Asia’s economies are expected to chug away at a respectable pace in 2013, although the growth won’t match previous peaks. However, an increasing proportion of growth will come from domestic activity, which is expected to be more stable than the global export trade that had stimulated the economic rise of many Asian countries.

For the region as a whole, the World Bank is forecasting growth of 7.6% in 2013 vs 2012’s estimated 7.2%. Although these are the slowest growth rates in the region since 2001, they are about three times the pace in the major developed economies in North America and Europe. Southeast Asian countries, such as Thailand, Malaysia and Indonesia, are growing the fastest due to strong domestic demand and rising investment, while countries such as Taiwan and Korea have been hurt by their greater reliance on global export markets.

“Southeast Asia is experiencing a structural rise in domestic demand,” says Eng Hock Ong, portfolio manager in Singapore for AGF Asian Growth Class Fund, sponsored by Toronto-based AGF Investments Inc. “The population is young, and demographics are pushing up consumer demand. Better government policies are creating the confidence to invest and spend, and interregional trade is resilient.”

The block of 10 countries that make up the Association of Southeast Asian Nations (ASEAN)has a population of 600 million people, roughly half the population of India, and ASEAN’s combined gross domestic product (GDP) of US$1.7 trillion is almost double that of India. By 2015, the ASEAN countries will be a common market trade barriers are being dismantled creating a free flow of services, goods and labour.

“There is an abundant supply of young and educated workers in the ASEAN bloc,” says Chuk Wong, lead manager of Dynamic Far East Value Fund, sponsored by Bank of Nova Scotia-owned GCIC Ltd. in Toronto.

With China entering an easing mode in terms of government policy, and its economy showing signs of recovery, other Asian countries can expect to benefit from increased trade with it.

“Growth is increasingly being driven by rising trade between Asian countries and a higher level of domestic economic activity,” says Phil Langham, head of emerging-market equities with RBC Global Asset Management Inc. in London and manager of RBC Emerging Markets Equity Fund. “The cost of borrowing has been falling for corporations, credit growth is strong and governments are in a position to spend on infrastructure. Low mortgage penetration means there is significant pent-up demand for housing.”

But despite growing wealth, some economies in the region still are tied to the fortunes of the West. And if the West’s troubles worsen, the pain will be felt by Asia’s exporters and manufacturers, affecting both employment and growth.

In addition, monetary easing by the big central banks in the developed world has boosted the currencies of countries such as Korea and Taiwan, which has hampered exports.

Mark Grammer, senior vice president of investments at Toronto-based Mackenzie Financial Corp. and manager of Mackenzie Universal Global Growth and International Stock funds, expects Asian stock markets will benefit as investors recognize that the region warrants a lower risk premium: “As investors recognize the lower risks of Asia, there should be an expansion in Asian price/earnings multiples, which I expect will eventually be higher than in the U.S. and Europe. Higher multiples, combined with earnings growth, will lead to healthy returns.”

Here’s a look at a handful of Asian markets (except China, which is covered on page B13):

– INDONESIA. Indonesia remains a favourite among fund portfolio managers due to its strong economy and rising standard of living. The country is endowed with natural resources, including oil, gas, rubber, coffee, palm oil and coal, and is well positioned to supply China. Domestic consumption also is rising rapidly.

Grammer likes Bank Bukopin, a microlender benefiting from regional growth. Wong likes Bank Rakyat Indonesia.

– THAILAND. Henry Chan, manager in Hong Kong of Fidelity Far East and Fidelity AsiaStar funds, sponsored by Toronto-based Fidelity Investments Canada ULC, says underleveraged consumers in Thailand give the credit industry a lot of room to develop, so he likes banks and real estate.

Ong sees banks as a good way to get exposure to a rising economy. The AGF fund holds shares in Kasikornbank PCL.

The Dynamic fund holds shares in Siam Commercial Bank Public Co. Ltd.; Pruksa Real Estate PCL, which specializes in low-cost housing and is a beneficiary of migration to cities; and Delta Electronics PCL, a manufacturer of basic electrical components such as power switches.

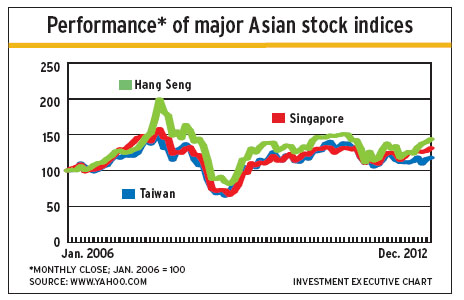

– TAIWAN. Wong says the export-oriented Taiwanese market is offering some great companies trading at low valuations for careful stock-pickers. He likes Chailease Holding Co. Ltd., a company that leases manufacturing equipment to small to medium-sized businesses.

Fund portfolio managers are cautious on Taiwan’s technology sector, which is exposed to global trade. But Ong likes Hon Hai Precision Industry Co., a maker of parts for smartphones that has moved some plants to mainland China to reduce labour costs.

– SOUTH KOREA. Chan is looking for plays on domestic consumption rather than exports, and likes Orion Confectionary Co., a food and beverage company that produces a bestselling chocolate pie. Chan has been cutting back on the Fidelity funds’ previously overweight positions in telecom companies as valuations have risen, but he still likes the theme and the funds hold shares in SK Telecom.

Ong, though, favours some exporters. The AGF fund’s largest holding is in Samsung Electronics Co., and the fund also holds shares in Hyundai Motor Co.

– INDIA. Mihir Vora, chief investment officer in Mumbai with Birla Sun Life Asset Management Co. Ltd. and manager of Excel India Fund, sponsored by Excel Funds Management Inc. of Mississauga, Ont., expects growth in India to pick up in 2013 to around 7% better than an expected 5%-5.5% for 2012, but far from the heated 9.7% pace of 2010. To stimulate growth, India’s government is investing in infrastructure and easing restrictions on foreign investment and foreign borrowing. Vora also expects lower interest rates in 2013, but inflation of 7% is a concern and will limit the drop.

Vora is optimistic about the service side of the economy, which makes up 60% of India’s GDP, followed by manufacturing at 25% and agriculture at 15%. Exports are growing rapidly, but India still has a trade deficit.

Vora likes industrial companies that will benefit from capital expenditures. Top holdings in the Excel fund include Larsen & Toubro Ltd., a multinational conglomerate with interests in machinery manufacturing and construction. And Vora also is partial to financials and the retail sector, which will ride the wave of stronger consumer spending. Financial services, including insurance companies, make up a generous 28% share of the Excel fund’s portfolio, including ICICI Bank Ltd., Infrastructure Development Finance Co., Power Finance Corp. Ltd. and HDFC Bank Ltd.

In retailing, Vora likes multi-product, nationwide retailer Pantaloon Retail India Ltd. His fund is overweight in the auto sector and holds shares in Bajaj Auto Ltd. and Tata Motors Ltd.

© 2013 Investment Executive. All rights reserved.