The financial advisors surveyed for Investment Executive‘s (IE) 2015 Report Card on Banks and Credit Unions (CUs) had strong opinions about the deposit-taking institutions at which they work. Indeed, advisors heaped praise – and higher ratings – on their firms when they met advisors’ expectations. Advisors were equally vocal in areas in which they felt their firms need to step up their game.

For example, advisors with Toronto-based Canadian Imperial Bank of Commerce (CIBC) had no shortage of accolades for their firm – and those sentiments are evident in the ratings they bestowed upon their bank for the second straight year.

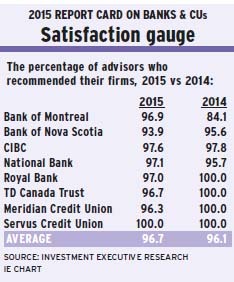

In last year’s Report Card, ratings for CIBC rose by half a point or more in 26 of the 33 categories in which it was rated. CIBC’s “IE rating,” which is the average of all the categories in which the bank was rated, and its “overall rating by advisors,” which indicates how advisors rated the bank out of 10, also rose by that same margin.

That trend continued this year. CIBC’s ratings rose by half a point or more in 20 of the 32 categories in which it was rated – as well as in its IE rating and overall rating by advisors. As a result, CIBC received the highest ratings for these last two categories in the Report Card.

“I joined a family,” says a CIBC advisor in Ontario. “We work together as a large team. You feel like you have the support to be successful.”

Adds a colleague in the same province: “I enjoy the culture. Gone are the days of promoting mediocrity.”

In fact, those days weren’t so long ago. In 2008, CIBC had the lowest IE rating and overall rating among all the deposit-taking institutions in that year’s Report Card. Since then, CIBC has made substantial investments in its business, from technology to wealth-management support services.

“We’ve really been on a journey,” says Larry Tomei, senior vice president, national sales and service, retail and business banking, with CIBC. “Building what we think is the best bank advisory program is not just a one-year or two-year thing; it’s an everyday, all the time thing.”

St. Catharines, Ont.-based Meridian Credit Union also had a strong showing in the Report Card for the second year in a row. In 2014, Meridian’s ratings rose by half a point or more in 20 of the 35 categories in which it was rated – as well as in its IE rating.

This year, Meridian’s ratings rose by that same margin in five of 32 categories, with advisors praising the CU’s efforts in categories such as “support for mobile technology and the mobile advisor” and the “advisor’s relationship with the compliance department.”

“Our compliance department, along with the back-office support, are proactive. They’re always there to answer questions,” says a Meridian advisor in Ontario. “Somehow they do it in a way that they’re nice and easy to deal with.”

Although neither CIBC nor Meridian saw their ratings drop by half a point or more in any category in this year’s Report Card, the other six deposit-taking institutions were not as fortunate. For example, Edmonton-based Servus Credit Union’s ratings dropped by that margin in 13 of 32 categories this year while rising by that same margin in only one category.

When asked about which categories Servus could most improve in, an advisor in Alberta says, “Technology [and] access to relevant information that we need for compliance.”

Servus advisors were not the only ones taking issue with their firm’s technology. In fact, the “support for technology tools and advisor desktop” category had the largest difference between the overall average importance rating (9.1) and the overall average performance rating (7.2) – known as the “satisfaction gap” – among any category in this year’s Report Card. (See story on page 20.)

“[The systems] are archaic,” says an advisor in Ontario of Montreal-based National Bank of Canada’s tech tools. “Our technology needs a huge quantum leap.”

Although advisors had significant issues with the technology their firms offer, many advisors were more than happy with the technology that their firms offer to clients. In fact, advisors rated their firms’ “online account access for clients” at 8.9 overall in performance. (See page 20.)

Advisors who were happiest with their firms’ efforts in this category appreciated online platforms for clients that are easy to use and understand. “[Our online platform for clients] is very easy to sign up for and access,” says an advisor in Ontario with Toronto-based Bank of Montreal. “And it’s very clear on how to move around within it.”

Yet, things aren’t always so clear for advisors in getting help for managing their clients’ complex wealth-management needs. In particular, advisors said, they don’t have the expertise to help clients in these areas, so they’re dependent upon their firms for help.

“[These are] fairly specialized areas, and not enough advisors are comfortable in [them],” says an advisor in Ontario with the Toronto-based Royal Bank of Canada.

But, many advisors said, their firms’ support in “support for tax planning” and “support for wills and estate planning” are falling short: these categories had the third- and fourth-highest (the latter a tie) satisfaction gaps in the survey, respectively. (See page 18.)

Although there were significant satisfaction gaps in many important categories, firms are delivering in the areas that matter most to advisors – namely “firm’s ethics” and “firm’s stability.” These two categories received the highest overall average importance and performance ratings in this year’s Report Card.

In terms of stability, advisors appreciated their firms’ strong financial footing, as well as their strong leadership.

“We are Ontario’s largest credit union,” says a Meridian advisor in Ontario. “We’re the largest in the communities we serve, and we’re growing. I feel very good about the leadership here.”

As for ethics, advisors said, the way their firms make business decisions and treat clients is important. But, beyond that, advisors appreciated their firms considering their roles in society.

“[The bank] provides good support to the local community and encourages staff to participate,” says an advisor in Alberta with Toronto-based TD Canada Trust.

Advisors with all the deposit-taking institutions in the Report Card said their firms following through on the promises they make also matters. In fact, the “firm’s delivery on promises” category was tied for the second-highest overall average importance rating, at 9.5.

One mechanism that TD employs to ensure it’s delivering on its advisors’ expectations is its annual Pulse survey. “It is very much a part of TD’s culture,” says Lee Bennett, senior vice president of TD Wealth Financial Planning, about Pulse, which provides management with direction in how they can help advisors grow within their role.

How we did it

Every year, the results of Investment Executive‘s (IE) Report Card on Banks and Credit Unions are obtained by asking financial advisors with deposit-taking institutions to rate their firms in a variety of categories. That tradition continued this year, although the categories in which advisors rated their firms were slightly different than in years past.

Specifically, IE research journalists Joy Blenman, Kevin Philipupillai, Kelsey Rolfe and Anne-Marie Vettorel asked 244 mutual-fund licensed advisors at six banks and two credit unions to rate their firms in 32 categories – down from 35 in 2014.

That’s because the “support for helping clients accumulate assets for retirement,” “support for an overall wealth-management process” and “firm’s diversity and inclusion strategy” categories were removed from the survey.

As well, the “support for helping clients plan for post-retirement income” category was reworded to “support for constructing a deaccumulation strategy for retired clients.” IE intended to compare these ratings year-over-year, but the results were so different that the category was treated as new.

The other big change in this year’s survey was a supplementary question asking advisors to rate how dramatically they expect the implementation of the second phase of the client relationship model to affect their businesses on a scale of one to five, with one representing “not at all” and five representing “completely.”

The ratings for the categories in the main table on page 17 maintained the same format as in years past. Advisors were asked to rate their firms’ performance in each category, as well as that category’s importance to their businesses, on a scale of zero to 10, with zero meaning “poor” or “unimportant” and 10 meaning “excellent” or “critically important.”

© 2015 Investment Executive. All rights reserved.