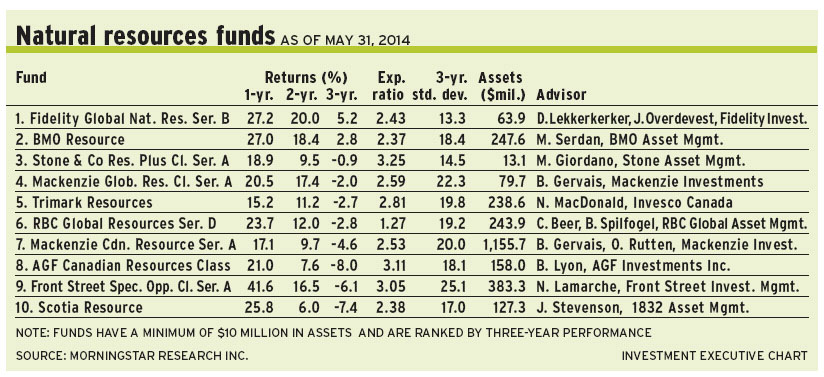

Natural resources stocks have shown resilience lately, demonstrating that the secular bull market is still alive and kicking. Fund portfolio managers maintain that overall conditions are positive, although they stress that stock-picking will be the key to fund performance.

“What we’ve seen in the last 12 months has been an energy-led recovery, but it’s not the entire story. There have been winners and losers,” says Bob Lyon, senior vice president with Toronto-based AGF Management Ltd., and portfolio manager of AGF Global Resources Class Fund. “While it’s too early to write the epitaph of the secular resource bull market, what we have entered is a pause in the secular story caused by slowing global demand from emerging market economies.”

Lyon points to China’s economy, which has slowed to about 7% annual growth in gross domestic product (GDP) from 10%. “That is still growth,” he says, “although not the level that investors had become accustomed to. But the commodities and stocks that have done the best are those that are least tied to the China story – and that’s the energy sector.”

Energy stocks have gained strength because demand for natural gas has been boosted by an improving North American economy, sending prices from $2 per million cubic feet (mcf) to $4/mcf.

“[The price of natural gas] is not tied in any material fashion to the world economy,” Lyon says. “Natural gas did have its own bear market from 2008 to 2013, but it was supply-driven with a lot of new gas coming to market thanks to unconventional drilling. Now, it’s a more balanced situation. We’ve just normalized the price from an oversold position.”

But, thanks to growing global demand, oil prices have surged in the past year to about US$104 a barrel for West Texas intermediate grade from US$91/barrel. This effectively has narrowed the differential (discount) relative to the Brent oil prices (set in London) to a few dollars.

“We’ve seen the tightening of the discount,” says Lyon, “as bottlenecks at Cushing, Okla., [a transportation hub for crude] have become alleviated and companies were able to get some of their oil exported. But it took a while to narrow that discount.”

Lyon argues that it’s critical to separate the strong players in the energy industry from the weak ones: “This is not the kind of market we had from 2003 to 2008, when global growth pulled commodity prices higher. But that doesn’t mean a lot of commodities don’t look fantastic. You just have to be a little more selective.”

Lyon favours the energy industry. Almost 70% of the AGF fund’s assets under management (AUM) is in that sector, and virtually all the rest is in mining and materials producers. Lyon, an investor who looks for mispriced stocks and growth stories, manages a 70-name portfolio.

One favourite is Tourmaline Oil Corp., which produces about 110,000 barrels of oil equivalent (BOE) a day, primarily natural gas. Thanks to horizontal drilling, this level of production is projected to grow to about 145,000 BOE a day.

“[Tourmaline has] a top management team,” says Lyon, “and one of the highest growth rates in Canada.” Tourmaline stock is trading at about $53.40 a share, or roughly 8.5 times enterprise value (EV) to earnings before interest, taxes, depreciation and amortization (EBITDA). Lyon has a target of $65-$75 a share within 18 months.

Sentiment grew too bearish a couple of years ago and sent investors to the exits, argues Darren Lekkerkerker, a fund portfolio manager with Toronto-based Fidelity Investments Canada ULC and portfolio co-manager of Fidelity Global Natural Resources Fund.

“At the low in 2013, no one wanted to say they owned natural resources stocks,” he says. “It became popular to say, ‘China is crashing.’ But the fundamentals haven’t really changed. Sentiment just went from very negative to less negative.”

During the 2003-2011 secular bull market, spending on mines and exploration increased as commodity prices also rose higher, says Joe Overdevest, co-manager and portfolio manager. “Currently, fewer mines are being built and spending on oil exploration is lower, as commodity prices are low.”

Spending on mines or major projects often occurs when prices are high because companies have the money to spend, Overdevest adds. “Mines take time to come into production, often several years. But as supply comes on, prices go lower, pushing down spending on future supply. This is the nature of the cycle.”

There is no denying, however, that rising living standards in the emerging markets are a powerful secular trend and one that will not easily diminish, says Overdevest. “But the slowdown in China’s [annual] GDP [growth] from 10% to 7% can be very negative for valuations.” Meanwhile, Overdevest notes that the mid-term outlook for oil and gas is “balanced”, as many new oil and gas wells are being exploited in North America, putting pressure on prices.

On the materials side, Lekkerkerker says, demand for base metals such as copper remains relatively strong, even though China’s appetite has diminished.

“Once you move enough people into the cities,” he says, “growth becomes harder to sustain. But the absolute amount of copper that China uses is still growing.” However, he anticipates that copper will be in a modest surplus situation in 2015, which could be negative for commodity prices.

Lekkerkerker and Overdevest have about 56% of the Fidelity fund’s AUM in energy firms and 40% in materials, split among chemicals (18%), containers and packaging (7.5%), and paper and forest products (6%), with smaller holdings in precious metals and technology. There also is about 4% in cash.

One top holding in the 47-name Fidelity fund is CCL Industries Inc., a Canadian packaging firm that acquired the office products division of Avery Dennison Corp. last year for a relatively low price of US$500 million, or about five times cash flow.

“[The deal] was very accretive to earnings per share,” says Lekkerkerker, adding that the firm has benefited from cost efficiencies. CCL stock is trading at about $105 a share, or 16 times 2015 earnings. Lekkerkerker expects the business to grow by about 3% a year, but has no stated target.

The secular theme is still intact, argues Chris Beer, vice president of Toronto-based RBC Global Asset Management Inc. (RBCGAM), and lead portfolio manager of RBC Global Resources Fund, who shares portfolio-management duties with Brahm Spilfogel, RBCGAM vice president.

“A couple of years ago, China was a US$7-trillion economy growing at 10%,” Beer says. “Now, it’s a US$9-trillion economy growing at 7% a year, which is much faster than the global economy. [And] we’re seeing Europe start to mend itself, and it is where the U.S. was a couple of years ago. The U.S. is also growing fairly strongly. There has been a bit of a decoupling, where developed countries are doing better than some emerging countries.”

Beer, like his peers, acknowledges that investors have shunned resources firms because of concerns about China’s decelerating trend. But poor management of capital, which resources companies are working to address, was another overriding worry.

“We’re starting to see companies grow production within cash flow, which is a first for many resource companies,” says Beer. “I’m not saying we’re off to the races. But many of these companies are trading at six times EV to EBITDA, vs nine to 9.5 times for the broader market. Obviously, these are cyclical firms, so you have to account for that. But if their bottom line is starting to improve, there are signs on the horizon that returns are growing.”

Beer generally keeps AUM of the RBC fund within a 60%/40% balance of energy to materials. And from a market-cap perspective, he also has a modest bias to small- and mid-cap names, which have more growth potential. Still, there is a fair weighting of large-cap names such as Suncor Energy Inc.

One favourite in the 80-name RBC fund’s portfolio is EOG Resources Inc., an oil firm that produces about 600,000 BOE a day and is one of the pioneers of horizontal drilling in Texas’ Eagleford and Permian plays.

“[EOG’s] EBITDA is growing at 15%, which is quite attractive for that size of company,” says Beer. “We’re also starting to see 13%-15% returns on invested capital.”

EOG stock is trading at about US$105.75 ($114.75) a share, or six times EV to EBITDA. Beer has a target of US$120-US$125 within 12 months.

© 2014 Investment Executive. All rights reserved.