Glenn Fortin, global equity analyst and portfolio manager at Beutel Goodman & Co. Ltd., says that the U.S. equity market has been a lacklustre performer so far this year, with the consensus that U.S. larger-cap corporate earnings per share will show little or no growth in 2015.

“The benchmark S&P 500 Index is essentially flat since the beginning of this year in U.S.-dollar terms,” says Fortin. But interestingly, he says, the Nasdaq Index, which has heavy weightings in both the technology and the health-care sectors, has done modestly better, though its return is still in the single-digit range in U.S.-dollar terms. “These two key U.S. sectors have been strong performers so far this year.”

A specialist in U.S. stocks and a value manager, Fortin notes that financial analysts have been downgrading their earnings estimates for 2015, reflecting in part the adverse impact of the strong U.S. dollar on U.S. companies with a global reach. “A large number of large-cap and mid-cap U.S. companies have significant international operations and the strong U.S. dollar is a headwind,” he says.

U.S. corporate earnings are expected to pick up some steam in 2016 as the global economy revives, he says. “Europe’s economy is starting to show signs of life and the stronger U.S. consumer will continue to be an important driver of the U.S. economy, which is in much better shape than most countries in the developed world.”

Also putting a brake on the U.S. equity market’s 2015 performance is the fact that the U.S. equity market is “fairly valued,” says Fortin.” The S&P 500 Index is currently trading at a price/earnings multiple of some 17 times, he notes. This compares with the 10-year average multiple of around 14 times. The historical average multiple is higher if you go beyond the past decade, he says.

Another factor causing uncertainty among equity investors, says Fortin, is the expectation that the U.S. Federal Reserve Board will finally start to raise its policy rate, with the consensus that it is likely to do so in September.

In summary, he says, the U.S. equity market, at present, is “broadly speaking fairly valued.” Within the market, many areas or sectors are “overvalued,” Fortin says. “But there are still pockets of value and this is where stock selection comes to the fore.” Beutel Goodman’s U.S. equity team is finding some stocks that meet its criteria. “This is even in sectors, such as consumer staples, where the stocks are generally expensive.”

The Beutel Goodman U.S. equity team targets larger-cap companies where the public market value is below “what we consider to be the value of the business, based on discounted free-cash-flow analysis.” The team looks for a return of 50% from the stock over a three-year period.

Fortin and colleague Rui Cardoso co-manage portfolios of large- and mid-cap U.S. equities totalling US$3 billion, including the U.S.-equity portion of balanced funds. Included in their mandate is Beutel Goodman American Equity. This fund is measured against the S&P 500 Index and has an average market cap of US$91 billion versus the benchmark’s average of US$130 billion.

The U.S. equity portfolio contains between 25 and 35 names. There are currently 26 holdings and the top 10 account for more than half of the portfolio.

Beutel Goodman American Equity, says Fortin, has overweight positions in a number of key U.S. sectors such as information technology, which is 20.1% of the S&P 500 Index, financials (16.2% of the index), health care (15.1%) and industrials (10%). “Industrials are our biggest percentage overweight in the portfolio,” says Fortin. It is also overweight in telecommunications services, “which is only a small weighting in the benchmark at 2.3%.”

The fund has no holdings in the materials sector (3.2% of S&P 500 Index) and utilities (3%). It has underweight positions in consumer-discretionary stocks (12.5%) and consumer staples (9.5%). Finally it is underweight in energy, which is 8% of the benchmark. “We are finding some energy-related names that offer value, such as companies supplying products to the energy industry but are not targeting the energy producers.”

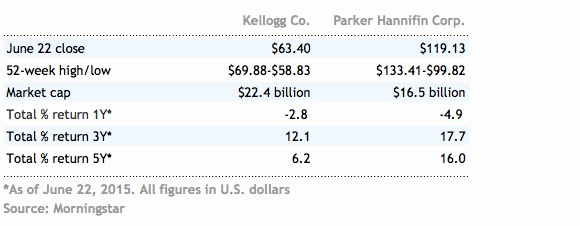

Fortin reports that a new addition to the portfolio in the industrial sector is Parker Hannifin Corp. (NYSE:PH), which is “a large-mid-cap with a market capitalization of US$17.1 billion.” Parker-Hannifin is a diversified manufacturer of motion and control technologies and systems.

“Its customer base, which tends to be sticky, is well diversified,” says Fortin. A plus, he notes, is that some 50% of its products and systems are custom-made, which is value-added, higher-margin business. Also, the company generates significant free cash flow and is committed to returning some of that to shareholders, he says. “Well-executed capital-allocation strategies are important to us in evaluating businesses.”

A new addition in the consumer-staples sector is Kellogg Co. (NYSE:K), which manufactures and markets cereal and snacks. “This long-established global food giant has introduced better cost management throughout the company and this should drive improved profitability,” says Fortin.

In this sector, the U.S. equity team has sold its holding in Kraft Foods Group, Inc. (Nasdaq:KRFT). This company is to be merged with H.J. Heinz Co. to form The Kraft Heinz Co. This merger is expected to close in the second half of this year. “The take-out price for Kraft exceeded our internal target price,” says Fortin. “It is hard to value the combined entity.”

In information technology, Beutel Goodman American Equity continues to focus on those companies that address the enterprise market rather than the consumer. “The enterprise specialists have high levels of recurring revenue, there are high barriers to entry in their businesses, high profit margins and the companies are strong cash-flow generators.”

A long-time top-10 holding in the fund is the software and services company Oracle Corp. (Nasdaq:ORCL). “Its software is embedded in its customers’ businesses and it is difficult for them to switch tech companies.” Other top technology holdings include Symantec Corp. (Nasdaq:SYMC), a software company focusing on both security (including providing its Norton anti-virus software) and storage software.

Also in the top 10 is Amdocs Ltd. (Nadaq:DOX), which specializes in software and services for the telecommunications sector. Another significant tech holding is Teradyne Inc. (NYSE:TER), which makes automatic test equipment for semiconductors, wireless and the defence/aerospace industries. “It is a dominant player in this industry, a strong free-cash-flow generator, and has a stellar balance sheet with a substantial holding in cash,” says Fortin. “The company is good at giving money back to shareholders, he adds.” We continue to be enthusiastic about these tech holdings, but have not added to them, of late.”

The biggest health-care holding in the fund continues to be Baxter International Inc. (NYSE:BAX). The company, says Fortin, is in the throes of splitting into two separately listed global health-care companies. “This move by Baxter is a way of creating value for shareholders.” Its medical-products business will, he says, remain under the Baxter International banner and continue to trade on the New York Stock Exchange under the ticker BAX. Its biopharmaceuticals business, which is to be known as Baxalta Inc., will trade on the NYSE on a regular basis under the ticker BXLT, effective July 1.

Baxter common shareholders of record on June 17 received one common share in Baxalta for every one Baxter share held at that date. “We will continue to own both pieces of the original Baxter,” says Fortin. “The two companies are expected to continue the Baxter legacy of diligently returning cash to shareholders,” he adds.

Other significant health-care holdings include Eli Lilly and Co. (NYSE:LLY), Merck & Co. (NYSE:MRK) and Johnson & Johnson (NYSE:JNJ). These three companies plus Baxter and Baxalta have “solid existing franchises and a good product mix,” Fortin says, “as well as promising pipelines of new products and therapies.” At present, he notes, the team is “happy with its health-care holdings and, like technology, is not adding to them, at this juncture.”