Even though turmoil surrounding China’s economy has upset financial markets, investors have shunned the traditional safe investment haven of gold bullion. As a result, precious metals mutual funds have taken a beating.

Yet, fund portfolio managers believe the worst may be behind them as they focus on companies that have attractive valuations in the face of a weak gold price.

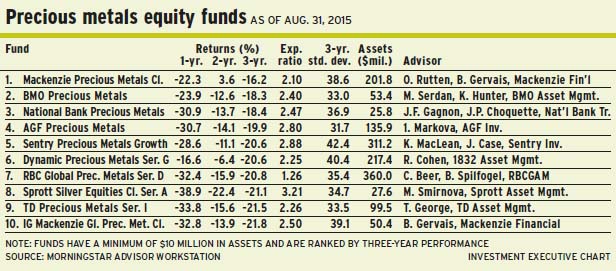

Gold’s weakness is the result of the market believing that the U.S. Federal Reserve Board will initiate an interest-rate hike cycle very soon, argues Onno Rutten, vice president with Toronto-based Mackenzie Financial Corp. and portfolio co-manager of Mackenzie Precious Metals Fund. Rutten shares portfolio-management duties with Benoît Gervais, Mackenzie’s senior vice president, investments.

That move in interest rates could increase the opportunity cost for holding gold, which currently is priced at about US$1,120 an ounce (vs US$1,200 a year ago), says Rutten.

“If real rates become positive [or higher than inflation], you can earn a better return from other assets. Gold does not pay interest or dividends,” says Rutten, adding that the end of quantitative easing in the U.S. in May 2014 also has held back gold. “That’s why the [bullion] price has declined.”

In addition, common wisdom says that because there is an inverse relationship between commodities and the U.S. dollar (US$), commodities prices have dropped against the strengthening U.S. greenback.

“Gold has been a collateral victim,” says Rutten, noting that speculators have exited from commodities funds and futures. “But I am not a believer that gold trades inversely against the US$. Historically, in certain periods, gold has traded positively against the US$; and in other periods, gold has traded negatively. There are [many] drivers. But gold has been part of the commodity complex, so it has been hit.”

The gold price may weaken further, Rutten says: “We are somewhat cautious on gold. In the near term, that rate hike is likely going to happen. Until we have that move behind us, gold still could be under pressure.”

As a result, gold could go as low as US$1,050 an ounce, he says; but, given more favourable circumstances, could rise to US$1,400 an ounce. Supporting factors would be the realization that the Fed cannot hike rates much further beyond its initial hike, given sluggish global economic growth and relentless currency devaluation in Japan, Europe and emerging markets.

Rutten notes that as the median all-in cost for gold production is about US$1,150 an ounce, many mining companies are struggling to break even: “If gold stays at this level, I see substantial restructuring, and mergers and acquisitions – with the caveat that often it will be a ‘take-under’, not a ‘takeover.’ On the other hand, there are firms with long-life gold reserves that are viable at US$1,100 an ounce and are extremely attractive.”

About one-third of the Mackenzie fund’s assets under management (AUM) is held in large-caps, one-third is in mid-caps and one-third is in small-cap exploration firms.

One favourite name in the Mackenzie fund’s 70 to 80 holdings is Detour Gold Corp., which is developing a northern Ontario mine that has a 20-year reserve life. Detour stock is trading at about $13.20 a share, or 8.7 times enterprise value (EV) to earnings before interest, depreciation and amortization (EBITDA). Rutten says the stock has 40%-60% upside.

Historically, gold and gold stocks don’t do well leading up to an interest rate hike, says Chris Beer, vice president with Toronto-based RBC Global Asset Management Inc. (RBCGAM), and portfolio co-manager of RBC Global Precious Metals Fund. Beer shares portfolio-management duties with Brahm Spilfogel, vice president of RBCGAM.

“The perception is that a rise in interest rates is more beneficial for bonds and other assets because gold does not pay a dividend,” says Beer. “Today, with 10-year U.S. treasuries paying about 2.15% and inflation at 1.5%-2%, that means you have negative real rates. Until the Fed raises rates, gold will be under pressure.”

Still, Beer argues, the rate hikes could be modest, as U.S. gross domestic product (GDP) growth has averaged about 2% for several years, while Europe’s GDP is weak, at 1%, and China’s GDP is likely to come in at below 5% in 2015.

“I can’t see global GDP next year at such a level that will warrant the U.S. to jack rates to a high level,” says Beer. “Once we get the first or second rate hike out of the way, we have to see what it will do. In the next six to 12 months, I think bullion and gold stocks will do well. They’re forming a bottom from here as we begin to see this rate hike.”

From a valuation perspective, Beer argues that stocks are cheap – multiples have collapsed to six to eight times EV to EBITDA from 10 to 12 times just two years ago. On a net asset value (NAV) basis, stocks sit at around NAV, vs three times NAV a few years ago.

“Unless that gold price goes much lower, these [stocks] look intriguingly cheap for the first time in many years,” says Beer, who argues that the direction for gold prices is upward, although he’s not calling for US$1,800-an-ounce gold any time soon. “If you’re buying gold stocks now, over the next couple of years, you have a chance that the gold price will be higher.”

About 25% of the RBC fund’s AUM is held in large-cap names, 50% is in mid-caps and 25% is in small-caps. “The sweet spot for better performers has been companies that can increase their production and reserves and, ultimately, their cash flow,” Beer says. “Typically, we buy companies that are profitable in the lowest quartile of the cost curve of the commodity. That [strategy] has lent itself to the mid-caps.”

Running a portfolio with about 55 names, Beer likes large-cap firms such as Goldcorp Inc.: “[It has] the strongest balance sheet in the group and the most transparent management structure.”

Goldcorp stock is trading at about $18 a share and pays a 1.7% dividend. There is no stated target.

THE RESOLUTION OF GREECE’S debt crisis was partly responsible for the sell-off in gold and gold-based exchange-traded funds, as was slowing demand for commodities from a weakening China, says Ani Markova, vice president with Toronto-based AGF Investments Inc. and portfolio manager of AGF Precious Metals Fund.

“But most important,” she says, “I believe we are in this vortex of extreme investor pessimism in the gold space because of the currency issues. Currencies have been a major contributor to all this rejigging of various asset classes. Gold seems to be the barometer against which all these currencies are measured.” Markova adds that gold may be down in US$ terms, but has risen to $1,485 an ounce vs the slumping loonie.

Markova, like her peers, points to the Fed as one of the main sources of pessimism surrounding gold: “The question is: ‘What would a rate hike mean to global growth, and will the Fed actually move?’ There is a lot of uncertainty about the timing and magnitude of the rate increases. I believe that once that uncertainty is eliminated, we will see a rally in this space because it’s so crushed.”

Still, Markova believes that in a slow-growth global environment, U.S. interest rates will not move in a significant way and that the gold price will be “range-bound” between US$1,100 and US$1,300 an ounce over the next 18 months.

“To see a meaningful rise in the gold price, we need to see the signs of inflation coming in,” she says. “We are not seeing that because the velocity of money still is very low. There still is a bit of slack in the system and, slowly but surely, we are moving there – but in a slower than anticipated rate.”

About 25% of the AGF fund’s AUM is held in large-caps, 10% is in mid-caps, 55% is in small-caps, 5% is in gold bullion and 5% is in cash.

One top holding in the 75-name AGF portfolio is Agnico Eagle Mines Ltd., which produces about 1.6 million ounces a year from mines in Mexico and northern Canada. “[Agnico Eagle has] great depth of talent in [its] management team,” says Markova. “[The firm continues] to do what [it does] best: optimize operations, drive costs down and look for other high-quality opportunities.”

Agnico Eagle stock trades at about is $29.65 a share (about 6.2 times EV to EBITDA) and pays a 1.3% dividend. Markova has a target of about $43 a share within 12 to 18 months.

© 2015 Investment Executive. All rights reserved.