Over the past year, rising stock markets have sparked a strong flow of new assets under management (AUM) into the brokerage and fund-dealer businesses. But this surge toward stocks may be coming at the expense of financial advisors who work at the deposit-taking institutions.

For the parts of the retail investment business that are heavily geared toward equities, the resurgence in the stock markets – including new all-time highs for certain indices – has boosted the AUM and productivity of front-line sales staff. Yet, according to the results of this year’s 2014 Report Card on Banks and Credit Unions, it appears that the fortunes of bank and credit union reps are heading in the opposite direction overall.

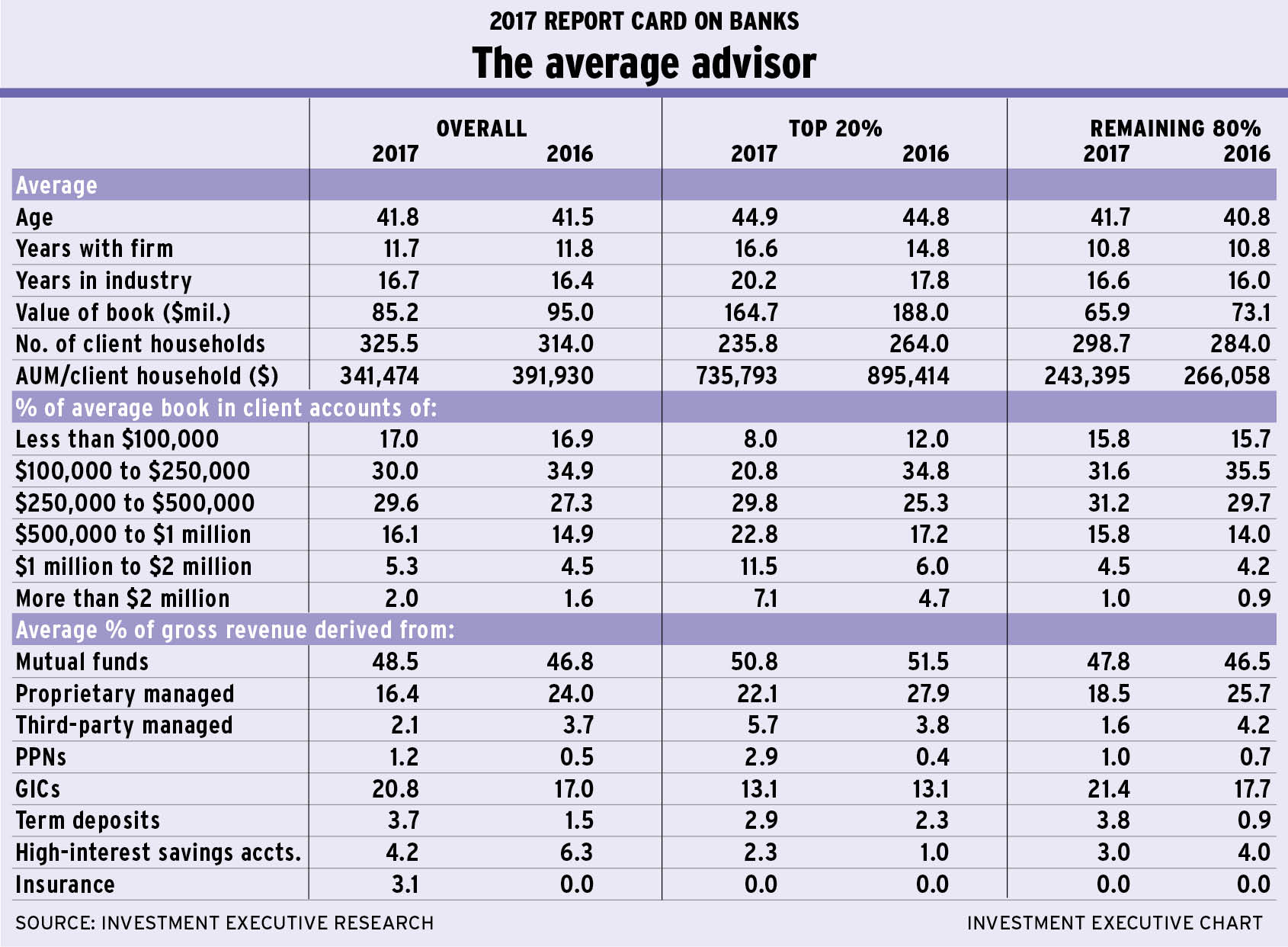

Average AUM for these advisors is down to $51.4 million from $57.3 million in 2013. At the same time, the number of client households these advisors are serving has jumped to 469.9 from 375.2.

Indeed, the data appear to indicate that advisors in the banking channel have been challenged to retain AUM over the past year. Thus, in the face of this trend, these advisors are trying to ramp up the volume of clients they serve. This overall decline in AUM and increase in client rosters has led to a decline in productivity as well. Average AUM/client household is down to $222,741 compared with $262,257 in 2013.

Given the big gains that reps in the brokerage and fund dealer businesses reported this year, it appears that client assets are migrating in their direction. The reasons for this trend are not hard to fathom. Given the exceptionally low interest rate environment, returns on cash and fixed-income are weak while stock-market returns have been strong.

In the immediate aftermath of the financial crisis of 2008-09, clients may have been willing to accept meagre returns, given their growing appreciation for the volatility that can accompany stock markets. Now, however, with equities rising relentlessly and more time since the crisis, some of that aversion to risk may have dissipated. As a result, more clients are chasing equities, which are higher-risk, higher-return assets.

For advisors plying their trade with deposit-taking institutions, this migration toward equities puts their AUM under pressure as clients shift to brokerage and fund-dealer reps who can offer direct access to equities holdings, along with mutual funds and exchange-traded funds that provide some equities exposure as well.

This basic shift in asset allocation is evident within bank-based advisors’ businesses. Looking at the two biggest components of the average advisor’s book – mutual funds and guaranteed investment certificate (GICs) – the general trend away from fixed-income and toward riskier, higher-return assets is clear. The average advisor in the banking channel now has 51.2% of his or her book in mutual funds, up from 46.8% last year. At the same time, exposure to GICs is down to an average of 24.5% from 27.4% in 2013.

So, for the AUM that these advisors have managed to retain over the past year, there has been an internal shift toward riskier asset classes. And it seems likely that it’s this same trend that’s weighing on their AUM and productivity.

This pressure is being felt throughout all segments of the banks’ and credit unions’ advisory sales forces. Both the top performers (the top 20% of advisors, as measured by AUM/client household) and the rest of the advisors are experiencing the same decline in average AUM and productivity, along with an increase in client numbers. However, top-performing advisors do appear to be distinguishing themselves from the rest by doing a better job of stanching the asset outflow.

Looking at the top 20% of advisors, they’re outperforming the rest of the banking channel in AUM retention. Although average AUM for top producers is down year-over-year, the decline is just about 2% vs a decline of almost 15% for the rest of the channel.

The top 20% of advisors still have average AUM of $119.3 million, which is down a bit from $122 million in 2013. And this amount is still well above the $91.6 million this segment reported in 2012 and more than double the $37.4 million recorded by the average advisor in the rest of the channel.

The top performers appear to be doing a superior job in retaining AUM, and it seems they are more aggressive in adding new accounts in the face of declining AUM. On average, the number of client households served by the top 20% of bank-based advisors is up by almost 11% year-over-year compared with slightly more than a 9% gain for the rest of the channel.

Average productivity for both the top performers and the rest of the channel is certainly taking a hit, but the decline is less severe for the top 20% – and their reduced production was driven more by an increase in client numbers than a drop in overall AUM.

This effort to build up client rosters among advisors also is reflected in the account distribution data. For one thing, both segments of advisors are reporting growth in their smallest accounts (the sub-$100,000 category), which now represent 32.4% of the average book overall, up from 31.9% last year.

The swing isn’t huge, but it’s indicative of the acquisition of new clients in the banking channel, which tends to start with smaller accounts. Moreover, virtually all of this activity appears to be coming from the top 20% of advisors: their exposure to these accounts rose to 13.9% from 12.1% vs little change for the rest of the channel. Given that the top performers have added more new clients than the remaining 80% of advisors, it seems likely this increase in smaller accounts is driven by the top advisors’ new client acquisition efforts.

Of course, the increased exposure to small accounts doesn’t necessarily equate solely to the addition of new clients. In some cases, this exposure may increase as larger clients shift a greater proportion of their assets to the brokerage and dealer industries – thereby dropping these accounts into a lower-value category.

The data hint at the reason. Advisors are reporting their allocations to accounts in the next category up on the value scale (the $100,000-$250,000 range) have declined a bit year-over-year to 27.7% from 29.8%.

Similarly, allocations to accounts in the $250,000-$500,000 range rose to 22.3% from 20%, but allocations to the next category ($500,000-$1 million) are down a bit to 11.3% from 12.8%. Again, this trend suggests that clients may be shifting a greater share of their assets toward the brokers and mutual fund dealer reps in order to increase their exposure to equities – but not necessarily abandoning their advisors at the banks and credit unions altogether.

Perhaps the oddest feature of the account distribution data is that bank-based advisors report that their allocations to the very biggest accounts (those worth more than $2 million) have risen notably to 2.7% from 1.6%. In fact, this rising trend holds for both the top 20% of advisors and the remaining 80%. It’s not entirely clear why this would be the case, although it could reflect a trend of clients cashing out of overheated real estate assets and parking that money for the time being.

Despite the overall decline in AUM and productivity, bank-based advisors’ bottom lines were relatively unscathed. Most report that their compensation falls into the sub-$100,000 category, essentially unchanged from last year.

However, there was a slight decline in pay for the ranks of top-paid advisors – those who reported their annual compensation to be in the $250,000-$500,000 range. The percentage of advisors who fall into this category was down to 1.7% from 2.8%. Most of this decline probably was captured in the increase for advisors earning in the $100,000-$250,000 range.

So, although rising equities may be booming and advisors’ AUM has declined as a result, their take-home pay still looks steady.

© 2014 Investment Executive. All rights reserved.