After a difficult 2013, which saw interest rates spike upon concerns that the U.S. Federal Reserve Board would end its quantitative easing program sooner than expected, Canadian fixed-income markets settled down and year-to-date returns have been positive.

However, portfolio managers of Canadian bond funds urge caution and are favouring corporate bonds because rising rates are on the horizon once more.

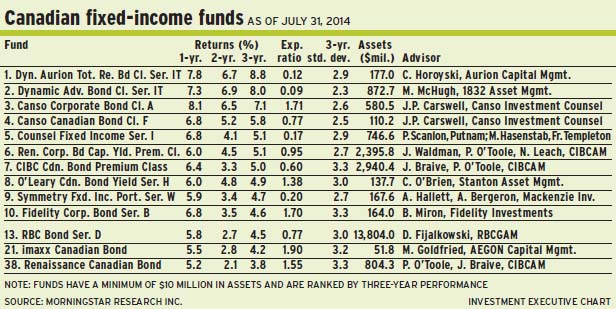

“Fixed-income has outperformed expectations this year. But it’s not inconceivable that rates will [go] back up,” says Dagmara Fijalkowski, senior vice president and head of global fixed-income at Toronto-based RBC Global Asset Management Inc., and lead manager of RBC Bond Fund. “And if yields back up, even by 35 basis points [bps] over the next 12 months, it would erase the gains in the Canadian bond universe. It wouldn’t take much to do that.”

Yet, Fijalkowski says, the key questions are: why are bond yields so low; and what has pushed them even lower?

“It’s not due to growth or the fact that there are lower inflation expectations,” says Fijalkowski. “It’s that there were additional surprises in terms of supply and demand for bonds. Part of that comes from a flight to quality due to geopolitical tensions, such as [those in] Ukraine and Iraq. Another factor is that the global allocation of savings and reserve assets held by foreign-exchange managers and sovereign wealth funds have been growing faster than we expected.”

The U.S. treasury market, she adds, has been a key beneficiary of massive foreign inflows, thus suppressing yields.

Then there is Europe, which has seen a combination of falling growth and inflation expectations, causing the European Central Bank to lower its benchmark rate to an unprecedented minus 0.1%.

“The global fixed-income market is interconnected,” says Fijalkowski. “It’s hard for U.S. treasury yields to increase when yields on 10-year German bunds are 1%. By comparison, 10-year U.S. treasuries, which yield 2.4%, seem like high yield.”

Despite this backdrop, Fijalkowski’s base-case scenario anticipates that yields will move higher gradually in 2015 and in slower increments: “Unless, of course, there is a surprise in terms of growth, and the Federal Reserve changes its tactics. For now, the Fed appears to be very cautious about the pace of increase. Rates have not even reflected, so far, the pace that the Fed indicates – and to us, the [Fed] has indicated [rising rates] will start in mid-2015. If we take the Fed at their word, fixed-income markets should price that in – but they haven’t yet.”

Given the environment, Fijalkowski is keeping average duration in the RBC fund at about 6.7 years, slightly shorter than the benchmark FTSE TMX Canada universe bond index’s 7.2 years. “This reflects our base-case scenario,” she explains, “that interest rates will go higher.”

The RBC fund has an over-weighted 43% of its assets under management (AUM) in corporate bonds; Fijalkowski favours the higher yields that asset class offers. Also, there is an underweighted 50% in government bonds (split 40%/10% between provincial and federal bonds) and 6.5% in cash.

Highly diversified, the RBC fund has more than 600 holdings, although the top 25 account for about 35% of its AUM. Representative of the investment-grade corporate-bond allocation are a Bank of Nova Scotia bond maturing in 2019, rated AA, yielding 2.23% to maturity; and a Bell Canada bond maturing in 2018, rated BBB-plus, and yielding 2.17% to maturity.

Benchmark U.S. 10-year yields were expected to rise to 3.6% by the end of 2014, but that clearly hasn’t happened, notes Marc Goldfried, chief invest officer and head of fixed-income with Toronto-based AEGON Capital Management Inc., and lead manager of imaxx Canadian Bond Fund.

“This view was based on a continued upward trajectory of economic growth, a pickup in inflation and some tougher language out of the Fed in terms of a removal of stimulus and zero- interest rate policy at some point,” Goldfried says. “The majority of prognosticators and asset managers also had that view.”

Yet, economies have confounded many people, adds Goldfried, as a result of a number of factors. One is a weak first quarter that suppressed yields, combined with a flight to quality in the wake of geopolitical tensions. In addition, Goldfried notes, U.S. bond yields are considered “cheap” vs German and Japanese bond yields, and central banks in other countries have bought U.S. dollars to keep their currencies low and their industries globally competitive.

“And despite reasonable improvements in U.S. employment,” Goldfried says, “the Fed’s chairman continues to be pessimistic about the outlook for employment. Janet Yellen keeps talking dovish, so the market keeps pushing out the forecast when administered rates will move higher.”

In Goldfried’s view, the benchmark U.S. 10-year yield will climb from its current 2.4% to hover between 2.75% and 3% by yearend.

“The U.S. economy appears to be on a sustainable upward trajectory. We see a huge turnaround in growth in the second quarter and a pickup in inflation fundamentals,” says Goldfried, adding that the U.S. market will define the direction of the Canadian bond market. “With U.S. growth in 2014 averaging about 3% and a 2% inflation rate, it’s hard to say there is value in the risk-free rate of return. We see bonds as expensive. Rates will back up and there will be some degradation of returns [for 2014].”

Goldfried is maintaining a relatively neutral average duration of 7.1 years and has allocated about 90% of the imaxx fund’s AUM to corporate bonds to maximize the greater upside from that area.

“Risk premiums, or spreads, have compressed a great deal in 2014,” Goldfried says. “We’re concerned about valuation, mostly on high-yield but less so on investment-grade.” He adds that default rates are low and not a concern because balance sheets are generally strong: “Investment-grade is OK, but we are approaching fair value on spreads.”

The imaxx fund holds bonds from 25 corporate issuers, 15 asset-backed securities and five Government of Canada bonds. Among those holdings is Canadian Western Bank’s BBB-rated bond maturing in 2019 and yielding 2.8% to maturity. Other holdings that will capture the upside of an improving economy include bonds from Aimia Corp., a leading global loyalty-management firm, which has a 2019-dated BBB-rated bond yielding 3.1% to maturity, and Pembina Pipeline Corp., which has a BBB-rated bond maturing in 2044 and yielding 4.45% to maturity.

Yields will move a little higher before yearend, agrees Patrick O’Toole, vice president with Toronto-based CIBC Asset Management Inc. and lead portfolio manager of Renaissance Canadian Bond Fund. He shares portfolio-management duties with John Braive, vice chairman at CIBCAM.

“We’re not expecting any gains from here in the bond market,” says O’Toole. “It will be more reserved. The U.S. economy struggled in the first half [of 2014], but the signs are there that the second half will be better. That will help reverse some of the downward pressure on interest rates in the first half of the year. That pressure was driven to some extent by geopolitical tensions that formed with the Ukraine/Russia conflict and Iraq. Those tensions may abate and allow interest rates to rise a little.”

O’Toole expects that during the next two or three fiscal quarters, bond yields will increase by about 50 bps. “The Canadian economy has been fairly steady at about 2% [gross domestic product] growth, but U.S. looks to have better momentum than that,” says O’Toole. “Not that it will be great in the U.S. in the second half. But there will be less pressure for Canadian yields to rise.”

Key to O’Toole’s forecast is that when rates start to rise, the increase will be very gradual: “The end point in the Fed funds rate, or when it finishes raising rates, will be much lower than what you’ve seen in the past.” O’Toole, expects the Fed to start raising rates in mid-2015. “The Fed is trying to convince the bond market that that will be the case. But if inflation gets out of hand, then the bond ‘vigilantes’ will be back and force the Fed’s hands sooner than it would like.”

Deflationary pressures, which act to suppress inflationary trends, have been abating in North America, although not in Europe, O’Toole adds: “We’ve seen house prices move higher [in North America] and wages starting to pick up a little bit. There’s not a lot to be concerned about inflation at the present time. But the day of inflation getting stronger is much closer than it was one or two years ago. We’re five years into this [economic] recovery, and we have gone through a significant healing period.”

In terms of average duration, O’Toole has positioned the fund at 6.75 years, or about a half-year shorter than the benchmark.

Like his peers, O’Toole favours investment-grade corporate bonds. About 53% of the CIBC fund’s AUM is in those investments, 13% is in high-yield bonds, 30% is in government bonds and 4% is in cash.

“Our view is that investment-grade and high-yield will outperform Canadas over the next 12 months,” says O’Toole, adding that investment-grade corporates may outperform by 1.5 percentage points; and high-yield bonds, by five percentage points.

On the investment-grade corporate side, O’Toole likes North West Redwater Partnership, a joint venture in the oilpatch between the Government of Alberta and Canadian Natural Resources Inc., which has a 2024-dated, BBB-rated bond yielding about 3.2% to maturity.

© 2014 Investment Executive. All rights reserved.