Financial advisors looking for a competitive advantage could find significant value in the alphabet soup of financial services industry-specific designations – particularly in the wake of more calls for increased professionalism in the industry.

However, data collected between 2009 and 2012 as part of Investment Executive‘s annual Report Card series reveal only minimal growth in the proportion of advisors who have acquired a professional designation.

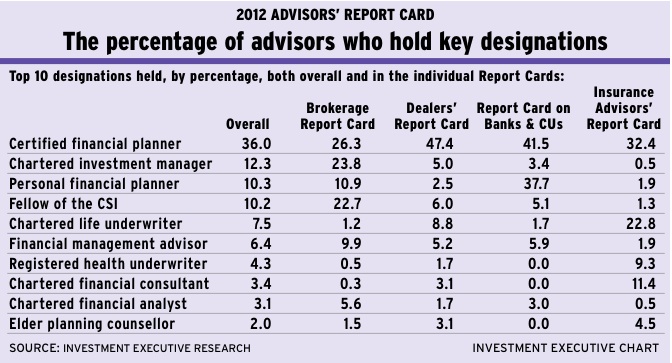

For example, the proportion of advisors who have acquired a certified financial planner (CFP) designation has grown only incrementally, to 36% in 2012 from 33.6% in 2009. Holders of the chartered investment manager designation topped out at 12.3% in both 2012 and 2011, up from a low of 9.7% in 2009. The acquisition of other designations – such as the financial management advisor and the chartered life underwriter – has remained stagnant, consistently in the range of 6.4%-7.5% of advisors.

Although professional designations are not demanded outright by most firms, they will be of increasing importance to advisors in the coming years. In particular, designations will be a way to help advisors distinguish themselves from their colleagues by staying ahead of the curve through their specialized knowledge.

“What we’ve seen since the financial crisis of 2008 is that investment advice in isolation is not sufficient – people need the advice of somebody who has that broader perspective,” says Cary List, president and CEO of the Toronto-based Financial Planning Standards Council, which enforces professional standards in financial planning. “I think the days of being able to make a living by choosing one particular company or product over another – or one particular mutual fund over another – are going to be gone pretty soon. Advisors are going to be challenged.”

Janet Ecker, president of the Toronto Financial Services Alliance (TFSA), says that there is going to be a greater need for designations among both advisors and their firms as they move into a more regulated and risk-averse world.

“Designations are a good proxy for saying we have good talent,” Ecker says. “We want to encourage more people to continue to obtain professional designations because it keeps that quality of talent very high.”

Although encouraging an advisor to take on the added work of obtaining (and maintaining) a professional designation can be a tough sell, Ecker says, over the long haul, it is a choice that will benefit the advisor: “It is good marketing [for advisors] personally, and [as an advisor] you will be able to do a better job, make more money and be of more value to your employer.”

Moreover, as the distinctions among the financial services industry’s traditional channels continue to blur, advisors need to decide what kind of clients they want to go after and then obtain the necessary designations to serve those clients properly, says Marc Flynn, vice president, regulatory relations and academic standards with Toronto-based CSI Global Education Inc., who notes: “A lot of designations were created to provide a different body of knowledge for a different clientele.”

Given the pressure to meet bottom lines, many advisors may decry the added time required to acquire a professional designation in lieu of spending time in developing their client base. Nevertheless, Alan Middleton, executive director of the Schulich Executive Education Centre at York University’s Schulich School of Business, says the long-term payoff will be of net benefit to advisors.

“[A designation] will add to your capabilities and [advisors] will have higher value-added relationships with clients,” says Middleton. “It’s the old rule – the people who tend to do well are prepared to accept delayed gratification.”

Although obtaining designations is important, Catherine Chandler-Crichlow, executive director of the TFSA’s Centre of Excellence in Financial Services Education, says a “balanced approach” to continued development is essential.

“Having a designation [in isolation] is not enough,” she says, adding that advisors need a broader range of competence and skills, which are garnered both from education and experience.

Several designations, including the CFP, have evolved in recent years to reflect these growing concerns. In 2010, for example, the certification process for the CFP went from being a single exam to a more thorough process that includes: the writing of two exams; the completion of a course between those exams, during which students are required to prepare a financial plan; and three years of mandatory financial planning experience.

Although the onus for obtaining professional designations is largely on individual advisors, financial services firms have a significant role to play in helping their advisors in this process. For instance, some of the firms in the 2012 Report Card series pay the fees for obtaining a designation on behalf of their advisors.

However, some firms would rather spend their money on “in-house” training for their advisors in the form of seminars and webinars. Although such programs could be very helpful for advisors, List says, they have some serious limitations because much of that training is geared toward sales.

“Sales skills are important,” says List, “but that doesn’t make you qualified as a professional advisor. [Firms and product] manufacturers aren’t teaching you the set of knowledge about tax laws and how you calculate a needs analysis; they’re arming you with the skills you need to sell. That’s the sales side, not the professional advice side.”

Many advisors agree with that assessment. Says an advisor in Manitoba with Winnipeg-based Great-West Life Assurance Co.: “[The firm] focuses too much on short-term sales. There is very little support for doing any kind of planning.”

Adds an advisor in Atlantic Canada with Lévis, Que.-based Desjardins Financial Security Independent Network: “The industry wants us to be planners, but they force us to be salespeople.”

© 2012 Investment Executive. All rights reserved.