It was a challeging time in 2014 for natural resources stocks. Commodity prices tumbled dramatically in the latter half of the year, primarily because of oversupply concerns. But since the start of 2015, the oil price in particular has shown resilience, gradually climbing to the US$60 a barrel level. Other commodity prices are flat or rising very slowly.

Although some fund portfolio managers are expressing optimism about oil, others are more cautious.

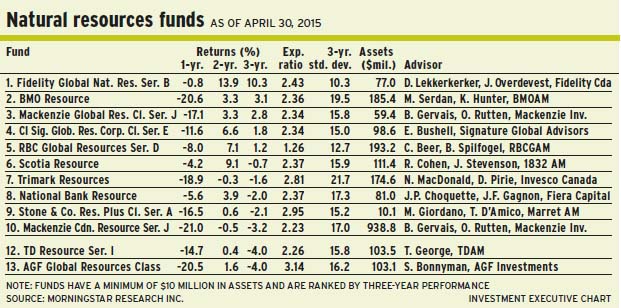

One of those in the cautious camp is Joe Overdevest, portfolio manager with Toronto-based Fidelity Investments Canada ULC and co-manager of Fidelity Global Natural Resources Fund.

“What changed for oil was OPEC [Organization of Petroleum Exporting Countries]. For the longest time, it was a ‘swing’ producer,” says Overdevest, referring to how OPEC would cut production when there was a global oversupply, then ramp up when supply fell short.

Last autumn was a turning point, says Overdevest, when OPEC declared it would no longer be a swing producer, even though U.S. production kept rising.

“[The price of] oil fell drastically – and rightfully so. But the commodity price overshoots, on the upside and downside, versus the fundamentals,” says Overdevest, who shares portfolio-management duties with Darren Lekkerkerker, portfolio manager at Fidelity.

“Has something fundamentally changed, just because oil has gone from US$45 to US$60 a barrel?” Overdevest asks rhetorically. “No. U.S. and Canadian producers have cut back capital spending. That’s positive. But the impact on the fundamentals is not felt until six months later. The oil price has already rebounded – partly because the price fell too much and, second, the price is anticipating production cuts. And those cuts are coming.”

Overdevest is reluctant to make a call on the oil price: “I’m cautious. Yes, [the price] can move up from here, because we have seen a lot of production cuts. But the big driver is supply and demand. Demand is OK, not robust, but global gross domestic product [GDP] growth is OK. The supply side is the bigger question.”

OPEC, which is scheduled to meet in June, may decide to cut production, although that is not certain. Meanwhile, some U.S. shale-oil producers have said they will resume drilling when oil hits US$65 a barrel.

“That’s a potential headwind for oil,” says Overdevest. “At US$65, there will be more supply, [which] may limit how high the oil price can go. Fundamentally, [comments by shale-oil firms] are negative for the oil price.”

About 59% of the Fidelity fund’s assets under management (AUM) is in oil and gas stocks (including service companies), 41% is in materials (which includes 7% in paper and forest products and 12% in packaging companies). From a geographical perspective, about 45% of the Fidelity fund’s AUM is in Canada, 44% is in the U.S., and 11% is in Europe.

One longtime favourite in the 47-name portfolio is Stella-Jones Inc., a provider of pressure-treated railway ties and utility poles. “[The firm] is a leader in an oligopolistic industry, and we think it will continue to compound its earnings growth,” says Lekkerkerker.

Stella-Jones stock is trading at about $46.80 a share, or at about 22 times forward earnings. There is no stated target.

a more optimistic view on oil is expressed by Thomas George, vice president at Toronto-based TD Asset Management Inc., and portfolio manager of TD Resource Fund. He believes that the commodity story is splitting into two tiers.

“One tier is solely focused on oil. The second tier is a mix of base and bulk commodities,” he says. “What differentiates them is that the supply/demand dynamics for oil are very attractive right now. But to make this dynamic work, you need to see action from both sides. We’re seeing that. To me, that’s bullish.”

The huge drop in the oil price, George adds, was driven by an oversupply relative to demand. “We needed to see supply come off, and we have seen that in the U.S.,” says George, adding that the U.S. Energy Information Agency has reported that the number of producing oil rigs has declined by 57% since the peak in mid-2014. “We need to see that one critical piece of the global supply puzzle is not growing anymore. That will stabilize the price at where we believe oil should be, long term.”

George, basing his opinion on strong global demand for gasoline and improving oil supply fundamentals, adds: “The new normal is anywhere from US$75 to US$90 a barrel. The first rung, US$75, is reachable by yearend.”

As for resources such as copper and iron ore, George says, the supply/demand dynamics are not quite as favourable.

“Copper is in a slightly different category than oil. But on a medium- to long-term view, there are attractive dynamics. It’s been very hard to replace the supply that we’re using,” says George, who regards the price of the base metal, US$2.90 a pound, as fair. “Copper is a consumption story, and it’s moving in line with – if not better than – global GDP growth.”

About 64% of the TD fund’s AUM is in energy, 32.5% is in materials, and there are small holdings in sectors such as utilities. On a geographical basis, Canadian stocks account for 73% of the fund’s AUM, while the U.S. accounts for 24%.

One favourite name is Netherlands-incorporated LyondellBasell Industries NV, a global producer of ethylene for plastics. “[Its] focus is on operational excellence,” says George. “[The firm] has a top-tier return on invested capital. And more than that, [company management] says what they will do.”

LyondellBasell, which has returned US$17.2 billion to shareholders since 2011 in the form of share buybacks and dividends, has just raised its dividend by 11% and initiated another 10% share buyback program.

New York-listed LyondellBasell stock is trading at about US$100.70 ($120.60) a share and pays a 3.1% dividend. George has a 12-month target of US$114.

THE REBOUND IN CRUDE OIL prices is correlated to the gradual weakening of the U.S. dollar (US$), argues Stephen Bonnyman, portfolio manager with Toronto-based AGF Investments Inc.; he oversees AGF Global Resources Class Fund.

“What we have watched taking place in this market has been driven predominantly by macro events – in particular, strength [in the US$]. A rising U.S. dollar has a negative impact on dollar-denominated commodity prices. But now, the reverse is happening. The U.S. dollar is weakening on a trade-weighted basis, which is triggering a response in all the commodities.”

This pattern may prevail for a while, he adds: “At this point, the U.S. is one of the stronger global economies. But we are starting to see the latent signs of an improving outlook, especially in Europe and China.”

Bonnyman notes that the rising component of shale oil in the U.S. has become a game-changer: “It’s important because it has a very high decline rate, which means production from Year 1 to Year 2, and so on, will fall. To maintain production, there is constant reinvestment.”

But because drilling has become uneconomical at current oil price levels, activity has been slashed in the U.S. Yet, lower production will only result in higher prices. “The market is underestimating the production response that is taking place,” says Bonnyman, who expects that oil could be US$65-US$70 a barrel within a year.

Bonnyman, who believes resources stocks are cheap relative to the market, has allocated about 52% of the AGF fund’s AUM to energy, 41% to materials and smaller amounts to industries such as fertilizers. On a regional basis, North America represents 85% of the fund’s AUM, while Europe accounts for 15%. The fund has about 60 holdings.

Bonnyman likes Lundin Mining Corp., a producer of copper, zinc and nickel with operations in Spain, Portugal and Sweden.

“[Lundin] has a solid, stable management team. We like [the firm’s] earnings leverage to rising commodity prices and look favourably on each of these three metals over the next 18 to 24 months,” says Bonnyman. Yet, he argues, the market has not acknowledged a recent Chilean copper acquisition that will boost earnings materially.

Lundin stock is trading at about $5.70 a share; however, based on rising earnings, Bonnyman’s target is $7.50 within about a year.

© 2015 Investment Executive. All rights reserved.