Emerging markets have been under pressure this autumn as concerns mount about a “quadruple whammy” of weak commodity prices, the strong U.S. dollar, the inevitability of rising interest rates in the U.S. and, most of all, China’s slowing economic growth.

Although some portfolio managers say the worries are very real, others argue that some areas in the emerging markets offer considerable upside.

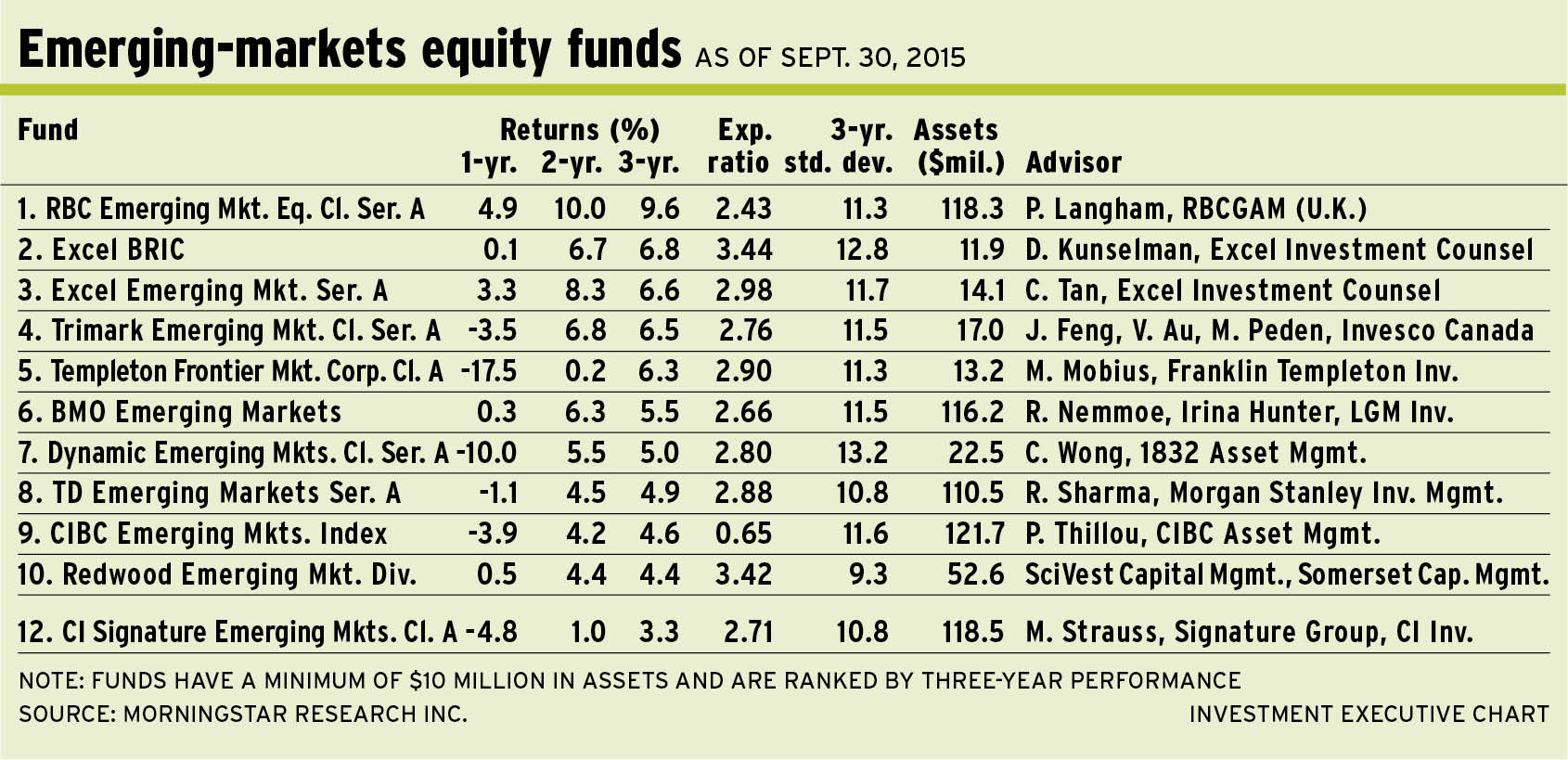

One of those in the first camp is Matthew Strauss, vice president in the Signature Group, a unit of Toronto-based CI Investments Inc., and manager of CI Signature Emerging Markets Class Fund: “We have moved toward real concerns about the growth of many emerging markets, which tends to be more of a fundamental issue.”

Economic growth is continuing to slow globally, and this is evident in recessions in Brazil and Russia. “Only a few countries have expectations that are more or less stable. Most countries, especially the commodity producers, have come under severe pressure,” says Strauss, who also cites slowdowns in Malaysia and South Africa.

The situation is only exacerbated by the end of so-called “easy money” – at least, as far as the U.S. is concerned. “There was a lot of cheap cash available – and a lot of it found its way into the emerging markets, both equities and bonds,” says Strauss. “If we are getting into a new liquidity regime, then some adjustments will be needed. That structural adjustment is playing into the negativity about the [emerging markets equities] asset class.”

Yet, it’s not all doom and gloom, says Strauss: “With all its challenges, is the asset class investible? I’d say yes. There are still some very good companies even in this environment. And some countries have embarked on reforms or are in the process of making important structural changes to create a platform for good growth for the next five years.”

About 15% of the CI fund’s assets under management (AUM) is in cash. Strauss says he is cautious and is looking for better buying opportunities. From a geographical standpoint, about 55% of AUM is in Asia (including 30% in China and Hong Kong) 13% is in Latin America, 5% is in South Africa. There also is 12% in U.S-listed resources firms.

One favourite holding in the 80-name fund CI is Tencent Holdings Ltd., a Hong Kong-listed dominant player in China focusing on social media and instant messaging. “Like a lot of Chinese companies under pressure,” Strauss says, “if we can get past this period of uncertainty, [Tencent] will do well.”

Tencent stock is trading at about HK$142.50 ($22.45) a share, or 38 times trailing earnings. There is no stated target.

A more upbeat view comes from Philippe Langham, head of emerging markets equities with London-based RBC Global Asset Management (U.K.) Ltd. and portfolio manager of RBC Emerging Markets Equity Fund. Although there is no denying that the sector has been under pressure, he argues, the impact of the downturn in commodities is overstated.

“What we are seeing now is that the impact is significantly less than it has been historically,” says Langham, adding that the commodity weighting in the MSCI emerging markets index is almost 50% lower than it was five years ago. In the future, he adds, “There will be more of a focus on domestic sectors such consumption.”

Langham views China’s slowing economic growth as a necessary part of that country’s reform process. “There is a rebalancing away from an investment-driven economy to one that is consumption-led,” he says. “I expect slower Chinese growth to be an ongoing feature, but not one that should scare investors.” He adds that some industries in China will remain under pressure.

In a similar vein, Langham says, investors should not be too worried about periods of subpar growth because they often lead to economic reforms. “Over the coming months, this [tendency] looks set to be an important feature in India, Malaysia, Mexico and China,” he says. “These reforms address issues such as fiscal discipline, infrastructure and privatization. While [the reforms] may take time to have an impact, they will support medium-term growth.”

From a valuation perspective, Langham argues, emerging markets stocks are trading at a discount of 30% relative to developed markets. “Some discount is warranted to compensate for higher risk,” he says. “But I expect the current discount to narrow over time.” On an absolute price/book value basis, he adds, the asset class has been cheaper only 5% of the time in the past two decades.

The RBC fund is fully invested. Langham has allocated about 17% of its AUM to China, 14% to India, 10% to South Korea and 9.9% to Taiwan, plus smaller amounts to countries such South Africa. Financials represent the top sector at 26%, followed by information technology (19%), consumer discretionary (15%) and consumer staples (14%).

One top name in the RBC fund is Mr. Price Group Ltd., a leading South Africa-based fashion and household-goods retailer. “It has consistently gained market, generated high returns on capital and is very cash-generative,” says Langham.

Mr. Price stock, which pays a 2.8% dividend, is trading at about ZAR 20,800 ($1,853.30) a share, or 19 times earnings. There is no stated target.

Equally bullish is Rasmus Nemmoe, lead portfolio manager, global emerging markets, with London, U.K.-based LGM Investments Ltd. and lead portfolio manager of BMO Emerging Markets Fund. He shares portfolio-management duties with Irina Hunter, portfolio manager at LGM.

Nemmoe notes that although some countries certainly are feeling the pinch, others are not affected as much. “Clearly, there are some countries highly exposed to issues such as weak commodity prices,” he says, citing Brazil and Russia as examples. “But there also are countries in which the risk is fairly contained. So, it’s important to take a more selective approach.”

Countries such as India are not only beneficiaries of the commodity downturn, they also are slowly being transformed.

India’s strength is thanks to a new government headed by Narendra Modi and by Raghuram Rajan, governor of the Reserve Bank of India, “who is steering financial markets in a very credible way,” says Nemmoe. “India, like the rest of the world, is not growing as fast as it did in the past. But [its growth] is still at decent levels.”

Turning to emerging markets equities, Nemmoe says, there has been indiscriminate selling. “Good and bad companies have been sold off together,”Nemmoe says. “But there are structural opportunities within the asset class.”

He points to India once again as an example of a promising market: “If you have a long-term approach and provided you can be more active within the asset class and sidestep the default exposure you get with a passive index, now is a good time to invest. I remain fairly optimistic.”

The BMO fund is fully invested. Nemmoe admits to being biased toward less developed markets in Southeast Asia that are benefiting from secular tailwinds. Consequently, about 29% of the BMO fund’s AUM is invested in India, 12% is in Indonesia, 9% is in the Philippines, and only 5% is in China and Hong Kong (regarded as a single market).

“We’ve always had a sizable exposure to India because that’s where some of the best bottom-up investment opportunities are within emerging markets,” Nemmoe says. “There are companies that can generate high returns in a high-growth environment. That translates into strong, free cash-flow growth and returns.”

Running a fund with 50 holdings, Nemmoe likes ITC Ltd., a diversified India-based firm with interests in tobacco, food, paper and hotels. ITC’s so-called “fast-moving consumer goods” segment caught Nemmoe’s attention as he believes ITC is leveraging its tobacco distribution network to ramp up the food distribution business, which will generate strong cash flows.

ITC stock is trading at about INR 340 ($6.30) a share, or roughly 20 times forward earnings. There is no stated target.

© 2015 Investment Executive. All rights reserved.