Energy stocks have rebounded in the past year, thanks to strong commodities prices, improvements in infrastructure and the continuing recovery in the North American economies. Based on current valuations, natural resources equity fund portfolio managers are confident about the prospects for 2014.

“We’ll have a good year for energy stocks, and also more volatility. But overall, it will be a positive year,” says Jennifer Stevenson, vice president with 1832 Asset Management LP in Calgary and portfolio manager of Dynamic Energy Income Fund. “That’s because the fundamental supply/demand [situation], particularly around oil, is tight.”

Stevenson notes that the oil industry has had a boost from two new major pipelines connecting a storage hub in Oklahoma to refineries on the U.S. Gulf Coast.

“We have more take-away capacity coming out of Canada,” she says, “so we’ve seen the Edmonton oil price tighten up and move closer to the West Texas intermediate [WTI] price.”

Canadian producers are benefiting from the narrowing of the price differentials between Canadian oil and offshore oil. For example, the heavy-oil differential has narrowed to $18 a barrel in the past year from $40, largely the result of expansion of BP PLC’s heavy-oil refinery in Indiana and greater pipeline and railway capacity to transport the commodity.

“The differential will always be around 20% of WTI because of the difference in quality. Heavy oil is not the same as light oil,” says Stevenson.”But 20% is still a great number. On top of that, we have a weak Canadian dollar [C$], which helps our producers. The product is priced in U.S. dollars, but our costs are in C$.”

Many companies in the energy sector, Stevenson adds, have streamlined operations, introduced cost controls and increased profitability.

“Companies can reinvest their free cash flow back into their businesses and give us growth,” she says. “We have stronger companies that operate in a better profitability environment.”

Meanwhile, although multiples have expanded for Canadian stocks, they remain cheaper than their U.S. counterparts.

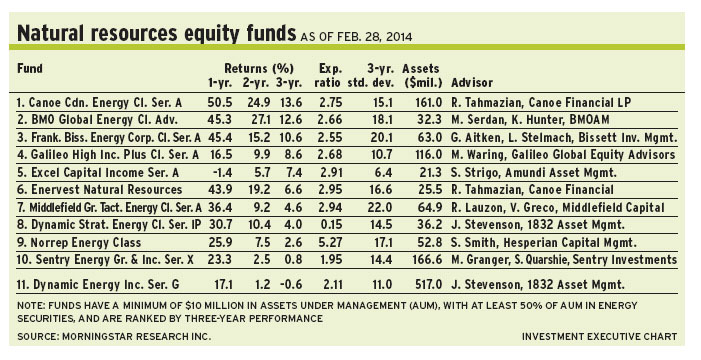

The Dynamic fund contains about 45 names. Roughly 62% of its assets under management (AUM) is in producers and services firms, 31% is in infrastructure and 7% is in cash. About 44% of the positions are in U.S.-based companies, 47% are in Canada and smaller portions are in markets such as the Netherlands.

Stevenson likes Enterprise Products Partners LP, a major U.S.-based firm that runs so-called “hubs” that handle natural gas liquids. Enterprise Products’ stock pays a 4.3% dividend and trades at 14 times enterprise value (EV) to earnings before interest, taxes, depreciation and amortization (EBITDA).

Enterprise Products’ shares are trading at US$65 ($69.50) each. Stevenson’s target is US$71 ($75.92) within 12 to 18 months.

Conditions have improved

Conditions have improved in the past six months, says Rafi Tahmazian, partner with Calgary-based Canoe Financial LP and portfolio manager of Canoe Canadian Energy Class Fund and EnerVest Natural Resources Fund.

“It’s due to the seasonal recovery,” says Tahmazian. “Back in the fall, everybody expected more demand for the winter heating season and that has come to fruition.

“The other factor,” he continues, “was that the sector was so out of favour for so long that valuations, relative to other sectors, looked compelling. That brought in new money, plus the money on the seasonal winter call.”

Into 2014, however, the sector continues to face challenges in the form of pipeline capacity constraints, while weaker players either have too much debt or lack the ability to exploit so-called “shale plays.”

“You need a lot of land and capital, and the typical company that will suffer is the junior firm,” Tahmazian says. “It’s becoming increasingly difficult to grow a junior oil and gas company out of that stage.”

This is attributable to the high cost of bringing production onstream, the need to find new wells to offset “decline rates” (the declining rate of production) and limitations on transporting the commodity that makes juniors dependent on larger players.

“It’s a difficult place to be,” says Tahmazian. “As a result, the money is going into the intermediate-sized companies.”

Regarding valuations, Tahmazian notes that the market is split between “haves,” whose valuations are high, and “have-nots,” whose prices are at 52-week lows. Yet, Tahmazian argues, this does not mean the “have” companies are overpriced; he believes they’re supported by strong fundamentals.

“Look at it this way: I water my flowers and pull my weeds. Most people tend to do the opposite,” Tahmazian says. “We are big believers in buying good companies that do well. And good companies mean three things: strong asset bases, strong balance sheets and strong management.”

Tahmazian is running portfolios with about 22 names in each of the Canoe and EnerVest funds. Except for three or four junior oil and gas names, the bulk of the AUM in these funds is in intermediate players.

One favourite is Raging River Exploration Inc., which is active in Saskatchewan and has grown from a junior player into an intermediate one.

Daily production has risen to 5,500 barrels of oil equivalent (BOE) in 2013 from 2,300 in 2012; Raging River expects to produce 9,500 BOE in 2014.

“[Raging River] has competent management with a good track record, is extremely well funded and benefits from a low cost of capital,” says Tahmazian, “which has allowed it to make strategic acquisitions throughout the year.”

Raging River stock is trading at about $7 a share, or about 7.5 times EV to EBITDA. There is no stated target.

Equally bullish is mason Granger, a fund portfolio manager with Toronto-based Sentry Investments Inc. and lead manager of Sentry Energy Growth & Income Fund. One main reason for Granger’s optimism is that energy stocks continue to discount an oil price that is considerably lower than the current WTI price of US$97 ($106) a barrel.

“Stocks are pricing in oil around US$70 a barrel, or almost a 30% discount to spot prices,” says Granger. “They are trading at a generational gap to the commodity.”

Granger notes that share prices for senior firms such as Suncor Energy Inc. have moved only modestly in five years. “It was trading at $26 in March 2009, when oil bottomed around US$30. Today, Suncor is $36 a share in a US$97-a-barrel environment,” says Granger, who shares portfolio-management duties with Swanzy Quarshie, a portfolio manager with Sentry.

“You have a company that has operating and financial leverage,” says Granger, “but for the stock to be $36 gives you a sense that it’s not reflecting what the commodity has done.”

To Granger, the discount says two things: “In 2009, when the price of oil fell to US$30, the stocks did not reflect the fact that was a sustainable level for oil prices. But coincidentally, on the other side, I don’t think that today stocks are getting full credit for oil [being] at US$97. Oil prices have tripled, but Suncor’s stock is up by only 38%.”

Granger notes that the market has split sharply between “haves” and “have-nots”: “There are a handful of companies in Calgary that can raise money whenever they want and investors will support them. But there are a whole bunch of companies that have to beg on their knees. It’s still not a healthy environment.”

Granger adds that financings for energy companies hit $12.2 billion in 2012. In 2013, financings fell to $7.3 billion, much of which occurred in the fourth quarter.

“Things started to look a lot better at the end of the year, in terms of investor appetite,” he says. “To me, it suggests we have come through a bottom and people are become more interested in energy stocks because they are so cheap.”

About 69% of the Sentry fund’s AUM is in exploration and production companies, 16% is in infrastructure and 15% is in services. Running a 32-name portfolio, Granger likes major firms such as Canadian Natural Resources Ltd. (CNR): “It is the go-to heavy oil name.

“We also believe,” he adds, “that improving operational performance at [CNR’s] Horizon oilsands project could drive investor confidence in the existing operations and expansion currently under construction.”

CNR shares, which pay a 2.1% dividend, are trading at about $38.15. There is no stated target.

© 2014 Investment Executive. All rights reserved.