There appears to be much miscommunication regarding banks’ receptiveness to their financial advisors’ feedback, according to the results of this year’s Report Card on Banks.

On one hand, advisors were unhappy with the way their banks fail to respond to or use advisors’ feedback. On the other hand, the banks reported that they take advisors’ feedback seriously before making any major changes.

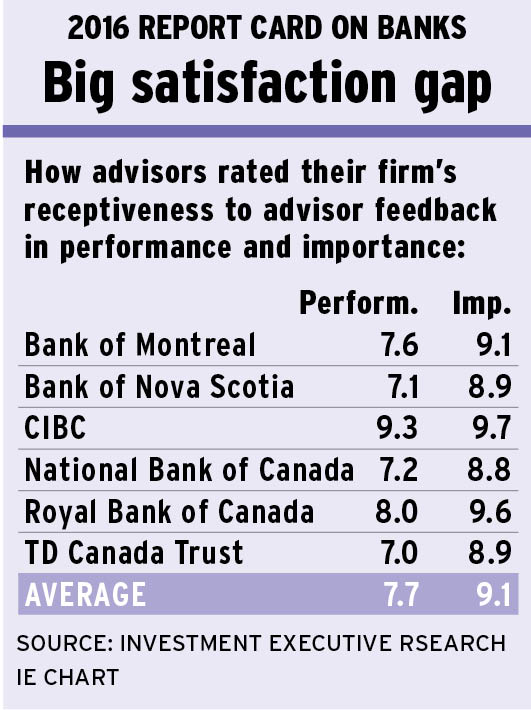

Advisors’ dissatisfaction is most evident in the fact that four of the six banks in the survey – Bank of Nova Scotia, Royal Bank of Canada (RBC), TD Canada Trust (all based in Toronto) and Montreal-based National Bank of Canada – saw their performance ratings in the “firm’s receptiveness to advisor feedback” category drop by half a point or more this year.

Consequently, the overall average performance rating for the category dropped to 7.7 from 8.2 year-over-year. This decline also resulted in a larger “satisfaction gap” – the difference between the overall average importance and performance ratings – for the category.

Specifically, advisors rated the category at 9.1 in overall average importance – 1.4 points higher than the overall average performance rating. This satisfaction gap is the third-largest such gap in this year’s Report Card.

The most common complaint among advisors was that even though their banks collect advisors’ feedback through surveys, roundtable discussions and focus groups, those efforts seldom lead to discernible change.

“They ask [for feedback], but I don’t think anybody reviews it,” says a National Bank advisor in Quebec. “I don’t think our voice reaches management.”

“You can express your opinion, but does anything necessarily happen? No,” says a TD advisor in Ontario, which received the lowest rating in the category, at 7.0, down from 8.0 last year. “The concerns we’ve had for the past 10 years are just not as important for the company as they are for us.”

However, Lee Bennett, senior vice president, TD Wealth Financial Planning, says there are several ways the bank takes advisors’ feedback into account, including through focus groups, surveys, as well as going out into the field and asking questions.

“We’ve implemented more than six major technology enhancements to improve both the client experience and the advisor experience,” she says. “Those implementations were all part of the feedback we received.”

The disconnection between what advisors believe their bank is doing with the feedback and what the firm actually does with it is not exclusive to TD. For example, an advisor in Ontario with National Bank, which saw its performance rating in the feedback category drop to 7.2 from 8.3 year-over-year, says: “Some people are recognized with more money and acknowledgment, in that they’ll invite you to a roundtable program. [This method] almost feels like they’re giving everybody a carrot in one form or another. Any time I’ve done it in the past, [my participation] is not necessarily translated into change.”

But that feedback from advisors has been a crucial part of the way National Bank incorporates changes today, says Annamaria Testani, vice president of national sales at National Bank.

Specifically, she points to a recent example in which the bank’s management was overhauling a product: “In the olden days, we would have gone into a closed room, [then] the engineers would have come out and said, ‘This is what you’re going to do.’ We didn’t do that [this time]. We held an enormous amount of focus groups with our financial planners, [put their ideas on a] whiteboard and [asked them], ‘Look, if you need a high net-worth product in the banking channel, what do you want with it?'”

Still, despite what executives say, many advisors across the board don’t believe their bank’s executives take these suggestions seriously. As an RBC advisor on the Prairies says: “We have surveys all the time. You do the same survey every year. I personally think it’s a waste of time.”

But a major challenge in listening to advisors and responding to their concerns may be the sheer volume of feedback that some bank executives receive. For example, Michael Walker, vice president and head of branch investments with RBC, which saw its rating drop to 8.0 from 8.6 in 2015, says that because there are so many advisors offering input, “it takes a lot of time and focus to [review their feedback] well.”

At RBC, feedback is taken seriously, he adds: “When we hear a point of view more than once. That’s when we go ‘OK, this is not an individual issue or an individual point of view. There is broader opportunity to act on this’.”

In contrast, advisors with Toronto-based Canadian Imperial Bank of Commerce (CIBC) were the only ones surveyed who were highly satisfied with their bank’s approach toward accepting advisor feedback. They rated their bank at 9.3 in the category, virtually identical to the 9.4 rating they gave last year.

Specifically, CIBC advisors appear to be satisfied with the bank’s open-door policy to management, egalitarian culture and prompt action taken when concerns or issues are brought up.

“I just came back from the conference and we had lunch with the CEO,” says a CIBC advisor in Ontario. “He was there with pen and paper, and said if anyone has any ideas, to contact him directly.”

“You get a sense that if you say something to someone higher up, they will take information back and do something with it,” adds a colleague in the same province. “That wasn’t the case a few years ago. [Back then], nothing happened with the feedback you gave.”

© 2016 Investment Executive. All rights reserved.