Plunging oil prices have grabbed the headlines – but they aren’t the only challenges you and your clients are likely to have to deal with this year.

The policies and actions of central banks are just as important – and may be more important – in determining how your clients’ investment portfolios should be positioned and the return your clients reasonably can expect to earn. How these banks handle the crucial issue of interest rates, for example, will be a central focus of 2015.

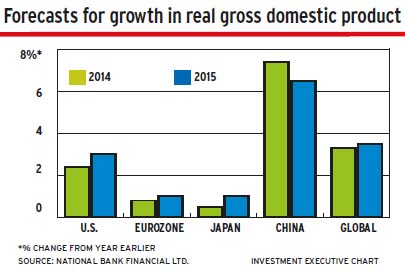

Central bank policy-makers are facing an especially turbulent global economy this year. For one thing, there are vast differences in economic growth rates around the globe.

U.S. real gross domestic product (GDP) growth has accelerated to about 3%. Europe and Japan are trying desperately to avoid recession and deflation, and will be lucky to achieve growth of 1%-1.5%. At the same time, China’s economic growth is slowing to around 6.5%-7%, but India is picking up steam and could see an 8% rise in real GDP vs about 5% in 2014.

The dramatic drop in oil prices to less than US$50 a barrel in early January from an average US$93 in September is exacerbating the situation. Lower oil prices are a boost to consumer spending because consumers have more to spend on other things after filling their cars’ gas tanks. And lower oil prices bring down costs for energy-intensive companies.

But the drop in the price of oil also causes layoffs by driving high-cost oil producers out of business and causing the survivors to cut their investment in future capacity dramatically.

Nor is the impact uniform. Oil is priced in U.S. dollars (US$). And with the greenback rising strongly against most other currencies, including the euro, the yen and the Canadian dollar (C$), some of the price drop is eliminated when oil prices are converted to home currencies. As of Dec. 31, 2014, the euro was down by 8% against the US$ since the end of August; the yen had fallen by 13.2% in the same period.

Furthermore, there is great uncertainty about how long oil prices will remain at today’s levels or where they will settle in the medium term.

If oil prices bounce back quickly, consumer confidence and spending could be affected negatively. On the other hand, if oil prices remain low for an extended period, economic growth could surprise on the upside and potentially generate inflationary pressures through strong wage increases.

The challenge for central banks is to navigate these treacherous waters and help the global economy back onto an even keel.

However, central banks face yet another challenge. Their use of quantitative easing (QE) to help to restore growth after the great recession of 2008-09 has put central banks in new territory. The tactic has never been used before, so there is no historical data on QE’s effectiveness.

More important for today, there’s no experience with unwinding the stimulus. Financial markets will be monitoring what the U.S. Federal Reserve Board, the European Central Bank (ECB) and Bank of Japan (BoJ) say and do very carefully. Markets will react fast and sharply if participants think the bankers’ policies are harming prospects for economic growth.

Most of the attention in the coming months will be on the Fed. “It’s getting harder and harder to justify U.S. rates where they are,” says Leo de Bever, former CEO of Alberta Investment Management Corp. in Edmonton. The Fed’s rate for overnight borrowings by banks, referred to as the “Fed funds target rate,” has been 0.25% since late in 2008.

But markets are nervous about higher rates – and the Fed is treading carefully. It wants to be sure the economy is strong enough to withstand higher rates before making any changes. What markets fear is that the Fed will raise interest rates too quickly and the U.S. economy will grind to a halt. That would affect every other country and region negatively.

The Fed’s first increase in rates is likely to come around mid-year. As Jurrien Timmer, director of global macro and portfolio manager with FMR LLC (aka Fidelity Investments) in Boston, puts it: “We are assuming the U.S. economy is healthy enough.”

But the Fed may delay any rises until later in the year or even until 2016. The Fed says the timing will be “data-dependent.” That is, the central bank will not raise rates until it believes that there is sufficient evidence that the U.S. economy is on a self-sustaining growth path.

Economic growth in the U.S. is dependent primarily upon consumer spending, which accounts for 70% of GDP. And consumer spending depends largely upon consumer confidence. If consumers become worried about job security and curtail expenditures, GDP growth will slow. And if consumers are hesitant, companies won’t expand their business or hire more workers.

U.S. consumer confidence currently is high, with the rate of unemployment low and more money available for spending as a result of low oil (and gasoline) prices.

However, rising interest rates and the potential negative effect they could have on the cost of mortgages or other debts could erode confidence. Consumers also may become alarmed if oil prices rebound quickly or the jobless rate stops falling.

The worst-case scenario is an increase in U.S. rates that is reversed quickly. This could cause consumers, businesses and investors to lose confidence in the ability of the Fed and other central banks to support and guide economies.

Ross Healy, chairman of Strategic Analysis Corp. in Toronto, and Nandu Narayanan, chief investment officer with Trident Investment Management LLC in New York and portfolio manager of several funds sponsored by CI Investments Inc., are among those who believe that QE has only delayed a collapse of the U.S. economy. Their thesis is that the U.S. essentially is bankrupt and must restructure its economy and finances before the country can return to healthy growth.

This is not a widely held view, but there are mainstream portfolio managers, such as Wendell Perkins, senior portfolio manager at Manulife Asset Management (U.S.) LLC in Chicago, who don’t believe the U.S. can withstand an increase in rates this year.

This group fears that if the Fed moves too fast, there could be a general loss of confidence in central banks and their policies, which would be very damaging to the global economy.

You and your clients also have to watch the moves made by the ECB and the BoJ – particularly if your clients have significant investments in those regions. (See the “Outlook 2015” special report in the Building Your Business pullout section in this issue of Investment Executive.)

If the ECB does not provide enough support for the eurozone economy and that region moves back into recession, there’s a real risk of deflation developing, which would prevent the eurozone from getting on a path of healthy economic growth.

Deflation is defined as sustained, broad-based drops in prices that results in consumers putting off purchases year after year because they believe prices will be lower in another year. Economies cannot continue to grow in that environment because there isn’t enough demand.

This scenario is what has happened in Japan during the past several decades; its economy has grown little since 2013. The BoJ’s current aggressive QE program is aimed at getting Japan’s economy finally out of deflation; although that strategy is expected to succeed, that is by no means certain.

Meanwhile, the ECB wants to implement a QE program of its own but needs the acquiescence of Germany, which is concerned about potential inflation, at the least. However, with the recent slowing of Germany’s economy, that country probably will go along with some QE.

© 2015 Investment Executive. All rights reserved.