Mark Thomson, managing director, equities, and head of research at Beutel Goodman & Co. Ltd., says that the valuation on the S&P/TSX Composite Index remains reasonable and there are opportunities to be had in a number of individual names.

A seasoned value manager, Thomson points out that certain sectors of the Canadian big-cap universe appear to be expensive. Here he includes utilities, pipelines, real estate investment trusts and gold-mining companies. But he adds that he is finding value among the Canadian chartered banks, energy producers and telecommunications-services stocks. “It is certainly possible to construct a well-priced diversified portfolio of high-quality Canadian big-cap names at this time.”

The S&P/TSX Composite Index is currently trading at a price-earnings ratio of about 17 times trailing earnings per share. “This is not high, looking back over the past 14 years.” Also, the dividend yield on the index, at 2.7%, is within the dividend-yield range over that period, Thomson says.

A specialist in financial services and long-time proponent of investing in the major Canadian chartered banks, Thomson says that these stocks have been out of favour and are cheap.

Bank stocks are currently trading at a P/E multiple ranging from 10 to 12 times, “which is more reasonable than the index.” In addition, he says, they have a dividend yield of from 3.7% to 4.5% depending on the bank, versus 2.7% for the benchmark. While the banks collectively account for some 21% of the index, they represent a far larger slice of the index’s total earnings, he adds.

Thomson is not swayed by the naysayers on Canadian bank stocks, who point to what they consider to be the high short positions on some of the major bank shares.

“There has historically been a lack of appreciation, particularly among U.S. investors, about the importance of the Canadian banks’ domestic retail- banking operations and the oligopolistic nature of the Canadian market,” he says. Also, he adds, “compared with their U.S. counterparts, the Canadian banks face a more predictable and consistent regulatory environment.”

Addressing the concerns about the Canadian banks’ exposure to potential weakness in the domestic housing market through their mortgage portfolios, Thomson says that there is a significant Canadian government backstop to this business through Canada Mortgage and Housing Corp. Also important to note, he says, is that “the average amount of equity in a home in Canada is 70% versus 40% to 45% in the United States.”

A long-time enthusiast when it comes to Canadian telecommunications- services stocks, Thomson is also finding some value in this sector. “The three main players continue to dominate the telecom-services business, despite the best efforts by the federal government to reduce the barriers to entry.” These companies, he adds, continue to be powerful cash-flow generators. “This is something we focus on.”

Of the energy sector, Thomson says that there is value to be had in specific Canadian low-cost producers that are not on the list of favourites in the oil patch. “Some of the brand-name, big-cap producers are trading at valuations that are factoring in an oil price in the high US$70s per barrel,” he says. Thomson prefers those energy stocks where the valuation is predicated on a more modest oil price.

Beutel Goodman manages assets of $42 billion. Of that total, Thomson and his team manage $22 billion in equities, of which $15.5 billion is in Canadian equities. This team’s mandates include the flagship Beutel Goodman Canadian Equity, a Morningstar gold-medalist fund in its category.

The investment process is essentially bottom-up, says Thomson. “In the case of big-caps, we look for a stock to produce a minimum total return of 50% over the next three years and automatically sell one third of our holding once the stock reaches our target price and then reassess the stock.”

Beutel Goodman Canadian Equity, with 32 names, is overweight in financials at 42.3% of the portfolio versus 34.9% of the index. Another overweight position is telecom services at 10.2% versus 4.7% of the index.

The portfolio is underweight in the energy sector at 14% (21.1%), and has no holdings in pipelines. It is also underweight materials at 3.9% (11.1%), and within that sector has no holdings in gold stocks. Nor does it have any holdings in the utilities and health-care sectors.

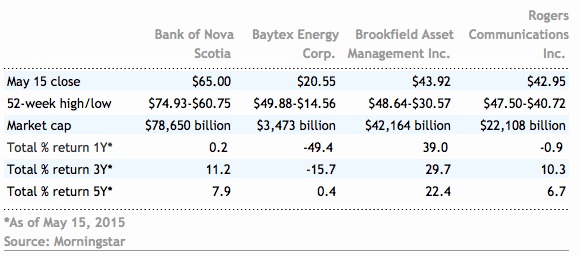

Four of the Big Five Canadian banks feature in the fund’s top-10 holdings. In order of their weightings, there are significant positions in Toronto-Dominion Bank (TSX:TD), Royal Bank of Canada (TSX:RY), Bank of Nova Scotia (TSX:BNS) and Canadian Imperial Bank of Commerce (TSX:CM).

Of these four banks, Thomson currently favours Scotiabank. The stock, he says, trades at a discount to that of TD and Royal. There are concerns, he says, about Scotiabank’s foreign operations in countries such as Mexico, Chile and Peru.

“Scotiabank is not among the top three banks in each of these markets and therefore faces competitive issues,” he notes. “Also, some of these economies are vulnerable to the pullback in resource prices.” Thomson believes a lot of these investor concerns are already reflected in Scotiabank’s stock price.

A non-bank financial that he has been adding to is Brookfield Asset Management Inc. (TSX:BAM.A). A little under half of its asset value is in its real estate, infrastructure and renewable power entities, says Thomson. “The remaining value is in its asset-management franchise.” In all, he says, Brookfield is “highly skilled at managing its businesses and the underlying profitability of the company is not being fully recognized by the market.” Of the life insurers, Thomson cautions that many of these stocks have had a good run. “At present, we do not see the return prospects from some of these stocks that we look for in an investment.”

Thomson currently favours Rogers Communications Inc. (TSX:RCI.B) in the telecommunications-services sector. The stock, he says, trades at a discount to its peers. Rogers’ president and CEO Guy Laurence is “doing a good job and customer turnover should come down over time.” The stock, says Thomson, should benefit from both an improvement in the company’s operating outlook and a reduction in its valuation discount.

In energy, Thomson and his team have been adding to the fund’s holdings in Cenovus Energy Inc. (TSX:CVE), an integrated oil company with oil-sands operations in northern Alberta, and Baytex Energy Corp. (TSX:BTE). The latter has some 82% of its production in crude oil and natural-gas liquids. Its three key resource plays are the Eagle Ford in Texas, Alberta’s Peace River oil-sands, and the Lloydminster heavy-oil play that straddles Alberta and Saskatchewan.

“Cenovus and Baytex are low cost producers, with reasonable balance sheets and are trading at valuations that are based on modest oil price assumptions,” says Thomson.

In the materials sector, Thomson points out that the agricultural stocks have had a good run. “They do not represent the opportunity that they once did, though they continue to be exceptionally good businesses.” He reports that the team recently sold one third of the portfolio’s holding in the fertilizer company Agrium Inc. (TSX:AGU).