Eric Bushell, chief investment officer at Toronto-based Signature Global Asset Management, says there is a need for investors to focus on the impact on their portfolios from shifts in foreign-exchange rates.

“Some countries have moved aggressively to help reduce the external value of their currencies, so as to stimulate exports,” he says. “The moves in foreign-exchange rates can be sizeable and have an impact on portfolio returns.”

The Europeans, for example, says Bushell, “have exhausted the traditional monetary-policy measure of lowering interest rates.” He points out that the European Central Bank’s policy rate is already in negative territory.

Bushell says that the ECB is relying increasingly on a weaker currency against the U.S. dollar, as an important policy tool. The euro has already declined by some 20% against the greenback in the last 12 months, he notes. “There is a possibility that it could continue on its downward path,” he says.

The ECB’s ambitious quantitative-easing program, (which involves the purchase of 60 billion euros worth of fixed-income assets a month), will both put a lot of money in circulation and could lower European interest rates further, he says. “If the interest-rate differential between Europe and North America remains intact, it is likely that the strong flow of institutional investor money out of Europe and into North America will continue,” says Bushell.

The Canadian dollar has also declined sharply against its U.S. counterpart, says Bushell. “Those Canadian investors with U.S.-dollar-denominated assets have benefitted from this.”

In addition to an active foreign-exchange strategy, there is also a need, he says, for global investors to recognize that the financial markets are “fragile and volatile.”

Liquidity in these markets has been severely curtailed, says Bushell, due to tighter regulations on the use of capital by investment dealers and banks in the wake of the global financial crisis. “If a financial asset is perceived to lack liquidity, it can suffer a severe drop in the event of a market shock.”

This vulnerability in the financial markets suggests that investors might want to keep higher than historical cash holdings to both protect capital and take advantage of a pullback.

Bushell and his team of specialists are responsible for managing some $55 billion in assets at Signature, a separate portfolio-management group under CI Investments Inc.’s umbrella. Of the assets, roughly half is in fixed-income securities and half in equities, he says. “In the case of equities, we have more investments outside of Canada than in Canada and in the case of fixed income, some two-thirds of the holdings are Canadian.”

When it comes to asset allocation between bonds and equities in balanced portfolios, Bushell reports that Signature has substantially reduced the equity component in its Canadian balanced portfolios in favour of bonds and cash. “Equities have had a strong showing and the valuations were high.”

The U.S. Federal Reserve Board is likely to proceed to raise its policy rate this fall, says Bushell. But, his call is that the bond market is not overly concerned about this prospect. Bond-market participants are aware of the strong deflationary forces still at work in the global economy. “We will likely be stuck in a low-interest-rate environment for the next decade.” This is good news for dividend-paying stocks, he adds.

A caveat for global equity investors, he says, is that they not underestimate China’s determination to expand its exports and challenge the strength of western multinationals. “China is moving up the value-added production chain in areas such as semiconductors, power generators and other heavy-industry products. “This will impact established western multinationals in those fields.”

In addition to his role in determining the overall strategy for Signature, Bushell is lead manager of CI Signature Select Canadian. The fund, which had assets of $2.7 billion at the end of May, has a Silver rating from Morningstar’s manager-research team. Bushell is also lead manager of CI Signature Select Canadian Corporate Class, a similar fund, which had assets of $1.9 billion at the end of May.

CI Signature Select Canadian has some 9% in cash, says Bushell, which is “slightly higher than it has been historically.” Of the equity holdings, the fund had 43% in Canada, 28% in the United States, 15% in Europe and 5% in the Pacific region.

Bushell notes that the cash portion of the portfolio is held in U.S. dollars. The U.S.-equity component is not hedged, he adds, but the fund’s holdings in European equities are 90% hedged. “As the Canadian dollar and the euro have declined sharply against the U.S. dollar, this foreign-exchange strategy was a significant contributor to the fund’s performance in the last year.”

Of the sector weights, financial services represent some 31% of the portfolio, consumer discretionary 10%, consumer staples 9%, technology 9%, health care 8% and industrials 8%. Natural resources constitute roughly 14% of the fund, of which 10% is in energy and 4% in basic materials.

It has been challenging to find new names in Canada, says Bushell. “We need new Canadian businesses and more initial public offerings.” CI Signature Select Canadian recently participated in the IPO of Ottawa-based e-commerce software maker Shopify Inc. (TSX:SH), which was listed in May. “The stock has done well since,” says Bushell. “E-commerce and, more significantly mobile e-commerce, are taking off.”

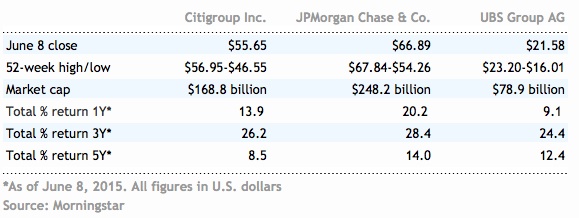

In the financial-services sector, the Signature group is finding opportunities among global banks such as Citigroup, Inc. (NYS:C), JPMorgan Chase & Co. (NYSE:JPM) and Switzerland’s UBS Group AG, which has an American Depository Receipt and trades in New York under the ticker UBS.

“These banks have all had to pay a number of large fines to different jurisdictions for a series of infractions, and this issue appears to be behind them,” says Bushell. “This, plus the fact that these banks have rebuilt their balance sheets, puts them in a better position to return capital to shareholders,” he notes. “Furthermore, the stocks are out of favour and offer value.”

In natural resources, Signature is becoming more enthusiastic about base-metals stocks. “We have been underweight the miners since 2011, but have been easing our way back, as there is growing demand for them for capital projects in such industries as renewable energy.” Bushell reports that the fund participated in the recent common-share offering by Canada’s First Quantum Minerals Ltd. (TSX:FM), a major copper producer.

Signature is cautious about energy producers and prefers energy-services companies, says Bushell. “The stocks of the former have not corrected sufficiently to reflect the steep decline in the oil price and the limited outlook for its advance, whereas the energy-services stocks were hit hard after the commodity-price drop.” An energy-services stock that the group favours is Nabors Industries Ltd. (NYSE:NBR).

The challenge to energy producers, says Bushell, is that oil and gas prices are capped. “It’s a question of supply, a lot of resources can be brought to market quickly if these commodity prices rise.” There is a tendency, he says, for investors to underestimate the magnitude of the U.S. shale business. “This business is much larger than that in Western Canada.”

In the consumer-discretionary sector, the Signature group likes select hotel companies. Bushell highlights Hilton Worldwide Holdings Inc. (NYSE:HLT). “The industry is in good shape; consumer confidence in the United States is strong.”

Bushell continues to pare back CI Signature Select Canadian’s holdings in the consumer-staples sector. “Many of these stocks are expensive,” he says. A recent sell from the portfolio is Kraft Foods Group, Inc. (Nasdaq:KRFT), which is to be merged with H.J. Heinz Co. to form The Kraft Heinz Co. This proposed merger is expected to close in the second half of this year.

“We had already trimmed our position in Kraft prior to the merger announcement in March,” Bushell says. “This is because branded foods are struggling with weak volumes and pricing, as natural foods and private-label products take increasing market share.”