Asia-Pacific markets have performed well in the past 12 months, with earnings momentum drawing in more investors. Although there are concerns that China’s economy may slow more than anticipated and Japan’s reforms may not deliver on their promises, portfolio managers generally are bullish on prospects for the region.

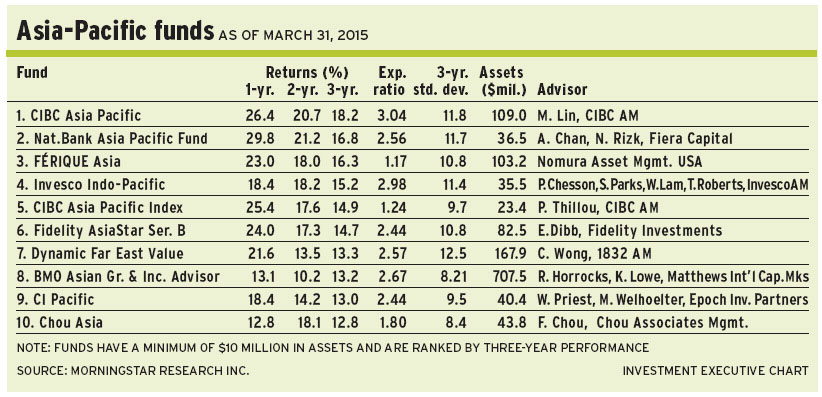

Portfolio managers, such as Mark Lin, vice president, international equities, with CIBC Asset Management Inc. in Montreal and manager of CIBC Asia-Pacific Fund, believe that although the growth of China’s economy is slowing, policy-makers are ensuring a so-called “soft landing.”

“The Bank of China still has levers to guide the economy,” says Lin, adding that China’s credit cycle still is in the early to middle stages. “The [central bank] can reduce interest rates or give the banks more flexibility in terms of their reserve ratios. And the government can still spend money on the fiscal front. In fact, they have spent money on projects such as high-speed rail and also lowered interest rates to counter the continuous economic slowdown.”

But now that China is the second-largest economy in the world, Lin says, “we’re seeing the law of large numbers: China cannot grow at the [double-digit] rate of the past. And there are qualitative constraints, in the form of dealing with very high rates of pollution in cities such as Beijing.”

Lin notes that growth in China’s gross domestic product (GDP) this year may be slightly less than the official target of 7%. “But every time China slows a bit,” he adds, “policy-makers step in. China is pretty much the only country that can do that. I’m still optimistic. Even if [GDP] grows by 6.8%, that’s still pretty fast; that’s a respectable rate.”

Conversely, Lin remains skeptical of Japan’s effort to turn around its economy, even in the face of a rebounding Japanese stock market that has cheered on the so-called “Abenomics” (named after the stimulative economic policies of Prime Minister Shinzo Abe).

“We have not seen the GDP numbers being significantly better since they implemented quantitative easing (QE), and we’ve seen two rounds of QE so far,” says Lin. “It has surprised me that the market reacted so favourably on monetary policy rather than the real fundamentals. We invest on the fundamentals. And our performance has not been hurt by our relatively low Japanese weighting.”

Lin is a bottom-up investor. About 25.4% of the CIBC fund’s assets under management (AUM) is invested in Australia, vs 13.8% of the benchmark MSCI all country Asia-Pacific index; 25.5% is invested in Japan (vs 40.3%); 25% in Greater China, which includes Hong Kong (18%); and 13.3% in Indonesia (1.5%); with smaller exposures to countries such as India.

One top holding in the 37-name portfolio is TPG Telecom Ltd., an Australia-based provider of high-speed broadband service. “It’s a smaller but very nimble player that is able to take market share from the large incumbents,” says Lin.

TPG’s stock is trading at about A$9.45 ($9) a share, and pays a 1% dividend. There is no stated target.

eileen dibb is a portfolio manager with Pyramis Global Advisors in Smithfield, R.I., a division of Boston-based FMR LLC (a.k.a. Fidelity Investments). She oversees Fidelity AsiaStar Fund.

From a macroeconomic perspective, she attributes some of China’s slowing GDP growth to rising wages, which have reduced foreign investment. And, she adds, “Fiscal spending on infrastructure is no longer as robust, which is also a drag on the economy.

“And there’s the issue of the sheer size of the Chinese economy, as the effect of large numbers start to kick in,” says Dibb, echoing Lin’s comments.

“We also have to remember that in 2009-10, there was a lot of fiscal stimulus, which artificially increased numbers,” Dibb says. “At this point, the Chinese government is intent on getting to a normalized growth level. It’s not the pace that matters, but the sustainability. Even at 6%, that’s pretty good growth for an economy as big as China’s.”

She adds that valuations in the region are reasonable, and stocks are trading in the low- to mid-teens, depending on the market.

As for Japan, Dibb is bullish and counts many positive developments. “There are a slew of new measures put out by the government that are meant to make companies more profitable,” says Dibb, noting that the Abe administration is pushing companies to achieve a return on equity greater than 8%.

The government also is encouraging firms to adopt corporate governance measures, such as voting proxies or new stewardship codes, she says: “There is a big push by the government that’s meant to change corporate behaviour in a way that is good for shareholders. That’s very different from what existed in Japan before Abenomics. Even though the jury is out on [these policies’] effects on the economy, the changes have allowed companies to be much more profitable.”

Dibb is largely a bottom-up, “growth at a reasonable price” investor. About 41% of the Fidelity fund’s AUM has been allocated to Japan, 11.5% to Hong Kong, 8.1% to China, 7.8% to Taiwan and 7.6% to Australia, with smaller weightings to countries such as South Korea.

One favourite name in the 120-name fund is Amcor Ltd., an Australia-based mid-cap producer of rigid and flexible plastic packaging. The firm generates about one-third of its sales in emerging markets. “[Amcor is] a reasonably ‘growth-y’ company with relatively low volatility,” says Dibb, noting that the firm generates a return of about 10% a year, including dividends. As most of its growth is in the consumer staples area, she adds, “it’s a relatively defensive name.”

Amcor stock is trading at about A$14.20 ($13.55) a share and pays a 3.4% dividend.

The Asia-Pacific market has more room to run because its earnings recovery has lagged the U.S. by a fair margin, argues Chuk Wong, vice president with Toronto-based 1832 Asset Management LP and lead portfolio manager of Dynamic Far East Value Fund.

“If you look at past performance over several years, Asian stocks are coming off a lower base, whereas the U.S. has had a six-year bull run,” Wong says.

“I’d be more concerned about the U.S. than the rest of the world. If you believe that stock prices reflect the underlying fundamentals, then Asia and Europe are still in the very early stages of earnings recovery. The downside from [this level] is more limited.”

When comparing valuations, Wong maintains that Asia-Pacific stocks are trading at 13.5 times earnings vs 17 times for the U.S. “This shows how cheap Asia is compared with the U.S.,” he says, adding that the discount is attributable to weaker earnings and higher interest rates in the Asia-Pacific region than in the U.S. “I expect that the valuation gap between Asia-Pacific and the U.S. will narrow going forward.”

Turning to China, Wong believes that its transition from an export-driven model to one that is domestically oriented is a process that may take many years: “It won’t change overnight. And I see that the growth on domestic, consumption-oriented side is doing a little better than the investment and export side. To me, that’s a very healthy indicator. That being said, this transition comes with slower growth. But it will make China a lot healthier going forward. So far, we have had a soft landing. I expect that situation to continue.”

Wong is skeptical of prospects in Japan and notes that strong market performance has been driven by a weak yen relative to the U.S. dollar.

“The rally has not been structurally driven. It’s the same old faces, such as Toyota Motor Co., and has not spilled over into many smaller-cap stocks. I’m looking for structural changes that would make Japanese companies more competitive and efficient. I’m still cautious.”

Wong is a bottom-up value investor. About 17% of the Dynamic fund’s AUM has been allocated to China, 13% to Thailand, 12% to Taiwan and 11% to Japan, with smaller allocations to countries such as Australia and India.

Running a portfolio with about 70 names, Wong likes Kweichow Moutai Co. Ltd., a Shanghai Stock Exchange-listed, large-cap maker of alcoholic beverages that is best known for production of baiju, the bestselling type of liquor in China.

“[Kweichow] is very underappreciated and trades at a 35% discount to its global peers, such as Diageo PLC,” Wong says.

Kweichow’s stock trades at about CNY196.65 ($39.80) a share. There is no stated target.

© 2015 Investment Executive. All rights reserved.