Canadian equity balanced funds produced double-digit returns last year, thanks in part to improving equities markets, although fixed-income investments proved to be a challenge as long-terms yields spiked higher. But portfolio managers are bullish and are overweighting equities that appear to have better prospects than bonds.

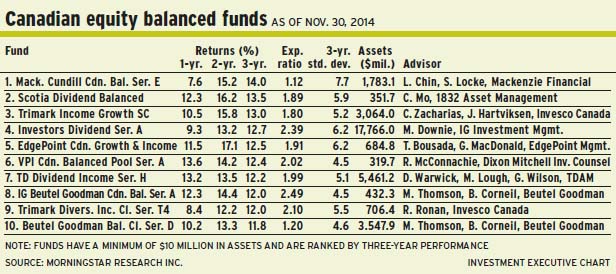

“I’m optimistic,” says Doug Warwick, managing director with Toronto-based TD Asset Management Inc. (TDAM), and lead manager of TD Dividend Income Fund. “The world has re-liquified since 2008. The banking system is in much better shape; leverage ratios are way down and capital ratios are way up. To me, the system is much safer.” (Warwick shares portfolio-management duties with Geoff Wilson and Michael Lough, managing director and vice president, respectively, with TDAM.)

Economic growth is modestly positive and inflationary risk is not a worry, says Warwick. “And there’s no significant risk of interest rates rising, in the next two or three years. They won’t run up to mid-single digits.”

As for valuations, Warwick notes that Canadian bank stocks, for example, are trading at around 11.5 times earnings and paying dividends of around 4%. “You can get a yield higher than fixed- income. I don’t see why these multiples can’t get bid up higher,” he says. “Even if we get a small expansion of the price/earnings multiple, as well as modest economic growth, I think that earnings could rise a little bit. But stocks could rise even more.”

From a strategic viewpoint, about 22% of the TD fund’s assets under management (AUM) are in fixed-income with the balance in equities, including about 3% in preferred shares.

The fixed-income portion of the TD fund is weighted heavily in corporate bonds, with 59% in investment-grade and 8% in high-yield bonds. There also is 19% in Government of Canada and 14% in provincial bonds. The average duration of the fixed-income portion is 6.3 years, vs. 6.7 years for the benchmark DEX universe bond index.

From an equities standpoint, Warwick favours Canadian stocks, largely because the TD fund complements other TD balanced funds that have wider ranges of geographical exposure. Warwick particularly likes financials, which account for 45% of this TD fund’s AUM, followed by energy (9%) and utilities (8%), with smaller weightings in sectors such as industrials.

“Stocks that we look for are less cyclical,” says Warwick. “We like high returns on equity, earnings and cash flow that grow over time, and distributions that grow over time. Financials, particularly the banks, fit that profile very well. Essentially, we’re trying to buy a book of income that will grow over time. If we can do that, then the net asset value should follow that.”

One top holding in the TD fund, which holds 45 equities names, is Royal Bank of Canada, the country’s leading bank. “In the latest quarter, it had a 20.3% return on equity,” says Warwick. “[It is] back on track for twice-a-year, modest increases in dividends. In the past 20 years, the dividend has risen to $2.38 a share from 29¢. That’s phenomenal.”

RBC stock, which pays a 3.8% dividend, is trading at about $69.20 a share. There’s no stated target.

Next: Les Stelmach, Bissett Investment Management

Les Stelmach, Bissett Investment Management

ALTHOUGH U.S. MARKETS were strong in 2013, your clients should appreciate that the performance of Canadian stocks was still “sneaky good,” says Les Stelmach, vice president with Calgary-based Bissett Investment Management, a division of Toronto-based Franklin Templeton Investments Corp., and portfolio co-manager of Franklin Bissett Dividend Income Fund. (Stelmach shares portfolio-management duties with Ryan Crowther, a Bissett vice president.)

“If you strip out the materials sector and the energy sector,” says Stelmach, “until recently, the Canadian equities market did a pretty good job in 2013. We don’t see a reason why it should not continue.”

Much of the market’s strength, Stelmach adds, was in the Canadian financial services sector, but industrials also fared well. Adds Stelmach: “Will we play catch-up to the U.S.? Yes, it’s possible. I’m not good at making broad forecasts. But I certainly would not rule it out.”

Stelmach notes that although economic challenges persist, central banks around the world are fostering economic growth by maintaining accommodative monetary policies. “The flip side,” he says, “is that the central banks believe they need to because there are still economic risks. Unfortunately, you can’t get all the positives, in terms of accommodative monetary policy, without the concerns that go along with it and [that] drive those policies. But I’m generally optimistic.”

Looking at the equities market, Stelmach also zeroes in on the financial services sector. Even if interest rates start to creep up, he notes, there’s the so-called “lag” effect – banks are slow to raise rates on savings accounts. “Their cost of funds won’t really go up as much,” he explains. “But the rate at which they lend money will go up much faster.”

Meanwhile, he adds, the banks have very profitable wealth-management businesses to help ride out interest rate hikes: “The outlook is still very positive. Maybe it’s true that interest rates can’t go lower. But they can certainly stay low for a period of time.”

From an asset-allocation perspective, Stelmach has about 61.7% of the Bissett fund’s AUM in Canadian stocks, 16.7% in U.S. stocks, 1.1% in international stocks and about 5% in cash. There’s also about 15.4% in bonds, with the bulk in corporate bonds. The average duration is 6.1 years, slightly below the benchmark.

Stelmach is a bottom-up portfolio manager who seeks companies trading below their intrinsic value. The Bissett fund holds about 40 Canadian and 18 U.S. stocks. Although Canadian banks dominate the top 10 holdings, Stelmach also likes some materials firms.

One new acquisition is Canexus Corp., a producer of chemicals used in the production of pulp. “[Canexus] stock has been weak of late because the market is waiting to hear about new contract announcements,” says Stelmach, adding that Canexus is looking to sign agreements with oil producers to ship oil via a low-cost storage terminal in Manitoba.

Canexus stock trades at about $6.36 a share and pays an 8.6% dividend. There’s no stated target.

Another favourite is Wajax Corp., a distributor of heavy equipment to the mining and energy industries. Says Stelmach: “There’s a slowdown in mining. But if we look longer term, this is a well-managed company and it generates good free cash flow throughout the business cycle.” The firm, he adds, is conservative in its use of working capital.

Wajax stock trades at about $36.85 a share and yields roughly 6.5%.

Glenn Paradis, imaxx Canadian Fixed Pay Fund

EQUALLY BULLISH IS GLENN Paradis, vice president, equities, with Toronto-based AEGON Capital Management Inc. and lead manager of imaxx Canadian Fixed Pay Fund. (Paradis works alongside Amelia Tsang, senior equities analyst at AEGON.)

“Our expectation is 2.25%-2.5% [economic] growth in 2014. We’re also expecting a pickup in the U.S., with growth of 2.5%-2.75%. Will Canada catch up? It will close the gap, but it won’t lead,” says Paradis, adding that Canada needs an export-led recovery to close the gross domestic product gap with the U.S.

Looking around the world, Paradis notes that Europe has turned the corner and finally is out of recession. And although Paradis is positive on China, he has concerns about the so-called “shadow banking” system that could be problematic for that country.

“It’s a risk in that economy,” says Paradis. “But we saw some social and economic reforms come out of the third plenary session that will be positive for China.”

Closer to home, Paradis anticipates that interest rates will come under pressure when the U.S. Federal Reserve Board finally begins tapering its bond-purchasing monetary stimulus (the so-called “quantitative easing” program) in either the spring or early summer. Paradis forecasts that 10-year bond yields will rise to 3%-3.25% by the end of the year.

“It won’t happen overnight and will be less of a shock than last summer,” he says. “And it won’t be high enough to disrupt the normal economic cycle.”

Paradis, who assumed management of the portfolio last summer from Stephen Carlin, has raised the imaxx fund’s equities exposure to about 83% of AUM (split between 70% Canadian stocks and 13% U.S.) from 73% at the start of 2013.

“We decided to get closer to our maximum in equities and reduce the bond exposure,” says Paradis, adding that 90% is the ceiling for equities in the fund. “Our view is that we will see a longer economic cycle and there will be non-inflationary growth. Rates have one way to go – and that’s somewhat higher. So, we restructured the fund to be more economically sensitive and less interest rate-sensitive.”

About 2% of the imaxx fund’s AUM is in cash; 15% is in fixed-income, mainly investment-grade corporate bonds. The average duration matches that of the benchmark.

Running a portfolio of about 100 holdings on the equities side, Paradis and Tsang like energy names such as AltaGas Ltd., which operates a utility and also produces gas.

“[AltaGas] has long-life assets that generate good cash flows, which meet our dividend requirements,” says Tsang, noting that the firm has a 4% yield. “[The firm] has a top-notch management team that has delivered very consistent earnings growth.”

With new projects coming onstream in 2014, the expectation is that AltaGas’s dividend will be increased. The stock trades at about $39.42 a share, or 12.6 times enterprise value to earnings before interest, taxes, depreciation and amortization. Tsang’s target price is $43 a share within 12 months.

© 2014 Investment Executive. All rights reserved.