] comes from the emerging markets. You’re getting stronger volume and pricing growth in markets such as Brazil and Mexico.”

Listed on the New York Stock Exchange, InBev American depositary receipts are trading at about US$112 ($125.55) each, or about 20 times 2015 earnings.

There have been several negative cross-currents affecting European markets, says Dominic Wallington, chief investment officer at London-based RBC Global Asset Management (U.K.) Ltd. and portfolio manager of RBC European Equity Fund.

“There have been events in Ukraine and some slightly weaker economic data,” says Wallington. “France has stalled, and Germany had a bit of blip in the first quarter. But countries such as Spain are rebounding more quickly than expected, Scandinavia remains very firm and the U.K. is one of the fastest-growing countries in the developed market. It’s a mixed picture. And in the mix, we are still relatively positive.”

Wallington adds, however, that it’s important to separate European companies’ revenue from overall gross domestic product numbers because more than 50% of company revenue originate outside the region. “The pan-European economic indicators are still positive,” he adds. “But Europe is never as simple as that.”

Wallington is optimistic that Europe is on track for economic recovery, based on programs such as the Long-Term Credit Refinancing Operation, which is a cheap-loan program for European banks that starts in September and will be followed by another round in December.

“There is always the possibility of quantitative easing, if need be,” says Wallington. “I still think there are a number of tools in the tool box, especially if you put it in context with actions taken by other central banks. Obviously, it’s more complicated to get the European Central Bank moving in one direction – because Europe is more complicated than a single state, like the U.K. But there is still room to manoeuvre.”

Wallington is a bottom-up investor who focuses on industry-leading companies. About 16% of the fully invested RBC fund’s AUM is in health-care firms, 15.4% is in financials, 13.8% is in consumer staples, 13% is in industrials and 13% is in consumer discretionary.

From a geographical perspective, about 38% of AUM is in the U.K., 9.5% is in Switzerland, 9% is in the Netherlands, with smaller weightings in Germany and Spain.

One top holding in the 60-name RBC fund is Reed Elsevier NV, a Netherlands-based firm that is the world’s leading scientific publisher.

“[Reed Elsevier] is the world’s fourth-largest digital-content provider,” Wallington says, “which gives you an idea of the scale. And 11 million scientists use its products and download 700 million articles a year.”

Reed Elsevier boasts a 30% EBIT margin, Wallington adds, and its return on equity is 49%: “There is a bull market in technology at the moment, and Reed Elsevier is in the sweet spot.”

Reed Elsevier stock, which has a 3% dividend yield, is priced at about 18 euros ($25.50), or 15 times future earnings. There is no stated target.

Another favourite is Christian Dior SA, a France-based holding company that operates six divisions, including Christian Dior Couture, wines and spirits with brands such as Moët & Chandon champagne, and Louis Vuitton leather goods.

Christian Dior stock is trading at about 132.70 euros ($192) a share, or 16.7 times 2015 earnings. The stock also boasts a 2.7% dividend yield.

© 2014 Investment Executive. All rights reserved.