With the insurance industry in a period of transition, insurance advisors surveyed for Investment Executive‘s (IE) 2016 Insurance Advisors’ Report Card appreciate that the dedicated sales agencies and managing general agencies (MGAs) through which they work are able to provide the support needed to steer through those changes and to take advisors’ businesses to new heights.

“[MGAs] are the backbone of the advisor,” says an advisor in Ontario with Kitchener, Ont.-based Financial Horizons Inc. “It’s a network of support.”

One of the big changes in the insurance industry this year is the decision of some firms to eliminate rewards-based travel incentive conferences following a report from the Canadian Life and Health Insurance Association Inc. stating that these trips could contribute to a “perception of a conflict of interest.”

Advisors noted that change is afoot, and although some are disappointed because they appreciate being recognized for their hard work, many are unconcerned. These advisors said they either have never qualified or simply aren’t interested in such conferences.

“I’m not a big believer in rewards,” says an advisor in Atlantic Canada with Waterloo, Ont.-based Sun Life Financial (Canada) Inc. “I get compensated for what I do.”

Another big development in the insurance industry is the increasing pervasiveness of technology and its impact on how advisors run their businesses. In this year’s survey, advisors placed more emphasis on the “support for mobile technology and the mobile advisor” that their firms make available. The overall average importance rating for this category rose substantially, to 8.5 from 6.9, year-over-year. (See page 16.)

“I’m always on the go,” says an advisor in Ontario with London, Ont.-based Freedom 55 Financial. “I’m in the regional office for a couple of hours and then on the road.”

Advisors also are turning to their firms to help them stand out from the crowd – and the results of this year’s Report Card suggest that firms are delivering on that front. The overall average performance rating in the “firm’s marketing support for advisor’s practice” category improved to 7.8 from 7.4 as five firms saw their ratings in the category rise by half a point or more. (See page 17.)

For example, advisors with Toronto PPI Advisory, which saw its marketing support rating rise to 8.9 from 8.0 year-over-year, praised the MGA for its well-staffed marketing department and its online tools and resources.

“We have access [to the marketing department],” says a PPI Advisory advisor in Ontario. “People here have breadth of experience.”

In addition to the support advisors receive to market their businesses to clients, firms that focus on keeping advisors well informed of the many developments in the insurance industry also were praised. Case in point: five firms saw their ratings rise significantly, by half a point or more, in the “firm’s effectiveness in keeping advisors informed” category.

Says an advisor in Ontario with Mississauga, Ont.-based RBC Life Insurance Co.: “We get regular updates anytime something comes up. They come directly to our email.”

RBC Life, PPI Advisory and Woodbridge, Ont.-based Hub Financial Inc. were among the firms that saw their ratings increase by half a point or more in several categories. These improved ratings led to an increase of the same margin in their IE ratings, which is the average of the ratings these firms received in all the categories, for these three firms. Conversely, Sun Life saw its ratings decline by a half a point or more in 12 of the 33 categories in which it was rated. (See page 11.)

All the ratings in this year’s Report Card were gathered by IE research journalists Megan Marrelli, Beatrice Paez and Kat Shermack, who spoke with 345 advisors at three dedicated sales agencies and six independent agencies (five of which are MGAs).

To participate in the Report Card, advisors must be either full-time employees of a dedicated sales agency or run at least 50% of their business through one of the MGAs in the survey.

Advisors were asked to rate their firm’s performance in a given category – as well as how important that category is to their business – on a scale of zero to 10, with zero meaning “poor” or “unimportant” and 10 meaning “excellent” or “critically important.”

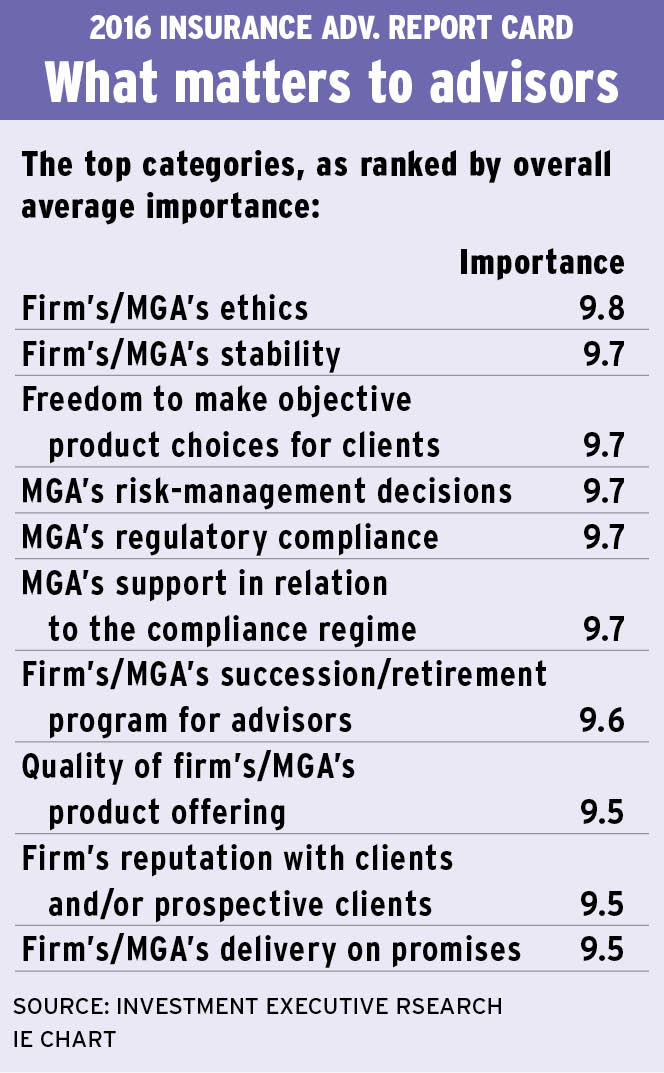

Although there were many changes in this year’s ratings vs last year, one thing remains constant: firms are delivering on what matters most to advisors.

For example, advisors gave “firm’s/MGA’s ethics,” “firm’s/MGA’s stability” and “MGA’s regulatory compliance” the top overall average importance ratings as well as the top overall average performance ratings in this year’s Report Card.

As for the increasing importance of compliance in the insurance industry, advisors appreciate that their MGAs are on top of the latest regulatory requirements. Compliance also figures heavily in an advisor’s thoughts on ethics, and many advisors praised the firms that have few infractions and honest staff members.

“You can drop $1,000 on the floor,” says an advisor on the Prairies with Calgary-based PPI Solutions Inc., “and [the staff] would go out of their way to find who [the money] belongs to.”

© 2016 Investment Executive. All rights reserved.