Despite headwinds in the form of rising longer-term interest rates and the U.S. Federal Reserve Board’s decision to start reducing its bond-buying program, high-yield bond funds performed relatively well last year, thanks to their improving economic fundamentals. Portfolio managers are veering between caution and optimism that returns will remain positive.

“It’s been a good year in general,” says Derek Brown, vice president with Fiera Capital Corp. in Toronto and portfolio co-manager of Altamira High Yield Bond Fund. “The economy has been good and corporate balance sheets have been improving. Quantitative easing [QE] gives access to near-free money. And spreads have narrowed.”

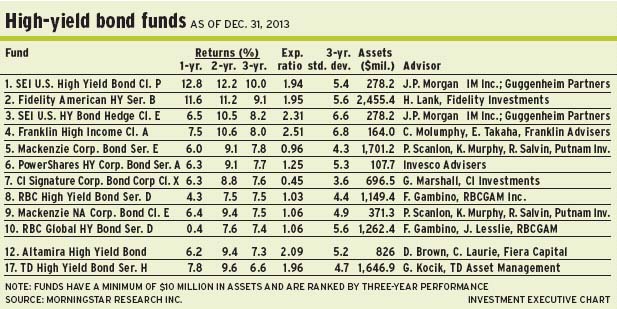

The spread over similarly dated U.S. treasuries has narrowed to about 430 basis points (bps) after spiking at 560 bps in June 2013, when the high-yield market flared up due to expectations that the Fed would “taper” its QE bond-buying program.

Looking ahead, however, Brown is cautious: “Valuations are at the point at which the market is fairly priced. Fundamentals need to get better, retail spending needs to go up and employment has to improve. We’re not quite seeing these things just yet. I’m constructive, but not overly constructive.” (Brown shares portfolio-management duties with Christopher Laurie, vice president of Fiera.)

Brown believes that the U.S. economy will improve in 2014 as its real gross domestic product growth accelerates to 2.75%-3%, vs 2.2% in 2013. “Over the next year, the consumer will come back into the market, but we’re not super-bullish,” he says. “We see a long, slow recovery and QE or tapering will be done by the end of 2014.”

As the economy improves, Brown expects the benchmark 10-year U.S. treasury yield to climb to about 3.25% by the end of 2014 and keep rising to about 4%-4.5% in 2016-17. “The Fed talks about the normalization of interest rates,” he says. “That’s what we’re heading into.”

About 42% of the Altamira fund’s assets under management (AUM) are in BB-rated bonds, 45% is in B-rated bonds, and 13% is in CCC-rated issues. As 85% of AUM is in U.S.-dollar (US$) denominated bonds, that portion is hedged back into Canadian dollars (C$). The fund’s average duration is four years, vs 4.32 years for the benchmark Bank of America Merrill Lynch high-yield master II index.

Running a portfolio holding about 120 issues, Brown prefers firms such as Cequel Communications Holdings LLC, whose subsidiary Suddenlink provides cable-TV and high-speed Internet access, primarily in the southern U.S. The Altamira fund holds two B-rated Cequel issues, with the 2020-dated bond yielding 5.8% and the 2012-dated bond yielding 6.1%.

Greg Kocik, managing director at Toronto-based TD Asset Management Inc. and portfolio manager of TD High Yield Bond Fund, believes that high-yield bonds will be less vulnerable to inevitably rising interest rates than government bonds. “As people realize that the reason why the Fed has been removing the stimulus,” he says, “[which is] because the economy is stronger – which translates into strong companies – that’s good news for bondholders.”

As tapering commences, Kocik adds, “We see the economy continue to grow unaffected, and profits correspond to that growth. Then people will actually continue to bid for high-yield bonds because default rates are expected to be quite low in this environment.” The default rate now is about 2% of the market, he adds: “That is close to the all-time lows.”

Looking down the road, Kocik is optimistic, although he maintains that returns will be coupon-like – around 6% before fees.

“Right now,” he says, “we’re close to the low end of the range, as far as the spread [over treasuries] is concerned. But compared with five-year government bonds that pay about 1.4%, high-yield bonds are quite attractive.”

His bullishness is based on the fact that the cost of borrowing is very low, which frees up a lot of cash to service corporate debt – and U.S. companies have become better at managing free cash flow.

Still, Kocik does see headwinds in the form of political disunity in the U.S. and the fallout from weakness in emerging markets: “There are concerns that they have not made major reforms. Countries such as Brazil are having a hard time dealing with inflation – and higher interest rates. If that gets worse, it could spill over into other asset classes, including high-yield bonds.”

About 55% of the TD fund’s AUM is in B-rated bonds, 34% is in BB-rated, and 11% is in CCC-rated issues. Kocik is keeping average duration low, at around 3.7 years. From a currency perspective, about 90% of the U.S. bond exposure is hedged back into C$.

“We spend more time on credit analysis than interest rate exposure,” he says. “But the reason the duration is lower is that it’s more an expression of value. It’s a bottom-up decision. When we compare a company with a five-year bond yielding 5% vs a 10-year bond yielding 5.5%, we see more value in the five-year bond.”

Running a portfolio holding bonds from about 140 issuers (some of which have multiple bonds), Kocik likes Lear Corp., which makes seating for the automotive industry. The TD fund is invested in a 2023-dated Lear bond, rated BB-plus and yielding 5.5%. Lear uses a lot of its free cash flow to buy back shares, but Kocik anticipates that will moderate and the firm will try to qualify for investment-grade (BBB) status.

“For this to play out,” Kocik says, “we need about three years of reasonable auto industry sales.”

Frank Gambino, vice president with RBC Global Asset Management Inc. and lead portfolio manager of RBC High Yield Bond Fund, also is upbeat about prospects for 2014: “Corporate balance sheets remain healthy. Although there is some deterioration, it’s not at a point at which we see a turn in the credit cycle. Defaults are low but could trend slightly higher over the next couple of years. Barring a major recession, we could be in a fairly favourable environment for the next one to two years.”

There is good demand for high-yield bonds, mostly from institutional investors, says Gambino, who shares duties with portfolio manager Stephen Notidis.

“The credit-risk environment is favourable,” notes Gambino. “There is good compensation for the environment we’re in, and valuations are reasonable. High-yield bonds tend to perform well in a rising-rate environment.”

Yet, he acknowledges that high-yield bond returns will moderate in 2014, although he believes that the category will outperform other fixed-income, such as government bonds. This is mainly due, he says, to a generally higher coupon and less interest-rate sensitivity.

However, the spectre of rising interest rates is on the horizon, Gambino adds: “I’m not sure if it will be in 2014 or 2015. But there is no escaping it unless we move into a deflationary or recessionary environment, in which rates have to stay low. Our base case is that rates will stay low or move higher.”

Gambino is somewhat cautious, as about 5% of the RBC fund’s AUM is in cash. The fund’s duration is also low, at three years. About 55% of AUM is in BB-rated bonds, followed by 18% in B-rated bonds, 11% in unrated issues, 2% in CCC-rated bonds and 9% in investment-grade issues.

“We’re keeping some cash because rates will move higher and there are limited opportunities, so we’re being careful about how we spend the cash,” Gambino says. “But our goal is to reduce that cash. We are also favouring more credit risk. If we start spending the cash, it will go more toward the single-B allocation.”

A bottom-up investor, the RBC fund holds bonds from about 85 issuers spread among 116 holdings. One top position is Sprint Nextel Inc., a BB-rated bond maturing in 2018 with a coupon yield of 7.5%. Says Gambino: “[Sprint Nextel is] one of the largest wireless firms in the U.S. and has done a good job in improving its operating performance.”

© 2014 Investment Executive. All rights reserved.