As regulators take steps to beef up oversight in the insurance sector’s independent distribution channel, most financial advisors as well as their firms and managing general agencies (MGAs) are confident that the regulatory changes will be effective in protecting clients.

Although there are concerns about the hefty amount of administrative work that tends to accompany compliance requirements, the advisors surveyed for this year’s Insurance Advisors’ Report Card were pleased with the support their firms are providing to help them navigate the new rules.

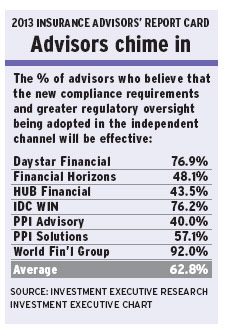

Late last year, the Canadian Council of Insurance Regulators (CCIR) adopted a set of recommendations designed to bring more oversight and accountability to MGAs and independent advisors. The recommendations deal with MGA/insurer relationships, agent supervision, product suitability and the information needs of regulators.

When advisors were asked whether they believe these recommendations will be effective, 62.8% of the advisors surveyed for the Report Card agreed.

“It’s going to help weed out people who are doing wrong, and that will only make our industry stronger,” says an advisor in Atlantic Canada with Calgary-based PPI Solutions Inc.

Other advisors suggested the new regulations could help improve the reputation of the insurance sector overall.

“I’d like the stigma about what goes on to change,” says an advisor in Ontario with Kitchener, Ont.-based Financial Horizons Inc. “People think we just want to gouge clients.”

Most MGAs’ executives also were supportive of the CCIR’s recommendations, suggesting that higher regulatory standards are likely to enhance the professionalism of the insurance sector.

“Improving professionalism is always a good thing, and that can only benefit all the players in the industry,” says Claude Ménard, senior vice president of marketing with PPI Advisory in Toronto.

However, advisors and executives alike admitted that there are plenty of challenges on the compliance front. In particular, many advisors complained about the abundance of compliance-related paperwork that they already face and the time that it takes away from meeting with clients.

“It’s almost overbearing,” says an advisor in Alberta with Toronto-based World Financial Group Insurance Agency of Canada Inc. (WFG). “I spend so much time filling out forms, which prevents me from going to meet families.”

There also were some advisors who felt that the regulators are going too far.

“Sometimes, the intent is good, but that gets lost if there’s too much of a burden on doing business,” says an advisor in Manitoba with Winnipeg-based Daystar Financial Group Inc. “[And] something that should take five minutes takes 45 minutes instead.”

In turn, some MGAs have stepped up their efforts to enhance their compliance processes in recent years as it has become clear that regulators are increasingly focused on this area.

“We’ve invested a lot of money and resources over the past number of years to be compliant,” says John Hamilton, president and CEO of Financial Horizons.

In the absence of industrywide standards and best practices, however, compliance practices have, until now, varied considerably from firm to firm. Thus, some MGAs and advisors are likely to feel the impact of the CCIR’s recommendations to a much greater extent than others will.

“Our company’s compliance is more stringent than [what] the regulators [require],” says an advisor in Alberta with WFG. “That’s why I don’t think it will make a big difference for us.”

Other advisors were more nervous about the impact of the new regulations.

“I think it’s enough as it is,” says an PPI Solutions advisor in Ontario. “If the regulations get tougher, the cost of compliance would be too high.”

Some firms, cognizant of the challenges that advisors face in this area, have taken various steps to ensure advisors have the support and training they need to run a compliant practice. This includes hiring more compliance support staff and hosting seminars and conference calls for advisors, among other initiatives.

The results of this year’s Report Card suggest that advisors are pleased in general with the help they’re getting. In a new category introduced this year, the “MGA’s support in relation to the compliance regime,” MGAs earned an overall average performance rating of 8.9. Furthermore, advisors confirmed that this support is important to them, giving the category an overall average importance rating of 9.2.

Advisors commended firms that communicate regularly on compliance issues and that have compliance staff readily available for support. These are key themes at the firms that earned the top ratings in this new category: WFG (9.3) and PPI Advisory (9.2).

Says an advisor with PPI Advisory in Alberta: “They share information with us to keep us aware of everything.”

Adds a WFG advisor in Alberta: “We have access to two compliance officers in the office that I can talk to at any time.”

Executives recognize that it’s necessary to enhance their compliance support efforts continuously as the regulatory environment evolves. Says Richard Williams, WFG’s president: “The requirements, from a regulatory perspective, have increased dramatically, so we have definitely beefed up our staff. It’s just part of the world we live in now.”

© 2013 Investment Executive. All rights reserved.