Canada’s big six banks are struggling to live up to their branch-based financial advisors’ expectations in some critical categories, ranging from compensation packages to wealth-management support services and technology tools, according to the results of Investment Executive‘s (IE) 2017 Report Card on Banks.

“The [technology] systems are slower; procedures take longer,” says an advisor in Atlantic Canada with Montreal-based National Bank of Canada. “Productivity has really gone down on a lot of levels. There’s a disconnection between management and people on the ground: expectations cannot be met; sales targets cannot be hit.”

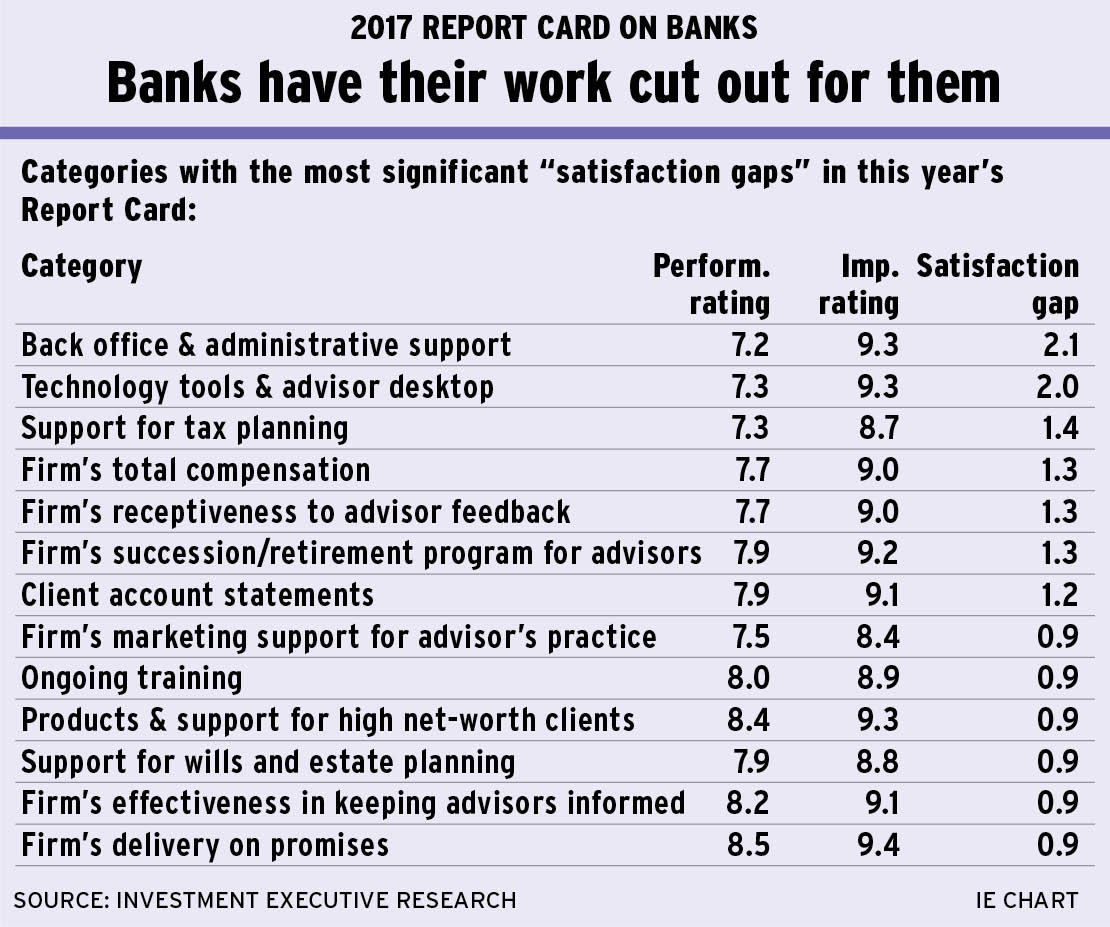

The banks’ failure to meet advisors’ expectations is evident in the significant “satisfaction gaps” – the differences between the overall average importance and overall average performance ratings – in categories in which advisors rely upon their banks, such as “firm’s total compensation,” “support for tax planning” and “technology tools and advisor desktop.” These categories garnered some of the largest satisfaction gaps in the survey, ranging from 1.3 points to 2.0 points.

In the case of tax planning support, five of the six banks’ performance ratings in the category dropped by half a point or more year-over-year. As a result, the satisfaction gap for this category is the third-widest in the survey.

Advisors at the banks are able to discuss taxes with clients only in the broadest of terms and are, therefore, dependent on their banks to provide access to tax experts. However, advisors often find themselves having to refer clients to third-party accountants because the banks’ specialists are available only through cumbersome call centres or to clients who qualify as high-net worth.

Read: Some support services are lacking

“I just send clients over to their accountants,” says an advisor in Ontario with Toronto-based Bank of Montreal (BMO). “I guess I could go through private wealth, but they’re getting a bit more picky about who you can send to them.”

The results of this year’s Report Card also reveal advisors’ dissatisfaction with their changing compensation and pension plans.

In fact, advisors with Bank of Nova Scotia and Canadian Imperial Bank of Commerce (CIBC), both based in Toronto, and National Bank received the lowest or much lower ratings in the “firm’s total compensation” category as a result of recent changes to advisors’ pay structures.

“I’m not at all impressed with how they did the salary cut,” says an advisor in Quebec with National Bank. “I know the market is tough. But when employees are used to a certain salary, that’s an enormous change. Maybe they could have done it a different way. I don’t know how, but it was really drastic.”

Read: Changes to paycheques upset advisors

As well, advisors were not pleased with changes to their pension plans and, in fact, the satisfaction gap for the “firm’s succession/retirement program for advisors” category was tied for the fourth-widest in the Report Card.

Having a reliable pension plan is important to branch-based advisors because, unlike advisors in the brokerage or dealer channels, bank branch-based advisors don’t own their books of business and, therefore, cannot live off the proceeds of the sale of their business in retirement.

However, most advisors surveyed for this Report Card complained about the general shift to defined-contribution pension plans from defined-benefit plans. Furthermore, Scotiabank advisors, specifically, took issue with that bank’s recent decision to eliminate the option to transfer the commuted value of a pension at retirement and gave their bank the lowest performance rating in the succession/retirement category, at 7.4.

“With the changes, [the bank] is going away from defined benefits [and] we won’t be able to take our commuted values,” says a Scotiabank advisor in Alberta. “[There are] quite a few changes that would affect me. It might be better for me to retire next year instead.”

Read: Pension plans leave much to be desired

Advisors surveyed for this year’s Report Card also were not shy about expressing their disappointment with the advisor-facing technology available at their respective banks.

Indeed, most banks’ tech tools simply aren’t up to scratch, which is evident from the fact that advisors gave the tech tools/advisor desktop category the second- widest satisfaction gap in the Report Card. Much of the frustration stems from the perceived gap between the banks’ investments in technology and the delivery time of promised upgrades.

“There is a lot of technology changing right now. Sometimes, those changes are a bit slow,” says an advisor in Ontario with Toronto-based Royal Bank of Canada.

Read: Banks are falling behind in technology

Advisors do give credit to the banks where it’s due, though, which was the case for client-facing technology. In fact, advisors were so impressed, by and large, with their banks’ efforts in this category that the satisfaction gap for “online account access for clients” is virtually non-existent.

“[Making] the online experience really optimal to clients has been CIBC’s focus,” says a CIBC advisor in Ontario. “We make sure clients have access to online statements.”

Read: Banks deliver on clients’ online access

Advisors also gave their banks top performance marks for “firm’s stability” – tied for second place (with “firm’s reputation with clients and/or prospective clients”) in importance to advisors – which may not be so surprising, given that the Big Six banks are some of the oldest and most profitable companies in Canada.

“We’ve been around for 200 years,” says a BMO advisor on the Prairies. “It’s the oldest bank in Canada.”

A lengthy corporate history is important to advisors because it plays a big part of a bank’s overall brand recognition.

For the most part, advisors believe their banks’ reputations are solid,conferring an overall average performance rating of 8.8 in the reputation category.

However, some advisors noted that their bank’s reputation – and, by extension, their own – has taken a hit this past year, given recent media reports about aggressive sales practices.

“There are a few things in the media right now; it’s hard because everyone gets painted with the same brush,” says an advisor on the Prairies with TD Wealth Financial Planning, a division of Toronto-Dominion Bank. “We’re all guilty by association.”

How we did it

Canada’s big six banks have large, arguably confusing organizational charts and thousands of employees, including financial advisors, who work with different clientele based on the advisors’ positions within these corporate behemoths.

Therefore, Investment Executive (IE) follows strict criteria when putting together the Report Card on Banks in order to cut through the bureaucracy and ensure we’re speaking to advisors who work at a comparable level in all the banks.

In order to participate in the survey, advisors must work in a bank branch, typically fulfilling a financial planning role; have long-term client relationships with mass-affluent individuals; and focus primarily on investments, as opposed to selling credit products.

As well, these advisors typically are employees of the banks’ retail divisions – with the exception of the financial planners working at Toronto-Dominion Bank (TD). Even though TD financial planners work in the bank’s branch network, they are part of TD Wealth Financial Planning, a unit of TD Wealth Management.

Regardless of these advisors’ varied positions within the banks’ corporate structures, the aim of IE’s Report Card is to give all these advisors a voice.

That voice came through loudly in the ratings found in the Report Card’s main table on page 12. These ratings were gathered from the results of 300 surveys that IE research journalists Latifa Abdin, Sophie Allen-Barron, Charles Bossy and Jennifer Cheng conducted.

Advisors who participated in the survey provided two ratings for each category: one for their bank’s performance and another to signify the importance of that category to the advisor’s business.

The ratings are based on a scale of zero to 10, with zero meaning “poor” or “unimportant” and 10 meaning “excellent” or “critically important.”

© 2017 Investment Executive. All rights reserved.