International equity markets have been weighed down by concerns about the unresolved European debt crisis as well as by the impact of the slowing Chinese economy. Although fund portfolio managers are divided on emphasizing Europe over Asia, they are generally upbeat, arguing that in spite of the ever-present worries, certain stocks are attractive and will shine through.

Europe’s malaise may continue for some time, says Jeff Feng, vice president at Toronto-based Invesco Canada Ltd., and portfolio co-manager of Trimark International Companies Fund, who shares portfolio-management duties with Michael Hatcher, head of global equities, and Darren McKiernan, vice president.

“The problem,” says Feng, “is we have overleveraged banks [in Europe] and governments tried to bail them out. As a consequence, governments are even more indebted than they were before the financial crisis.” Countries such as Spain have seen the cost of borrowing skyrocket. “Also, we have overleveraged consumers,” he adds. “Put it all together, that’s all working against the region.”

Europeans have to face reality and make painful long-term adjustments. “It will mean spending cuts by both governments and consumers,” says Feng. “There’s no magic bullet. Even if the European Central Bank cuts rates tomorrow, it won’t solve the problems from a fundamental perspective.”

Turning to the other side of the globe, Feng argues that China has to lessen its dependence on heavy infrastructure spending: “[China has] to direct the economy to be more consumer-oriented. Everyone knows this. The question is: how to do it?”

To make this happen, says Feng, China’s government needs to introduce better social safety nets to create more confidence, which will, in turn, spur consumer spending.

“This will take time – and will be a more difficult process than building roads and airports,” says Feng, who anticipates that China’s economic growth will slow to about 6%-7%. “Some people say that 6% is a ‘hard landing’,” he says. “I think [China’s economic leaders] can live with that; 6% or 7% growth is still pretty good.”

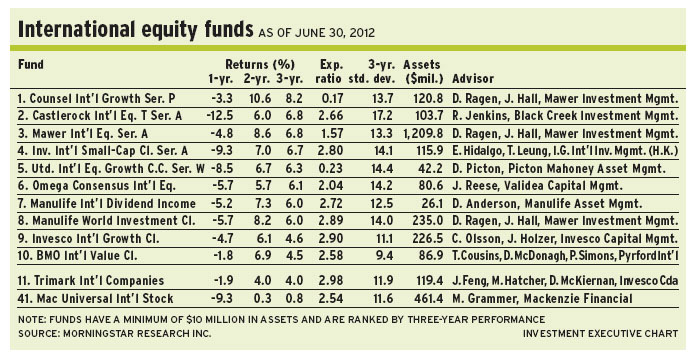

Primarily bottom-up investors, the Trimark fund’s portfolio managers favour companies that can thrive in a slow-growth environment and participate in the faster-growing emerging markets. “For most of our European companies,” Feng explains, “40%-70% of sales are from outside Europe.”

Currently, about 53% of the Trimark fund’s assets under management (AUM) is in Europe, 39% is in Asia/Pacific countries, and 8% is in cash.

One top holding in the 36-name Trimark fund is SMC Corp., a Japan-based maker of automation systems that is benefiting from strong demand in emerging markets. “[SMC is] a leader in pneumatic components manufacturing,” says Feng, noting that the firm has a 38% global market share. “[Its] operating margin was 25.8% for the year ended Mar. 31.” SMC stock is trading at about 7.3 times enterprise value to earnings before interest, taxes and depreciation. SMC’s share price is about 13,270 yen ($168); Feng has no stated target.

Mark Grammer, vice presi- dent at Toronto-based Mackenzie Financial Corp. and portfolio manager of Mackenzie Universal International Stock Fund, agrees that the issues in Europe may continue for some time.

“The European Union has a dichotomy in its economies,” says Grammer. “The economies in the northern part are relatively strong; but in the south, they are facing extreme difficulties. France could also become a problem down the road, if [it continues to move] in the direction that [it’s] headed. President [François] Hollande wants to shorten the retirement age to 60 from 62. That’s a big step in the wrong direction. It’s only reinforcing entitlements and won’t win [France] favours with its northern friends.”

But the picture is considerably brighter in China, Grammer argues: “Fiscal conditions [there] are much better than anywhere in the world.” Grammer subscribes to the ‘soft’ landing scenario: “The deficits are very manageable, and the decision to slow growth has not only been a wise one but effective.”

Grammer maintains that China has successfully forestalled a housing bubble and has moved into an era of measured growth: “The fact [China] lowered [its] gross domestic product growth target below the 8% historical threshold is indicative that [China is] at the point of its maturation when [it doesn’t] need rapid growth to move to sustainable prosperity.”

From an investment perspective, Grammer lately has spent some of the Mackenzie fund’s cash, which has fallen to less than 10% of AUM from around 15%. “Someone asked me,” he says, “what I think of the situation. I said it was horrible. But that doesn’t mean I’m not making investments. We’ve taken opportunities to upgrade the portfolio.”

Currently, about 50% of The Mackenzie fund’s AUM is in Europe, 32% is in Asia/Pacific, 6% is in Latin America, 2% is in Africa and 9% is in cash.

One of the top names in the 53-name Mackenzie fund is Intertek Group PLC, a Britain-based supplier of testing, inspection and certification services. “With the increase in global trade, there’s a growing requirement for more testing and inspections,” says Grammer. “[Intertek] also is involved in commodities and with the growth of ‘fracking’ in the U.S. natural gas industry, which should drive demand for Intertek’s services.”

The shares are trading at about £25.75 ($40.42) each. Grammer has no stated target.

David Ragen, director at Calgary-based Mawer Investment Management Ltd., and portfolio co-manager of Mawer International Equity Fund (formerly Mawer World Investment Fund), who shares portfolio-management duties with Jim Hall, Mawer’s chairman and chief investment officer. Ragen anticipates that European growth will be flat this year.

“You can’t have all this austerity and not suffer through growth,” says Ragen. “There’s been a shift in thinking. The initial focus was on cutting costs and programs. But people were surprised at how much of an impact this is having on the region; it’s worse than people thought. So, there’s been a push recently on the growth side.”

Ragen notes that the recent election of Hollande as France’s president is indicating a tilt back to growth: “The problem is everyone is cutting at the same time. In [Britain], they started cutting before the other European Union countries, while everyone else was still spending. That didn’t leave as big an impact. But if everyone stops spending at the same time, the impact will be far greater.”

Meanwhile, fear has driven investors to the safety of 10-year German bunds, even though their yields are about 1.5%. “That’s a testament to how scared people have become,” says Ragen, a bottom-up stock-picker. “But I wouldn’t buy a German bond for anything. To me, the bond market is one of the riskiest markets out there. It’s way too expensive.”

In contrast, argues Ragen, investors can reap 3%-4% dividend yields in most of the developed world. “There’s a lot going on in the world, but the valuations aren’t ignoring these facts,” says Ragen, who believes China will achieve a soft landing. “If I was given a choice between stocks and bonds, the answer – by far – is stocks. I don’t know what will happen in the near term. But in the medium term, the opportunities are pretty attractive. Eventually, the world will do better.”

From a strategic perspective, about 69% of the Mawer fund’s AUM is in Europe (split between 28% in euro-based stocks and 41% in Britain), with 16% in Asia, 10% in emerging markets, 5% in cash and small weightings in markets such as Australia.

One of the top holdings in the 59-name Mawer fund is Getinge AB, a Sweden-based manufacturer of sterilizers, stents and related medical devices for hospitals. “People won’t cut costs on stuff like this. So, there is a lot more certainty and barriers to entry,” says Ragen, noting that Getinge’s average return on equity has been around 18%. Getinge shares are trading at about 171.7 krona ($24) each. Ragen has no stated target.

Another favourite is Jardine Matheson Holdings Ltd., a Hong Kong-based, Singapore-listed conglomerate with diverse interests in Indonesian car dealerships; the Mandarin Oriental, a luxury hotel chain; and Dairy Farm International Holdings, a prominent Asian retailer. Jardine Matheson stock is trading at about US$48.50 ($49) a share, or roughly 11.7 times trailing earnings. The shares also have a 2.5% dividend yield.

© 2012 Investment Executive. All rights reserved.