Global fixed-income markets were challenging – to say the least – in 2013, thanks to worries about the intentions of the U.S. Federal Reserve Board and its long-awaited decision to reduce its bond-buying program. Looking into 2014, portfolio managers are cautious, realizing that economies are on the mend and that bond yields will inevitably rise.

“Our base-case scenario is for global growth to accelerate somewhat from 2013,” says Dagmara Fijalkowski, senior vice president and head of global fixed-income with Toronto-based RBC Global Asset Management Inc. and portfolio co-manager of RBC Global Bond Fund. “The U.S. will experience a cyclical recovery and the forecast is about 2.75% gross domestic product [GDP] growth. Japan similarly will see stronger growth, thanks to the massive stimulus. And Europe, because of the reduction in austerity measures and less fiscal drag, should see positive growth; [the forecast is] low at 0.7% – but for Europe, it’s a positive news scenario.”

Although deflation is a concern and could cause market jitters, Fijalkowski does not anticipate such a development. (See story on page 20.) Nor does she foresee excessive inflation. “Low inflation or non-inflationary growth is positive for corporations and not bad for bonds,” says Fijalkowski, who shares portfolio-management duties with Soo Boo Cheah, portfolio manager with London-based RBC Global Asset management (UK) Ltd.

Even with 10-year U.S. government bond yields at 2.9% and inflation about 1%, Fijalkowski believes yields are attractive: “If you think that nominal yields could rise to about 3.5% in 2014 and this disinflationary trend persists, then fixed-income investments will be of more interest to investors.”

There is a high probability that the benchmark 10-year U.S. government bond yield will reach 3.5%, argues Cheah: “But having said this, we do not completely dismiss an environment in which the 10-year yield may go below 3% if the growth picture does not materialize. Our message is that we may have a forecast, but our investment process does not rely on one forecast. Rather, we develop a range of economic scenarios, evaluate the upside and downside, and assign risks accordingly to all the scenarios.”

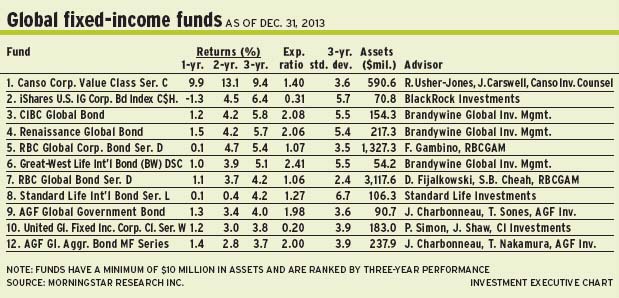

From a strategic viewpoint, Fijalkowski and Cheah are somewhat defensive. The RBC fund portfolio’s average duration is six years, slightly below the benchmark Citigroup world government bond index (hedged into Canadian dollars [C$] ). But what matters to these active portfolio managers is their decision to shorten duration within certain regions – particularly Japan.

In brief, much of the weighting in Japan has been shifted into U.S. and European markets, in which the risk/reward profile is more attractive. The portfolio managers use credit and other yield curve strategies to generate a running yield of 2.8%, which is higher than the benchmark’s 2.4%.

From a regional perspective, Europe accounts for 44% of the RBC fund’s assets under management (AUM) vs 40% for the benchmark. There’s also 38% in the U.S. and Canada combined vs 30% in the benchmark; and 17% in Japan vs 26% in the benchmark. More than 350 holdings comprise the fund, the bulk of which is in sovereign debt.

From a currency standpoint, 92% of the RBC fund is hedged back into C$.

Princing in tapering

The bond market has priced in most of the so-called “tapering” by the Fed, says Jean Charbonneau, senior vice president with Toronto-based AGF Investments Inc. and portfolio co-manager of AGF Global Government Bond Fund; he shares portfolio-management duties with AGF vice president Tristan Sones. (Charbonneau also is portfolio co-manager of AGF Global Aggregate Bond Fund.)

“Most of the normalization is behind us,” says Charbonneau. “Now, the market is reacting more to improving economic fundamentals than to monetary policy. I look at some metrics, and 2.75%-3% for 10-year U.S. treasury bonds is fair value. And Canada is pretty much in the same bucket.”

Charbonneau argues that interest rates may not rise much higher from current levels: “We’ve already gone from a low of 1.38% in July 2011 for 10-year treasuries to about 2.8%-3% today. My best guess is flat to coupon returns in the first half of 2014. Equities are still the favourite asset class. But the bond market is fairly valued, given the low levels of inflation. Real yields are around 2%, which are not cheap nor extremely rich.”

The AGF fund’s average duration is 4.75 years compared with 6.6 years for the bench mark Citigroup world government bond index (unhedged). Says Charbonneau: “In a rising environment, I am bit defensive.”

From a regional perspective, about 87% of the AGF Global Government Bond Fund’s AUM is allocated to developed markets and 13% to emerging markets such as South Africa and Mexico. There’s 33% in the U.S., 4.5% in Japan, 5% in the U.K. and 33% in Europe (the bulk of which is in peripheral countries such as Spain, Italy, Portugal and Ireland).

“These countries have outperformed core Europe and North America,” says Charbonneau, noting that Spain’s and Italy’s government bonds are yielding 4.1% vs 1.84% for Germany’s sovereigns. “The risk/return profile is more attractive than in core Europe.”

From a currency viewpoint, the AGF fund is partially hedged: about half the eurozone exposure and one-third of the U.S. weighting is hedged back to the C$. Pound sterling exposure is unhedged.

Charbonneau is utilizing a similar strategy with AGF Global Aggregate Bond Fund, for which he shares portfolio-management duties with AGF vice president Tom Nakamura. Says Charbonneau: “I’m overweighted in Europe and have trimmed the U.S. exposure and have about 11% in emerging markets.”

This AGF fund’s average duration is 5.25 years vs 6.26 years for the benchmark Barclays global aggregate bond index.

Richard Usher-Jones, partner and vice president with Richmond Hill, Ont.-based Canso Investment Counsel Ltd. who oversees Canso Corporate Value Class Fund, is reluctant to make market calls as his firm is focused primarily on bottom-up investing.

“For Canadians looking for fixed-income exposure, where we find value in foreign issues is particularly in the so-called ‘Maple’ space,” says Usher-Jones, referring to C$-denominated bonds issued by foreign entities in the Canadian market. Some leading issuers of Maples include Goldman Sachs Group Inc., Lloyds Bank PLC and Royal Bank of Scotland.

“Interest rates are at very low levels, and we are concerned about that,” says Usher-Jones. “We’ve been accumulating floating-rate bonds in the past few years.” (Floating-rate bonds have a spread above a reference rate, in the form of the Canadian deposit offered rate.) “These bonds are quite attractive and carry limited interest rate risk. We didn’t have to pay up for that additional option.”

Currently, about 52% of the Canso fund’s AUM is in bonds from foreign issuers, with the majority of those in Maple bonds, and the balance is in Canadian issues. In total, there are about 50 issuers.

The fund’s average duration is 2.9 years vs six years for the benchmark DEX universe all corporate index. Usher-Jones emphasizes that his firm does all of its own research and does not rely on credit-rating agencies.

About 8% of the Canso fund’s holdings is in non-Canadian currencies, hedged back to the C$.

“We don’t come out and say, ‘More than half the portfolio will be in foreign issuers or Maple bonds’,” he says. “But, today, they are very attractive from a quality and a yield perspective.”

Among the Maple bonds, Usher-Jones likes Germany’s Commerzbank AG’s 2023-dated issue, which is rated BB and yields 6.75%. “Everyone seems to love Canadian banks and hate foreign banks,” he says. “But, in our world, some of the most attractive yields are in places people don’t like.”

On the U.S. side, Usher-Jones favours Maples issued by firms such as Goldman Sachs, whose A- rated bond matures in May 2018 and yields 3.1%.

On the Canadian side, he likes Shaw Communications Inc.’s BBB-low bond maturing in 2039 that is yielding 5.8%.

© 2014 Investment Executive. All rights reserved.