Although financial markets continue to be roiled by heightened uncertainty and dogged by the sluggish economic recovery, it appears that Canada’s insurance advisors are managing to build their businesses.

According to the results of Investment Executive‘s (IE‘s) latest survey of insurance advisors, the past year has largely been a time of resurgence. The average advisor has both grown his or her asset base and client base vs the previous year, recovering much of the ground lost in 2011 and bolstering the bottom line in the process.

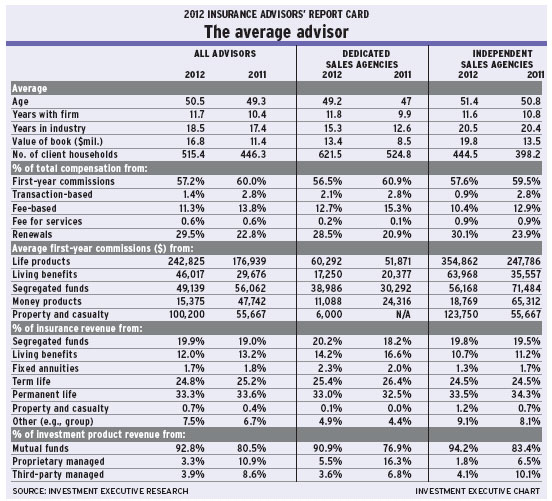

Underlying this story, the basic demographic profile of the average advisor in IE‘s survey is evolving more or less as expected. The average advisor is another year older, at 50.5 years of age, up from 49.3 years in 2011; and he or she has another year in the business under his or her belt – the average advisor’s tenure in the industry has increased to 18.5 years from 17.4 years.

This demographic stability highlights the fact that the insurance sector is aging right alongside its clients and the population at large. There’s no sign of an infusion of youth to bring down those averages.

This stability is echoed by the fact that IE‘s data also show the average advisor is staying put with his or her current firm, as the average tenure with the advisor’s current firm is reported to be 11.7 years, up from 10.4 last year. So, although it appears that the past year has been one of growth, this has not been the robust growth that is often accompanied by an increasing temptation to switch firms in search of a better deal.

These signs of stability are evident throughout the insurance sector – among both independent advisors and those who belong to dedicated sales forces. And although the average independent advisor is still older and more experienced than the average agent with a dedicated sales force, advisors in both channels report being with their current firm for almost 12 years (11.6 years for independents; 11.8 years for dedicated agents).

In the case of the independents, that’s an increase of slightly less than a year over 2011. For the dedicated agents, it’s an increase of almost two years, which suggests this channel is enjoying less mobility.

Despite this steadiness, both channels also have seen impressive growth in their books of business over the past year. Looking at the value of assets under management (AUM) isn’t that meaningful, as this tends to represent a relatively small portion of insurance advisors’ practices. Nevertheless, it’s worth noting that the average advisor saw his or her total AUM jump to $16.8 million from $11.4 million year-over-year.

Dedicated agents saw a bigger percentage jump in their AUM, to $13.4 million from $8.5 million. However, the independents continue to boast bigger absolute totals, with average AUM of $19.8 million, up from $13.5 million.

Although the percentage increases in AUM year-over-year are quite large in both channels of the business, this jump takes these totals back only to the levels reported in the 2010 survey, suggesting that 2011 might have been something of an aberration. So, rather than enjoying some blockbuster growth, it seems more likely that insurance advisors simply have been reviving their businesses over the past year.

It’s a similar situation in terms of the number of client households that advisors are serving. The average advisor now reports that he or she now is handling about 515 client households, up from 446 last year. However, this is just a return to 2010 levels, when the average advisor was servicing 519 client households. Again, these increases are evident in both channels of the insurance sector.

Still, there does appear to be real change taking place in other aspects of the insurance sector. For one, first-year commissions in a number of product lines appear to be on the upswing. Life products remain the biggest contributor to first-year commission totals – and they are growing impressively. In the most recent survey, the average advisor now reports generating $242,825 in first-year commissions from these products, up from $173,939 in 2011 and $146,376 in 2010.

So, while we’re seeing a big jump in these first-year commission totals, this is taking the average advisor well beyond the 2010 levels – not just back to them, as was the case with the increases in AUM and number of client households.

And it’s the independents who are really driving this growth, with their average first-year commissions from life products now at $354,862 a year, up from $247,786 in 2011 and $277,616 in 2010.

At the same time, the independents have seen their first-year commission totals for money products and segregated funds drop noticeably year-over-year.

Among the dedicated agents, the breakdown of first-year commissions generally appears more stable overall. These advisors also have seen solid growth in their first-year commissions from life products, but the increase is much smaller than for the independents, in both dollar and percentage terms – with their average annualized commissions rising to $60,292 from $51,871.

Unlike the independents, the dedicated agents saw their first-year commissions from seg funds increase, while their take from living-benefits products has declined. In addition, their commissions from money products also dropped precipitously year-over-year, to less than half of last year’s total and below 2010 levels.

Despite these shifts, it appears that very little has changed in the product mix of the average advisor’s overall practice. The market share for seg funds is up but down for living benefits, yet the moves aren’t substantial.

That’s not the case for the mix of investment products that advisors use, however, with mutual funds jumping to a 92.8% share this year from 80.5% last year. Conversely, allocations to both proprietary and third-party managed products are down sharply from the previous year.

© 2012 Investment Executive. All rights reserved.