International equities markets have strengthened this year despite weakness in recession-plagued Europe and concerns about growth in China. Although fund portfolio managers are emphasizing Europe over Asia, many are generally upbeat, arguing that stocks will shine through the economic uncertainty.

The good news is that the worst appears to be over for Europe. “The effects of the financial crisis are working their way through Europe, with some signs of positive results in places such as the U.K. and particularly Ireland,” says Richard Jenkins, managing director and chairman of Toronto-based Black Creek Investment Management Inc. and lead manager of CI Black Creek International Equity Class Fund. “Those countries that are restructuring internally are getting there, although it takes time and is very painful.”

“Greece is slowly turning, but it will take a very long time,” Jenkins continues. “Spain is ‘early days,’ with 25% unemployment; but housing is finally being priced so they can start selling it. Italy has made a number of reforms, although the political process there is always messy because of the nature of Italian democracy.”

Although Europe is slowly tackling structural reforms, Asia faces its own challenges, adds Evelyn Huang, director, global equities, with Black Creek and portfolio co-manager of the CI fund: “In China, the cheap labour, investment-driven growth story is slowing dramatically. The new government is trying to increase domestic consumption by providing certain levels of health care and social security, so that people will feel more secure and spend money.”

Huang points out that China’s average savings rate is an astonishing 30%-40%.

As a result of rising labour costs in China, multinationals are locating in cheaper jurisdictions such as Vietnam and Bangladesh, thus affecting gross domestic product (GDP) growth in China.

“Growth will slow to a more sustainable level – about 6%-7% nominal growth,” says Huang. “But it’s a healthier rate of growth.”

Jenkins notes that South America is a mixed story, with an investment and offshore oil boom in Brazil that is offset by the worsening economic picture in Argentina and Venezuela.

There’s a similar tale in South Asia, where Pakistan is growing, for example, but India is losing momentum partly because the outsourcing story that helped it prosper in the past has lost some of its lustre.

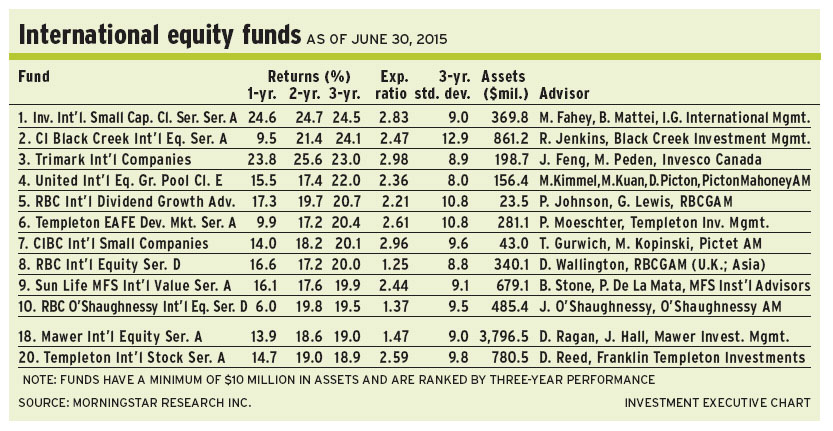

Jenkins and Huang are bottom-up managers who use a blend of value and growth styles. About 64% of the CI fund’s assets under management (AUM) is in so-called Greater Europe (including 15% in the U.K.) and 26% is in Greater Asia (including 8.5% in Japan), with small holdings in markets such as Mexico and the balance in cash.

In a concentrated portfolio of about 25 names, WuXi PharmaTech Inc., a mid-sized Chinese clinical research and outsourcing provider, is a favourite.

“Nine out the top 10 pharmaceutical companies are among [WuXi’s] customers,” says Huang. “[The firm] began in chemical discovery in the early stages of drug development and have added other capabilities, such as pharmacology and biologics. [WuXi has] the potential to be a much larger company.”

WuXi’s American depository receipts are trading on the New York Stock Exchange (NYSE) at about US$20.15 ($20.95) each, or 16 times 2013 earnings. There is no stated target.

European markets may be getting ahead of themselves and perhaps pushing valuations too far, argues David Ragan, director of Calgary-based Mawer Investment Management Ltd., and lead manager of Mawer International Equity Fund.

“A year ago, Europe was far too cheap. We could have bought indices at single-digit multiples,” says Ragan, who shares portfolio-management duties with Jim Hall, Mawer’s chairman and chief investment officer. “Fast-forward to now, and valuations are up by 15%-30%. It’s been a big move – and a great place to be outside of Canada.”

Ragan believes that markets are re-tracing some of their gains: “This is particularly true in Asia and emerging markets, which have been slipping.”

He adds that Japan’s markets have lost some of the steam created by the Bank of Japan’s quantitative easing program unveiled last winter. Indeed, Ragan remains skeptical about Japan.

“People are only looking at the short term,” Ragan says, adding that the massive amount of liquidity pumped into the system by the Japanese has succeeded only in encouraging speculators. “I don’t see how the Japanese recovery ends happily. That’s why we haven’t bought into it. We couldn’t find good stocks there.”

The macroeconomic picture in Europe is better, observes Ragan: “Although growth is still low and there is very high unemployment, especially among the young. But there is some progress in getting more balanced government budgets. They probably were too harsh on the austerity side, which hurt growth. There’s been a gradual shift since last year to people saying, ‘We can spend some; we have to be prudent and can’t just cut our way out of it’.”

From a strategic perspective, Ragan has about 67% of the Mawer fund’s AUM in Europe (including about 36% in the U.K.), plus 18% in Greater Asia, 6% in Latin America, smaller holdings in markets such as in Israel and 6% in cash.

One of the top holdings in the 60-name Mawer fund is Roche Holding AG, a global, Switzerland-based pharmaceutical company that specializes in making so-called “biological” drugs (a.k.a. “living proteins”).

“These drugs are incredibly difficult to copy. That’s one of the reasons we like Roche,” says Ragan, adding that one of Roche’s more successful drugs is Avastin, which is used for treating colorectal cancer. “Even if [Roche’s] drugs go off patent, a generic [drug] firm will have immense difficulty and cost [in] trying to prove [its] drugs are equivalent to Roche’s.”

Roche’s stock is trading at about 227.2 Swiss francs ($252.80) a share, or 14 times current earnings. The stock also pays a 3.2% dividend. Ragan has no stated target.

Another favourite is BASF AG, a global, diversified chemicals firm based in Germany. “[BASF is a] very efficient operator,” says Ragan. “The waste products from one process will be used in the same plant as an input to another process. Because of the scale of operations, that’s how [BASF gets] some cost advantages.”

BASF shares are trading at about 12.9 times current earnings, at 70.50 euros ($96.20). “People are a little bearish on the stock because about half of BASF’s revenue originates in Europe,” says Ragan. “But the rest comes from North America and Asia, which are doing a little better.”

Jeff Feng, vice president of Toronto-based Invesco Canada Ltd. and co-manager of Trimark International Companies Fund, admits he is more pessimistic than he was a year ago. Feng shares portfolio-management duties with Michael Hatcher, head of global equities with Invesco Canada, and Darren McKiernan, vice president.

“In the past 12 months,” says Feng, “global equities’ valuations have shot up. And on the fundamentals side, the big problems in Europe are still there. You don’t read about them as much in the newspapers, but it doesn’t mean they have gone away.”

Europe’s economy is still in the process of finding a bottom, argues Feng: “It will take years, maybe a decade, to deal with deleveraging in the financial system, very high unemployment rates and heavy debt loads at the government level. Those problems aren’t solved very easily. It takes a very long time.”

As for China, Feng maintains that it has become clearer that China’s economic transformation from an investment-oriented focus to being driven by consumption is more challenging than expected. “[China’s] system has too much capacity in many industries. More important, there are some wrong incentives at the local government level to keep that excess capacity,” says Feng, adding that factory managers are focused on top-line growth rather than on return on investment.

Feng does not believe economic reform in China is likely without political reform: “Even for the economy to grow at the forecasted rate of 6%-7%, [China] needs to have a certain degree of political reform. Unless we see a clear sign, we don’t have enough confidence.”

Feng, primarily a bottom-up investor, has become cautious and raised the level of cash in the Trimark fund to about 11.6% of AUM. This is partly the result of reducing the weighting in Japan by half, to 7.5%; Feng believes that country’s quantitative easing program will have little lasting impact on its economy.

The Trimark fund also holds about 29% of its AUM in Asia (excluding Japan), 47.2% in Europe and 4.7% in Latin America.

In the portfolio of 41 companies, Feng likes stocks such as Publicis Groupe SA, a French advertising agency that is among the largest in the world. “Scale is very important in [the ad] business, since multinationals prefer to work with global firms such as Publicis because they want to deliver a consistent message,” says Feng, adding that Publicis has emerged as a global leader in the burgeoning use of social media. “Even though overall advertising spending is growing at 2%-3%, globally, companies that take advantage of the digital side can grow faster.”

Publicis stock is trading about 55.5 euros ($75.50) a share, or 15.4 times current earnings. There is no stated target.

Another favourite is Willis Group Holdings PLC, a global insurance agency that works with large and mid-sized companies. Although strong competition has kept insurance premiums down for the past decade, Feng notes, Willis has been able to grow its top line at a low single-digit rate.

Meanwhile, he argues, Willis is undergoing a restructuring under its new CEO, Dominic Casserley, and insurance rates should go up at some point. “We’ve been waiting a long time,” says Feng, “but that should happen.”

Willis stock is listed on the NYSE and is trading at about US$40.80 ($42.43) a share, or 15.3 times estimated current earnings.

© 2013 Investment Executive. All rights reserved.