After a robust 2013, in which U.S. stocks went up by 32.3%, stock markets have been eking out modest gains lately. Yet, fund portfolio managers are generally upbeat about 2014 despite the risks on the horizon in the form of rising interest rates and geopolitical tensions in Ukraine and the Middle East.

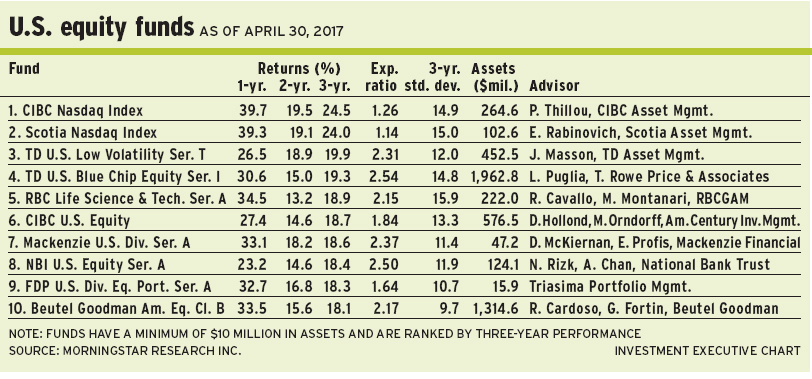

Larry Puglia, vice president with Baltimore-based T. Rowe Price Associates Inc., and portfolio manager of TD U.S. Blue Chip Equity Fund, argues that after an excellent year, the U.S. equities market has lately been characterized by a shift away from growth stocks.

“Overall, the market was doing fairly well until early March, when we had a couple of events that precipitated a rotation away from momentum stocks,” says Puglia. “But we are coming off a year in which the market did very well. Throw in any sort of concern, such as unrest in Ukraine, and it’s not surprising that there’s been a slowing in stock gains and some significant declines in certain stocks.”

Investors are not questioning the U.S. economy’s progress, adds Puglia: “We are still experiencing a recovery. But there’s been a rotation in the market. A number of consumer staples stocks have done well, as have airlines and energy names. There has been a correction affecting some growth stocks with higher valuations. But you can still find enough stocks that are attractive on a risk/reward basis to warrant being fully invested. Across the board, valuations are reasonable.”

Puglia notes that markets have moved upward in the past 18 months despite slow job growth and weak wage growth. And, on balance, he remains cautiously optimistic: “We’ve had periods in the past that were slow, steady recoveries that did not overheat and triggered a substantial increase in rates. We’ve seen it many times, when the market climbs a ‘wall of worry’ and is not precluded from doing well in an economic environment that is tepid and slowly growing.”

Puglia is a bottom-up growth manager; he keeps the TD fund fully invested. About 26% of the TD fund’s assets under management (AUM) is in consumer discretionary stocks (vs 12% in the S&P 500 composite index), 22% is in information technology (IT; 18%)), 17% is in health care (13.3%), 8% is in financials (16.4%) and smaller weightings are in sectors such as telecommunications services.

Running a portfolio with 140 names, Puglia likes global biotech companies such as Biogen Idec Inc., which develops therapies for chronic diseases such as multiple sclerosis.

“We like that area,” says Puglia, “because a person is often diagnosed in his or her 40s and can be treated with some success with these drugs, but will need treatment for several decades.

“Over the next three years,” adds Puglia, “earnings should grow [by] around 25% a year. The market is not growing at that rate.”

Biogen stock is trading at about US$276.50 ($305.30) a share, or about 35 times trailing earnings. There is no stated target.

Grayson Witcher, a fund portfolio manager with Calgary-based Mawer Investment Management Ltd. who oversees Mawer U.S. Equity Fund, believes that valuations in U.S. large-cap equities markets are fair to slightly expensive.

“If you look at the very long term, price/earnings multiples have averaged around 16.5 times,” says Witcher. “Compare it to where we are now, it’s around 17 to 18 times, and a little expensive. That gives us a sense of where we are going.” (He adds that small- and mid-cap stocks are trading at higher valuations of 23 to 25 times earnings.)

In spite of the higher than average multiples for large-caps, Witcher does not see any imminent risks that are greatly worrying: “It’s hard to predict the exact timing of an event. But you can get a sense of risk building. For now, [the U.S. Federal Reserve Board] policy is still pretty accommodative. It’s unlikely that higher rates will choke off the economy anytime soon. The economy is doing reasonably well, although unemployment is still high and consumer confidence is only OK.”

Yet, external factors, such as tension in the Middle East, have the potential to escalate – although Witcher does not expect them to get wildly out of control.

“The other issue is slower growth, especially in the U.S.,” says Witcher. “We had a decade of very high growth in the 1990s and rapid housing market expansion in the 2000s. We got used to it. But there have been periods in the past when gross domestic product growth was 1%-2% and 5%-6% annual equity returns were regarded as the norm. I am not saying that we are going back to that. But there is risk we might.”

Witcher is a bottom-up manager. The Mawer fund holds shares in about 53 companies, which generally fit into the mould of being so-called “wealth creators” – well-managed companies that trade at a discount to their intrinsic value.

From a sectoral standpoint, financials account for 20.3% of the Mawer fund’s AUM, followed by IT (17.3%), industrials (10.3%), consumer staples (10.3%), health care (10.1%) and smaller holder holdings in sectors such as energy and materials.

One favourite name in the industrials sector is United Technologies Corp. (UTC), a global conglomerate with interests in Otis Elevator Co., aerospace player Pratt & Whitney (a division of UTC) and Carrier Corp. (of heating and air conditioning products fame). In particular, Witcher likes the fact that both Otis and Pratt & Whitney have strong recurring revenue from maintenance contracts.

“Once you are ‘specked’ into a new aircraft, like the Boeing 787,” says Witcher, “it’s very hard to get replaced. These are very stable and predictable businesses. And the valuation is pretty reasonable.”

UTC stock is trading at about US$116.50 ($128.50) a share. There is no stated target.

Bottom-up stock-picker Ashley Misquitta, a fund portfolio manager with Toronto-based Invesco Canada Ltd., who co-manages Trimark U.S. Companies Fund with Invesco vice president Jim Young, agrees that valuations are higher than a couple of years ago and that diligence in required when stock-picking.

“Two or three years ago, stocks were trading at attractive valuations, or even below,” says Misquitta. “Now, we have to exercise more patience. Sometimes, we can jump in immediately; but, other times, we have to be a bit more selective. But as new money comes, it’s not hard to deploy that capital.”

Rather than dwell on short-term risks, Misquitta is concentrating on stocks that will benefit from long-term secular tailwinds.

“We are in the early stages of an energy boom,” he says. “The U.S. is sitting on vast reserves of oil and gas. [Americans] are getting better at extracting crude oil from the Bakken shale, for instance. There also are plays in the U.S. that remain unexploited.”

Another factor is the evolving U.S. manufacturing sector, which many people had written off due to the so-called “offshoring” of jobs.

“We are in the early stages in seeing a reversal of that,” says Misquitta, noting that rising productivity has offset rising labour costs. “There are more higher-value manufacturing jobs returning to the U.S. because the U.S. remains quite competitive on a unit cost basis.”

At the same time, he adds, low natural gas prices have been a boon to chemicals producers, refiners and steel industries: “Input costs are low, so companies are factoring that into their decisions on where to build new plants. This is helping the manufacturing sector.”

Although Misquitta is cognizant of the risks regarding China, and even Europe, he believes those won’t change the fact that the economic cycle remains in place. “We will have recessions and extrinsic events that scare markets,” he says. “But, as managers, we can’t predict them. As bottom-up fundamental investors, we’d rather pay attention to the businesses we own and their internal dynamics.”

There are about 48 names in the Invesco fund. About 28% of the fund’s AUM is in IT, followed by 15% in consumer discretionary firms, 14.4% in financials, 13.1% in health care, 12.5% in industrials, with smaller holdings in sectors such as energy.

One top holding is Johnson & Johnson Services Inc., a global diversified health-care products provider with market-leading interests in consumer products, medical devices, trauma products and pharmaceuticals.

“When it comes to consumer products, [Johnson & Johnson has] very robust brands, and tends to be somewhat recession-resistant,” says Misquitta. “On the medical devices side, around 70% of [the firm’s] business is No. 1 or No. 2 in market share. The barriers to entry are very high for new companies to supplant them.”

Misquitta adds that Johnson & Johnson’s cash flow has been consistent, even through the last recession: “That’s an attractive characteristic in a business.”

Johnson & Johnson stock is trading at about US$100 ($110) a share, or 19 times trailing earnings, and pays a 2.6% dividend. There is no stated target.

© 2014 Investment Executive. All rights reserved.