FINANCIAL ADVISORS IN CANADA’S DEALER CHANNEL appear to be settling into a comfortable, almost sedentary middle age. They clearly are getting older and their average financial picture is not growing much – if at all.

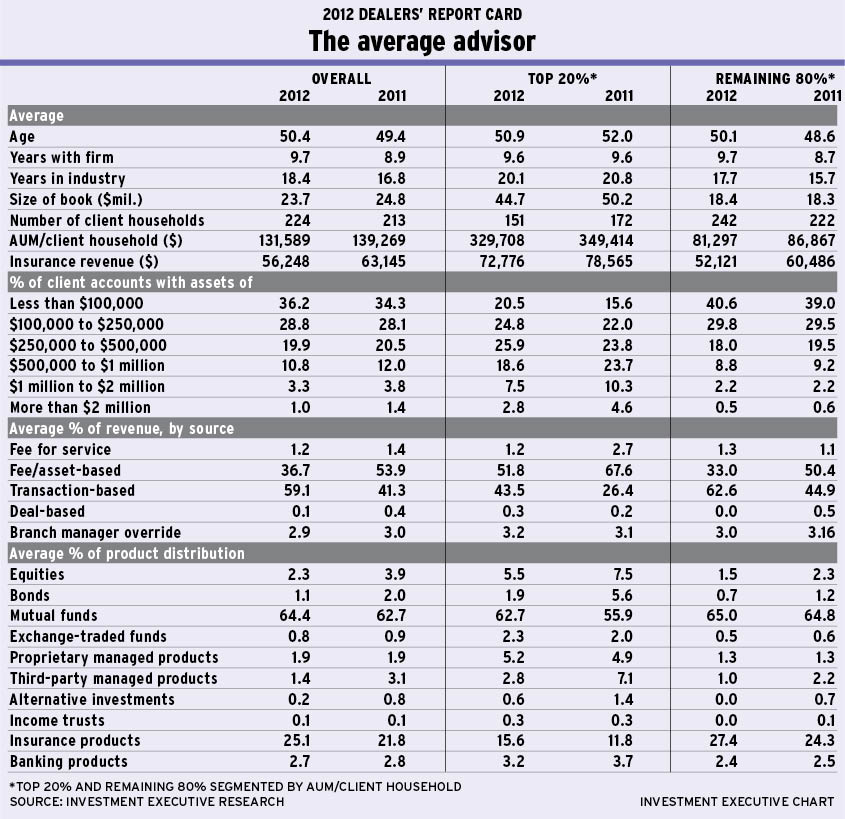

The latest version of Investment Executive‘s (IE’s) annual Dealers’ Report Card found that the average advisor in the survey is now 50.4 years old with more than 18 years of experience in the business and has spent 9.7 years at his or her current firm.

All of these metrics are up by about one full year from last year’s survey, indicating that the underlying demographics of the advisor ranks at the dealers hasn’t changed much year-over-year. There hasn’t been an influx of rookies to bring fresh blood into the channel; nor has there been a wave of retirements among the older reps, which would limit the increase in these averages.

Of course, given the market climate, it’s not hard to see why the picture for the dealer channel appears so unchanged. For prospective new reps, it’s a tough time to try to build a book; for the older reps, they may feel that they can’t afford to retire, given the turmoil of the past few years and the effect that has had on both their clients and advisors’ businesses.

Indeed, average assets under management (AUM) for dealer reps in IE‘s survey actually declined slightly year-over-year. Average AUM in this year’s survey was $23.7 million, down from $24.8 million last year. And average productivity – measured by AUM per client household – also was down, to $131,589 from $139,269.

This dip in productivity can be attributed to changes on both sides of the equation – not only was average AUM down a bit year-over-year, but average client rosters were up – so the reps have spread smaller asset bases across slightly larger books.

However, the picture looks a bit different when you divide the sector into top-performing reps and the rest of the channel. (IE segments the dealer sales force by AUM/client household into the top 20% of reps and the remaining 80%.) And although both segments of the dealer channel are seeing their productivity decline, the drivers of those declines are somewhat different for the two groups.

For the top 20% of reps, average AUM was down notably to $44.7 million this year from $50.2 million last year. But this drop in AUM also has been accompanied by a reduction in the average number of client households they serve to 151 this year from 172 last year. This pruning of client rosters has served to ameliorate some of the drop in productivity that these reps would have faced amid the double-digit decline in AUM. As a result, the fall-off in productivity amounts to less than 6% year-over-year, as average AUM/client household has slipped to almost $329,708 from $349,414.

The remaining 80% of advisors at the dealers experienced a comparable 6.4% drop in productivity, with their average AUM/client household slipping to $81,297 in the current survey from $86,867 last year. But, unlike the top 20%, who saw both AUM and client numbers decline, the rest of the dealer channel experienced slight gains in both categories.

For the advisors among the remaining 80%, this past year has been a case of running harder to stay in place. Average AUM for these reps inched upward to $18.4 million from $18.3 million last year. But, to maintain that number, their client rosters grew by about 9% to 242 client households from 222 last year.

The weakening in productivity experienced by both segments of the dealer channel also is reflected in the account distribution data. Allocations to the smaller account sizes within the average advisor’s book were up from the previous year. Overall, accounts worth less than $250,000 represented 65% of the average book this year, up from 62.4% last year.

This trend is evident in both segments of the dealer channel. That said, the increases in allocation for the top 20% of reps have come in all account categories worth less than $500,000. And, even for these top producers, the biggest increase was in the sub-$100,000 category, in which the allocation has grown to 20.5% from 15.6%.

Conversely, the top 20% of advisors saw significant drops in the allocations in their book to the largest account categories. Accounts worth more than $1 million represented 14.9% of the books of the top-producing reps in last year’s survey; this year, that figure was down to 10.3%.

For the remaining 80% of reps, the swing in account allocations was somewhat less dramatic. The share of book for accounts worth more than $500,000 was almost unchanged from last year. Allocations to accounts in the $250,000-$500,000 range were down by about 7.7% year-over-year. And, at the same time, allocations to the smallest accounts (less than $250,000) were up by 2.8% from last year.

More striking than the swings in account distribution are the seismic shifts in revenue mix that emerge in this year’s data. The average rep in IE‘s survey reported that transaction-based revenue has jumped to 59.1% of their revenue this year from 41.3% last year; at the same time, fee- and asset-based revenue collectively were down to 36.7% from 53.9%.

To some extent, these abrupt swings between asset- and transaction-based sources of revenue represent a reversal in the trends seen last year. In 2010, reps reported that their revenue was more or less evenly split between transactions and asset-based sources. Then, in last year’s survey, the numbers swung sharply in favour of fee- and asset-driven sources. This year, it appears that trend has reversed, swinging back heavily in favour of transactions.

Although the magnitude of the shift back toward transactions may be somewhat overstated by the fact the numbers had moved substantially in the opposite direction last year, there’s no questioning the direction of this year’s move. The evident resurgence in the importance of transactions may reflect a couple of trends.

For one, it could be evidence of increased client movement. Clients that move their accounts between reps or from other types of firms (such as banks and investment dealers) may lead to portfolios being more actively traded; thus, the transactions involved end up generating more revenue than the fees that are being produced by more static, longtime clients.

There also is the possibility that the significance of fees is declining for several reasons. For one, the apparent shifts in account distribution could be a factor affecting the revenue mix. The increase in allocations in the average book to smaller accounts may be undermining the importance of fees – either because firms aren’t as likely to use asset-based charges for their smaller clients or these clients prefer transactions to fees.

Similarly, increasing cost-consciousness among clients may mean that fewer clients are willing to pay ongoing fees. At a time when portfolio returns are so meagre, even a modest fee can eat up a substantial portion of those returns. So, clients may well be drifting away from asset-based compensation arrangements and back toward traditional transactions.

In addition, it may be that in circumstances in which fees are being paid, the size of the fees themselves are dropping. Indeed, ongoing market uncertainty has driven many mutual fund investors away from equities and toward fixed-income funds over the past year – and fixed-income funds pay lower trailers than equity funds, so this could be helping to erode that source of revenue.

Whatever the explanation – and there probably isn’t just one – this trend toward transactions and away from fees is evident among both the top 20% of reps and the remaining 80%. For the top 20%, fees still represented 51.8% of revenue, but that was down from 67.6% last year. Meanwhile, for the remaining 80%, fees accounted for 33% of their annual revenue, down from 50.4% last year.

Dealer reps also saw their insurance revenue decline. This year, the average rep’s insurance revenue amounted to $56,248 for the year, which is down from about $63,145 last year. This downward trend held true for both the top 20% of reps and the rest of the channel.

And yet, although overall insurance revenue was down from last year, reps reported that insurance products are making up a bigger part of the products they sell, up to 25.1% from 21.8% last year.

Within their insurance practices, however, the product mix had hardly changed. The notable gain was for segregated funds, which saw their share of the average book rise to 28.7% from 26.8%.

Use of mutual funds also rose, to 64.4% of the average book from 62.7% last year. At the same time, holdings of direct equities, bonds and exchange-traded funds were all down a bit from last year.

Third-party managed accounts saw their share of the average book shrink, too. Although proprietary managed accounts still make up about 2% of the average rep’s book, allocations to third-party accounts were more than halved to just 1.4% from 3.1%.

Allocations to alternative investments also were down – albeit to 0.2% this year from a mere 0.8% last year.

Other than these categories, it appears that there haven’t been any big changes to the product mix of the average portfolio.

This sort of stasis seems to be reflected within much of the dealer channel these days. On the surface, the business looks little changed from last year – but it appears that reps may be working a bit harder just to maintain their position within the financial services industry.

© 2012 Investment Executive. All rights reserved.