Although Canadian equities markets surprised on the upside in 2014, they lagged their U.S. counterparts by a small margin because Canada’s resources stocks have yet to recover from the autumn correction. Portfolio managers of Canadian-focused equity funds, which have non-Canadian equities exposure to varying degrees, are optimistic and argue that there are still opportunities despite generally fair valuations.

“It’s slightly different, north and south of the border. Overall, the quality of growth is improving, especially in the U.S. – and there are a few reasons for that,” says Brandon Snow, principal and co-chief investment officer at Toronto-based Cambridge Global Asset Management, a unit of CI Investments Inc., and portfolio manager of CI Cambridge Canadian Equity Corporate Class Fund.

“First, U.S. government spending continues to be weak relative to the real economy,” he says. “Second, there is a tailwind in the drop in the oil price. While the growth of oil is good for some parts of the economy, the impact of the falling oil price is more important for consumer confidence.”

Meanwhile, Snow adds, the U.S. housing market has stabilized: “With the oil price down, good job growth and mortgage availability easing, all these things combine to give you a pretty buoyant consumer market in the U.S.”

But, Snow believes, economic growth in Canada will lag that in the U.S.: “The growth drivers here are at the opposite end of the spectrum. The money spent on residential construction is still quite high. But the decline in the commodity space brings less capital into the country and could cause a slowdown. Overall, Canadian consumer debt levels are pretty high. A lot of these underlying drivers are already in place, and it’s hard to see them getting better.”

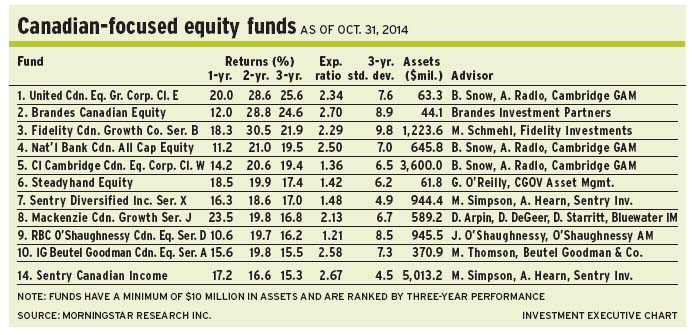

Snow is a bottom-up investor. About 13% of the Cambridge fund’s assets under management (AUM) is in cash, which is a byproduct of the stock-picking process.

From a sector standpoint, about 30% of AUM is in consumer staples and discretionary stocks, 15% is in energy, 15% is in financials and 12% is in industrials. There are smaller allocations in sectors such as technology.

Roughly 44% of the Cambridge fund’s AUM is in Canadian stocks, 35% is in U.S. stocks (with no currency hedge) and 8% is in Europe and Latin America stocks (hedged back into the Canadian dollar [C$]).

Running a fund with 40 names, Snow lately added Adecco SA, a French temporary staff placement firm that has global operations. “We like the management team. [Adecco] introduced a more flexible business model after the 2008-09 financial shock,” Snow says. “[The firm] can withstand economic headwinds if they do happen.”

Listed in Switzerland, Adecco stock is trading at about 67.65 CHF ($65.40), or 15.5 times trailing earnings, and pays a 3% dividend. Snow has no stated target.

The economic fundamentals are strong in North America, agrees Michael Simpson, senior vice president at Toronto-based Sentry Investments Inc., and lead portfolio manager of Sentry Canadian Income Fund. He shares portfolio-management duties with Aubrey Hearn, vice president of Sentry.

Simpson points to the rebounding U.S. economy, which is gaining traction from lower energy prices: “The average gasoline price is US$2.94 a gallon, which is a huge benefit to consumers. Over a year ago, it was US$3.64. When consumers can save, that’s like a reverse tax. Traditionally, people tend to spend more when that happens.”

Overall, Simpson is optimistic about the U.S., which has seen unemployment fall to less than 6%, but neutral on Canada. He has concerns about Canada’s energy sector, which is bound to be affected by lower commodity prices, but is upbeat on Canada’s manufacturing sector, which benefits from the weak C$ and the stronger U.S. economy.

“Companies that invested in equipment when [the C$] was high, are now benefiting from a 13% decline in the dollar,” says Simpson, who foresees 2%-2.5% economic growth in Canada in 2015, vs more than 3% in the U.S.

Simpson admits that a looming hike in interest rates in the U.S., which might occur in mid-2015, is a concern. However, he adds, the benchmark rate is not likely to go as high as in previous economic cycles.

From a geographical viewpoint, about 63% of the Sentry fund’s AUM is allocated to Canadian stocks and 36% to U.S. stocks (which are partially hedged back to the C$). Simpson has been increasing the U.S. exposure because of better growth prospects and wider diversification there than at home.

From a sector standpoint, 25.9% of the Sentry fund’s AUM is in industrials, 19.4% is in energy and 14% is in a blend of consumer staples and discretionary. There are smaller allocations in sectors such as health care and 6% in cash.

Simpson is a value-oriented investor; the Sentry fund has about 52 names. One top holding is Catamaran Corp., a Canadian information-technology (IT) firm that administers drug plans for a variety of corporate clients. “The bigger players [in the drug plan administration business] target the larger companies, while Catamaran serves the mid- and small niche,” Simpson says. “It’s growing its business.”

Catamaran stock is trading at $56.50 a share, or 18 times 2015 earnings. Simpson has a 12- to 18-month target of $62 a share.

Equally optimistic is David Arpin, portfolio manager at Toronto-based Bluewater Investment Management Inc. and co-manager of Mackenzie Canadian Growth Fund. He shares portfolio-management duties with Dennis Starritt and Dina DeGeer, both principals of Bluewater.

“Economic fundamentals seem relatively sound in North America,” Arpin says. “The big pieces are employment growth in the U.S., which has been reasonably strong, and the housing sector, [which] has started to improve over the past few years.”

The U.S. economy has suffered, however, from declining public-sector spending.

“That headwind is seemingly almost over and should be a tailwind for U.S. growth,” says Arpin. “There is a similar story on the Canadian side, where we are projected to run a surplus this year. Lots of things have turned around in the past few years. There isn’t strong growth; just a moderate, slow improvement.”

Arpin expects an interest rate hike, but is reluctant to forecast its timing: “The Federal Reserve [Board] has tied its rate hike to inflation, which is running below its target, and slack in the labour force. The latter is more difficult [to pin down]. It’s an area that the Fed is trying to understand more clearly. It has communicated that either factor will lead to an interest rate hike, but I don’t know when that will happen.”

As for valuations, Arpin notes, many sectors have rebounded from the September correction, but Canadian resources stocks still are well off their highs: “Valuations have changed in the energy and materials, and that’s where we are focused. A lot of other things bounced back really quickly.”

From a geographical viewpoint, 58% of the Mackenzie fund’s AUM is held in Canadian stocks, and 38% is in U.S. stocks (which are not hedged back to the C$), plus about 4% in cash.

From a sector viewpoint, there is 22.7% in IT, 22% in consumer cyclical, 14% in industrials, 10% in financials and smaller weightings in other sectors, such as 5.2% in energy.

Arpin is a bottom-up investor. One favourite holding among the Mackenzie fund’s approximately 31 holdings is Stella-Jones Inc., which manufactures railway ties and utility poles. In the former business, Stella-Jones offers a start-to-finish service for railways and also benefits from a duopoly.

“That [duopoly]comes with higher margins and higher total revenue for the firm,” says Arpin, noting that the railway division is enjoying 20% annual growth. The utility pole business, he adds, is growing at a similar rate.

Stella-Jones stock is trading at about $35.10 a share, or 18 times 2015 earnings. Arpin has no stated target.

© 2015 Investment Executive. All rights reserved.